October jobs surprise, Amazon is relentless, Apple dips, Intel pops

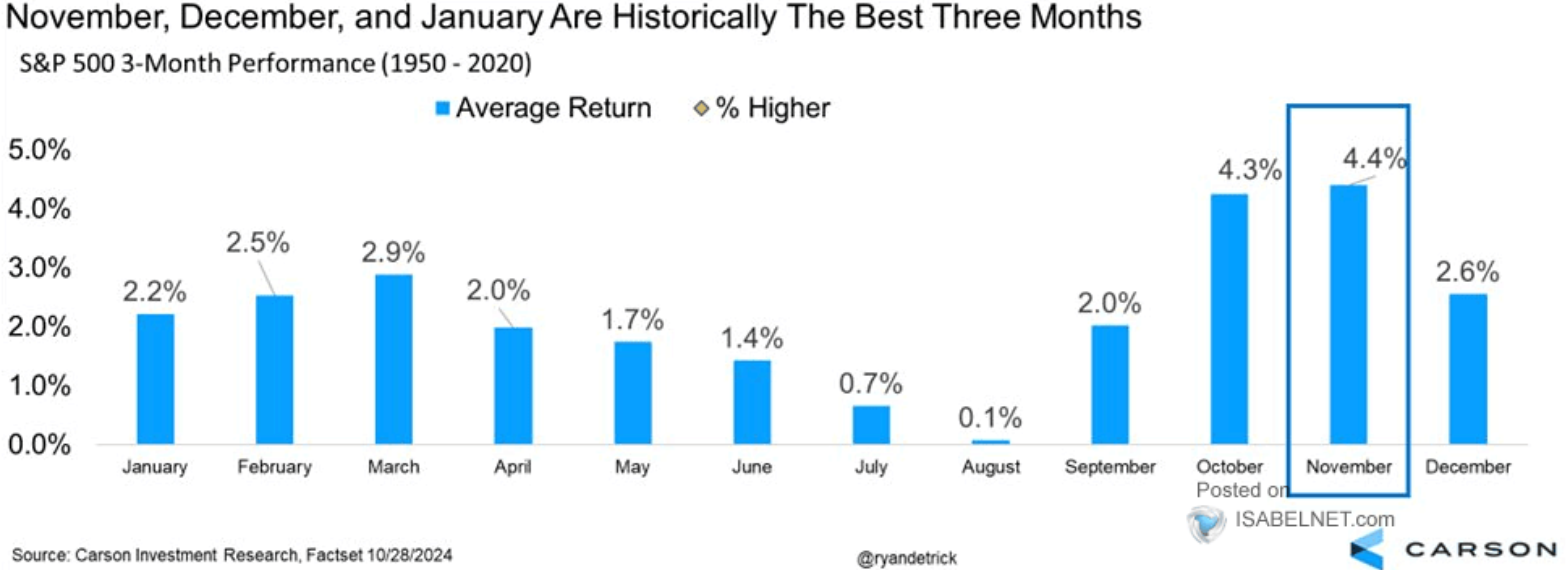

Sugar crash: I had to double check my screen when US jobs data came out. The US economy added just 12,000 jobs in October. That’s well below the 100,000 that was expected and is the worst pace of job growth since December 2020. This is likely due to a lot of hurricane distortion and strike action at Boeing. Indeed, the unemployment rate held steady at 4.1%. Futures are still positive after the print, so investors may look through this. Will voters? Yesterday’s sell-off in stocks was so severe that it wiped out all the October gains for the S&P 500. This halts what was a 5-month win streak for the index. The TSX fared a little better in October eking out a modest gain and extending its monthly win streak to four months of gains. While October was a disappointment, worth noting we are still in a seasonally strong period for stocks. Check the chart below from Ryan Detrick at Carson:

Relentless: Shares of Amazon could hit an all-time high after an earnings hat trick. Profit, sales and the forecast all came in better than expected. The joked used to be the Amazon was the world’s largest non-profit. You really can’t say that anymore. Indeed, the company is now forecasting $20 billion in operating income, which is well above expectations. As Dan Ives at Wedbush points out, Amazon has now reported operating income above the high end of its forecast range for a seventh consecutive month. So maybe there is upside to the forecast. Most think of Amazon as the everything store, but its cloud business is the profit crown jewel. The retail business was 80% of sales this quarter, but just 40% of operating income. Compare this to the cloud business which is 17% of sales, but 60% of operating income. Growth in AI has reaccelerated growth at Amazon Web Services. Amazon could be the biggest mega cap winner in AI according to Rohit Kulkarni at Roth MKM. “Amazon has integrated AI into what is the most diverse tech footprint of any mega cap, with multi-billion revenue streams in e-commerce, advertising, subscriptions, online video, and cloud,” he wrote in a note to clients.

Apple a day: Apple earnings are a bit of a let down this morning with the stock drifting lower in the pre-market. Apple grew sales 6% this quarter, which was a bit better than expected, but its forecast suggests a slowdown. Apple is calling for sales growth of just mid-single digit. This is below the 7% street forecast. There were some positives in the quarter. Services revenue continue to grow at double digits. Chinese sales fell, but aren’t falling as much as before. iPhone revenues were also better. Key for the stock will be the roll out of Apple Intelligence across devices and most of the sell-side bulls thinks this will show up in the March quarter.

A low bar: Shares of Intel are popping by the most in six weeks after issuing a better than feared forecast for Q4. It’s impressive the stock is moving higher considering the CEO said sales of their AI accelerator chip are weaker than expected and they won’t hit the $500 million revenue target this year. Speaks to just how beaten up the stock is with shares down nearly 60% in 2024.

Bargain bin: I’ll watch the reaction in shares of Air Canada and Magna today. Both stocks have underperformed this year and both are trading at single-digit PEs. On the surface, Magna’s results look disappointing. Sales fell more than feared, earnings missed forecasts, and they are cutting their sales forecast for the year. But the stock is up 7% in the pre-market. Scotia’s Jonathan Goldman says there were three positives in the quarter. A measure of adjusted profit came in higher than expected, the 2024 forecast cut was not as bad as feared, and the company announced its resuming share buybacks which is a lot earlier than investors expected. Air Canada is flat for the year, but has perked up recently up 26% from the low in August. Today’s results showed sales that didn’t fall as much as feared, smaller increase in capacity and higher “load factor” than expectations (percent of the plane that is filled). Air Canada is also increasing its profit forecast on a better cost outlook and more restrained capacity growth. They also announced a buyback to buy up to 10% of the public float. This will be the first buyback since before the pandemic.