BRAND NEW EPISODE: AI’S DEBT FUELED GROWTH

The AI boom is being financed with debt—and the numbers are staggering. The world’s biggest tech companies are spending hundreds of billions of dollars to build the infrastructure behind artificial intelligence. But while investors focus on the stocks, Brian Carney, Portfolio Manager at Mawer Investment Management, is watching the credit markets—and he sees risks most investors are ignoring.

Looking to invest in high-quality companies without high fees? The HAMILTON CHAMPIONS™ suite of ETFs offers exposure to diversified portfolios of equity champions across tech, financials, utilities, and dividend strategies, all with a low 0.19% management fee, designed to help you stay invested with confidence for the long term. For more information on the HAMILTON CHAMPIONS™ suite, visit: www.hamiltonetfs.com/hamilton-

Here are five things to know:

Another day: US stocks are recovering this morning after a sell-off yesterday while the TSX looks set for another day of weakness. The big show in the US will be Micron earnings today after the bell which has been one of the hottest and, increasingly, volatile names around. Options markets are implying a 14% swing in the stock. I own Micron. Looking back at yesterday’s weakness, it was interesting to see consumer staples catch a bid on both sides of the border. In Canada that was largely due to Couche-Tard surging 11% to a record high after strong quarterly results. In the US there was no such earnings boost, rather a sector that is finally getting some love. The sector is littered with cheap names and high dividends but many with bad balance sheets and weak growth prospects. I’m on the hunt for “bad getting better” stories – I’ll let you know if I find a worthy one. Better yet, let me know if you have a candidate! TSX was hampered by weakness in energy and materials. Oil continues to fall, trading at the lowest level since a week after the war in Iran began in March (see chart below). What happened to the geopolitical premium everyone said would be in the price? Right now the market only thinks that needs to be $6/bl above pre-war levels. The energy stocks have suffered, but not as much as the drop in crude. In other news, the folks over at the Dow Jones Industrial Average are booting Verizon and adding Alphabet. Probably about time given Salesforce is part of the Dow but Google hasn’t been. This now makes 4 Mag 7’s that are in the index (Apple, Amazon and Microsoft are the others).

