The AI boom is supposed to be a tech story. Larry McDonald thinks it’s a commodities story. On this episode of In the Money with Amber Kanwar, the Bear Traps Report founder and best-selling author explains why surging demand for copper, uranium, oil, natural gas and gold could create some of the biggest investment opportunities of the next decade.

Looking to invest in high-quality companies without high fees? The HAMILTON CHAMPIONS™ suite of ETFs offers exposure to diversified portfolios of equity champions across tech, financials, utilities, and dividend strategies, all with a low 0.19% management fee, designed to help you stay invested with confidence for the long term. For more information on the HAMILTON CHAMPIONS™ suite, visit: www.hamiltonetfs.com/hamilton-

Thank you to everyone who said they wanted to be part of our live audience at the Calgary Stampede – we have officially SOLD OUT after just one week! Still blown away by the number of people willing to join me at 8am when the rest of the city will be nursing a hangover. For those that can’t be there, don’t worry – our episode with Greg Ebel, CEO of Enbridge will come out on our platforms as usual.

Here are five things to know today:

At the mound: Stocks are mixed to start a brand new trading week. The headlines around US and Iran negotiations were volatile with the Strait of Hormuz is in key focus. Over the weekend, Iran said they were closing it because of Israel attacks in Lebanon. Earlier this morning, US President JD Vance said it is open. This is where I would put that “hands up” emoji in the newsletter. The markets have always been optimistic about negotiations so naturally they are taking their cue from the positive tone: oil is barely higher and stocks appear unphased. Gold continues to struggle here with no outcome seemingly helpful – might be because the US dollar is sitting around a one-year high.

Another day, another drug deal: AbbVie is buying Apogee in an $11 billion deal at a nearly 50% premium to the close last week. It’s the biggest deal in three years for AbbVie and gives it access to a promising new eczema treatment as well as other immune and inflamatory treatments. Eden Rahim of NextEdge, who is on a hot streak lately, says there is a positive read-through to Nektar Therapeutics in an email to me over the weekend. Nektar also has an eczema treatment and is up 3% in the pre-market. Nektar once had a partnership with Eli Lilly that fell apart and the stock has been punished. But he notes that Nektar is undervalued with a $2 billion market cap and $1 billion in cash.

Out of this world: SpaceX shares are down 4% and in the red for a second session in a row after announcing it would now be tapping the bond markets following its IPO last week. The “jumbo” bond offering is of mostly senior unsecured notes aiming to raise at least $20 billion with proceeds used to pay down other forms of debt. Last week, all major bond rating agencies gave SpaceX an investment grade credit rating. These type of issuances are becoming common place in the bond market – which is being asked to absorb unprecedented levels of supply. How does this all end? Don’t miss our episode tomorrow with Brian Carney of Mawer Investment Management for a focus on the AI-induced debt boom.

Hot inflation summer: Inflation in Canada soared to 3.2% in May compared to last year – the highest since 2023. Gas prices were the main culprit. When you strip those out, core inflation remains around the Bank of Canada’s target at 2.1%, albeit a tick higher than the previous reading. If you take out the effect of gasoline, inflation only increased 2.2%. Despite all the ways your can torture the data to fit the “inflation is not a problem here” narrative, the market continues to price in a rate hike in December. Inflation could get worse before it gets better, notes Andrew Grantham at CIBC. “Core measures of inflation may accelerate modestly further in the months ahead, as airfares over the peak summer travel months pick up even more of the fuel-driven price increases, and as the FIFA World Cup temporarily boosts prices in areas such as hotels and spectator sports,” he wrote in a note to clients, “However, the low starting point for core measures of inflation on a year-over-year basis should enable the Bank of Canada to look through any near-term acceleration and we continue to see interest rates on hold throughout the remainder of 2026.”

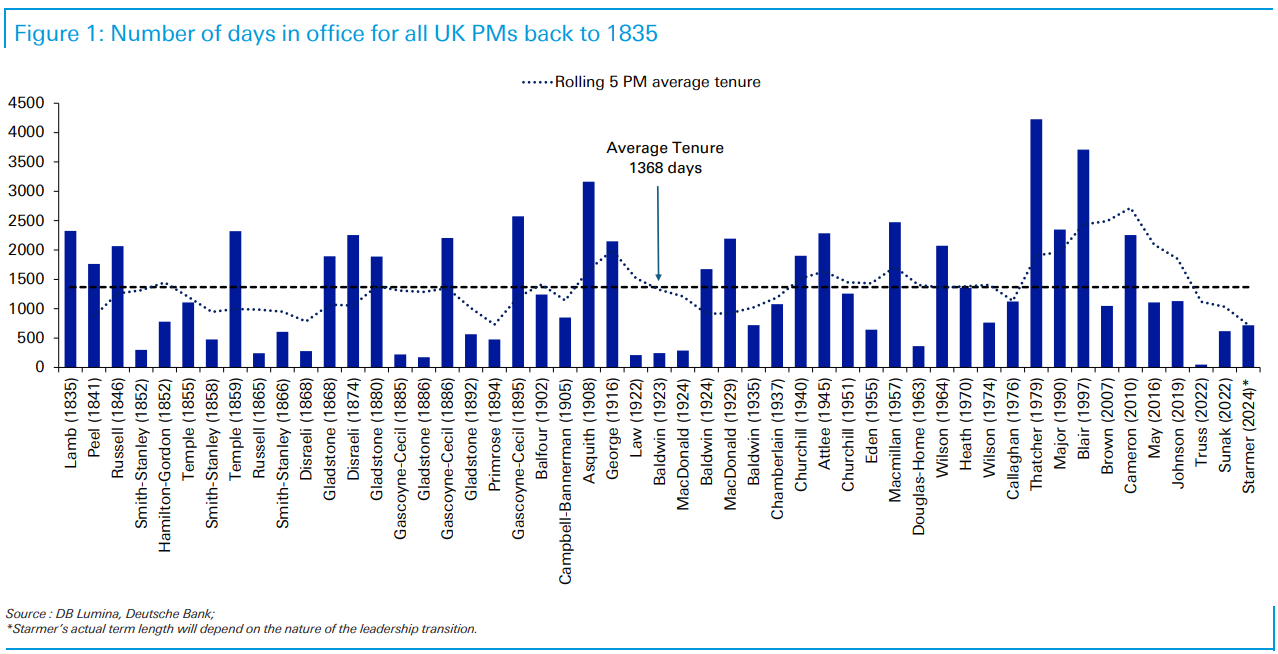

8th time is a charm: UK Prime Minister Keir Starmer announced plans to resign after the Labour Party finds a new leader to take them into an election marking the downfall of a 7th Prime Minister in the last 10 years. Naturally, the markets have a stiff upper lip about it all having seen the writing on the wall and, quite frankly, having seen this movie before. That’s not to say there is no price for this tumult: the British Pound bouncing from a three month low and bond yields have steadily risen over the last several months. Starmer’s resignation took place one day before the 10-year anniversary of the Brexit vote. “Since David Cameron resigned after the Brexit referendum in 2016, the UK has moved through Theresa May, Boris Johnson, Liz Truss, Rishi Sunak and now Keir Starmer in unusually rapid succession. The obvious explanation is Brexit, but the deeper point is that Brexit exposed structural weaknesses that the UK, like many other Western economies, face,” wrote Jim Reid of Deutsche Bank.

Don’t miss our next episode!

![]()