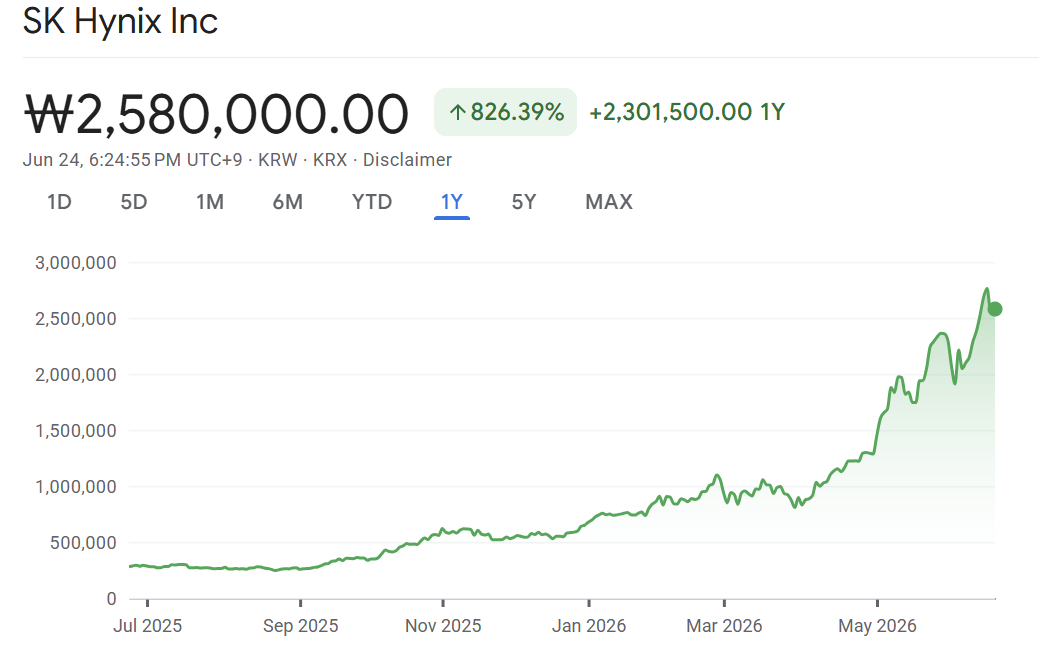

Joining the casino: SK Hynix announced plans for a US listing in an effort to raise nearly $30 billion. The South Korean memory chip maker, which makes up 30% of the KOSPI, is looking to get its piece of the AI gold rush as companies race to finance themselves in either equity or debt markets. A listing of that size would be one of the biggest in history and give North American investors access to the leading high bandwidth memory chip maker in the world. Despite it’s dominance in the hottest part of the memory market, the company trades at a discount to peers like Micron and other chipmakers like Taiwan Semiconductor.

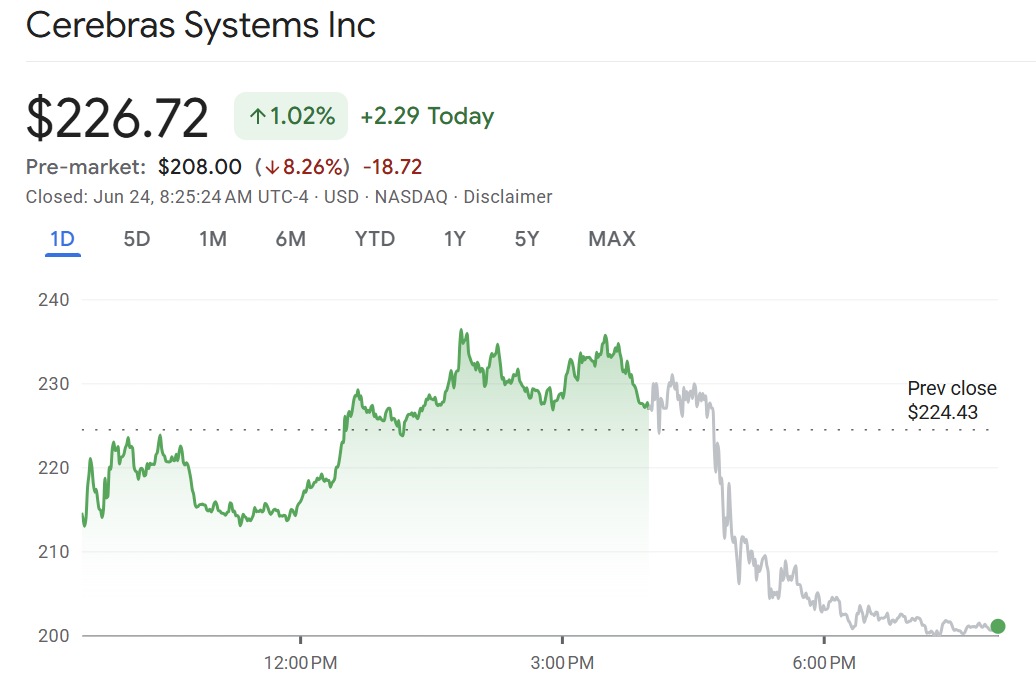

Hazing: Cerebras Systems is plunging 10% after its first quarterly results as public company. The AI chipmaker known for the speed of its technology went public in May at $185/share. Sales increased 94% from last year which was higher than expected this quarter and its loss was much smaller. Headlines say the forecast was disappointing but it was actually higher than consensus. So what gives? The debut for Cerebras coincided with a spike in volatility for the semiconductor sector – one measure shows volatility has increased to the highest level since Liberation Day in 2025. “We’re not sure why the stock was down after hours, as simply nothing in these numbers was disappointing, but we expect normal volatility for a relatively thin float; we see significant open ended growth opportunities, and find the stock compelling,” wrote Joseph Moore of Morgan Stanley.

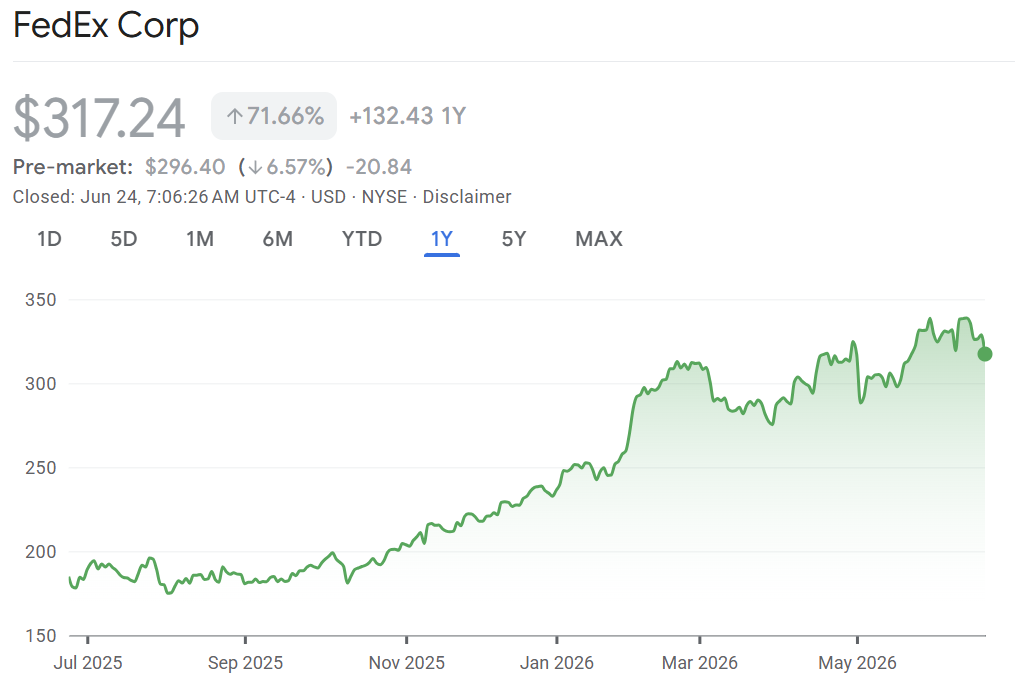

Overnight delivery: FedEx is dropping 6.5% after its profit forecast came in below expectations. Some of this is a bit messy because they are changing to calendar year reporting after spinning off it’s less-than-truckload business. In the reported quarter, profit and sales came in higher than expected. Express shipping revenue increased 14%. FedEx has been in the midst of a multiyear effort to increase sales, profit and free cashflow by streamlining its business and combining its ground and express units. The effort has paid off: FedEx is up 36% so far in 2026 outperforming rival UPS which is only up 6%. The quarter suggests the momentum is continuing and most analysts are willing to look through the noise. “…The underlying guide reinforces improving revenue quality, with management emphasizing better base pricing, premium B2B growth, and traction in healthcare, aerospace, automotive, and AI/data-center verticals,” wrote Patrick Tyler Brown of Raymond James, “We believe that change is afoot with FDX’s DRIVE program driving better margins, earnings, and FCF in out years than fully appreciated.”

Crackberry: BlackBerry has a new buy rating from Stifel and a street-high price target of $12/share (USD) ahead of earnings tomorrow. “Despite the +130% YTD move, we believe the market still misdefines BlackBerry,” wrote Stifel’s Suthan Sukumar, “This is no longer an auto-supplier story, but rather a mission-critical software layer in the physical AI stack and a dominant partner to silicon leaders like NVIDIA, Qualcomm, and AMD powering the build-out from cloud to edge, across cars, robots, factories, and medical devices.”

Don’t miss our next episode!

![]()