The oil market just got a historic geopolitical shock — and Eric Nuttall says market complacency is creating a major opportunity in energy stocks. Geopolitics has jolted the oil market — but according to Nuttall, the real story for investors was already unfolding long before the latest headlines. The Partner & Senior Portfolio Manager at Ninepoint Partners, joins In the Money with Amber Kanwar for an emergency session to break down the implications of the Iran crisis, why the market may be dangerously complacent about global oil supply, and why he believes energy stocks remain in a multi-year bull market.

In a world full of unpleasantness right now, I’ve found new joy in watching these fast food CEOs trying to convince us they actually eat their own “product.” It started with the McDonald’s CEO trying to convince us at 120lbs, he and his cashmere sweater actually enjoy eating burgers on a regular basis. I am reminded of something a marketing exec told me years ago. When the ad agency runs out of ideas, they suggest putting the CEO in the commercial. And the CEO never says no. In this case, maybe he should have!

Here are five things to know today:

Data over everything: Markets overcame geopolitics yesterday after US economic data showed the services sector expanded at the fastest pace since 2022. This morning, futures are back in the red but as we’ve seen for the last two of three trading sessions optimism takes hold after the open. The war in the Middle East continues to rage on, with Iran firing retaliatory strikes against Israel and neighbouring Gulf States. Oil is barely higher, however. This is incredibly complacency said Eric Nuttall on the podcast who explained why this conflict was different and more severe than geopolitical events in the past. The real action remains in the bond market which is anything but complacent right now. Yields are rising across the board as bond investors bet the war is inflationary and central banks will be hard pressed to ease further in this environment.

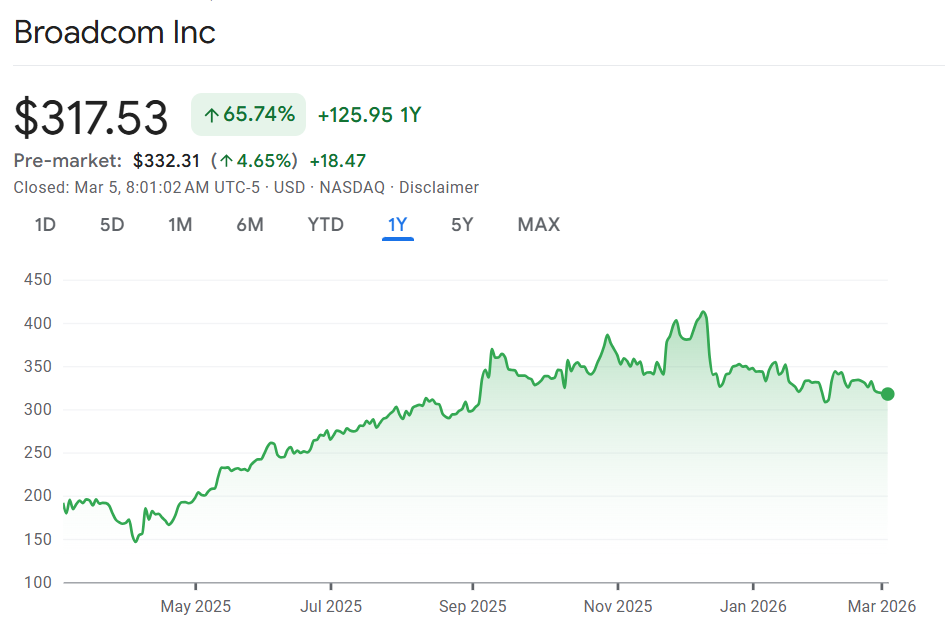

The cat is alive: Broadcom is breathing new life into the AI trade this morning with the stock popping 5% after earnings beat expectations, its AI-related revenue doubled, and it offered a rosy forecast. The chip maker said AI-related revenue can hit $100 billion by next year. For perspective, AI-related chip sales last year were $20 billion. Broadcom is different from Nvidia in that they make custom AI chips for training and running AI models. Considering the material step up in revenue projections, the stock’s pre-market rally looks quite pathetic. Especially considering the stock had been selling off into results and is actually down 8% so far in 2026. Part of that has to do with concerns about margins, customers like Google making their own chips, and the non-AI software business “stable but unexciting” according to a Morgan Stanley analyst. Yet, there is room for more upside they argue. “The quarter was strong, with AI driving upside and improved long-term visibility. Margin concerns eased, networking outperformed, and 2027 AI potential remains significant,” wrote Joseph Moore of Morgan Stanley.

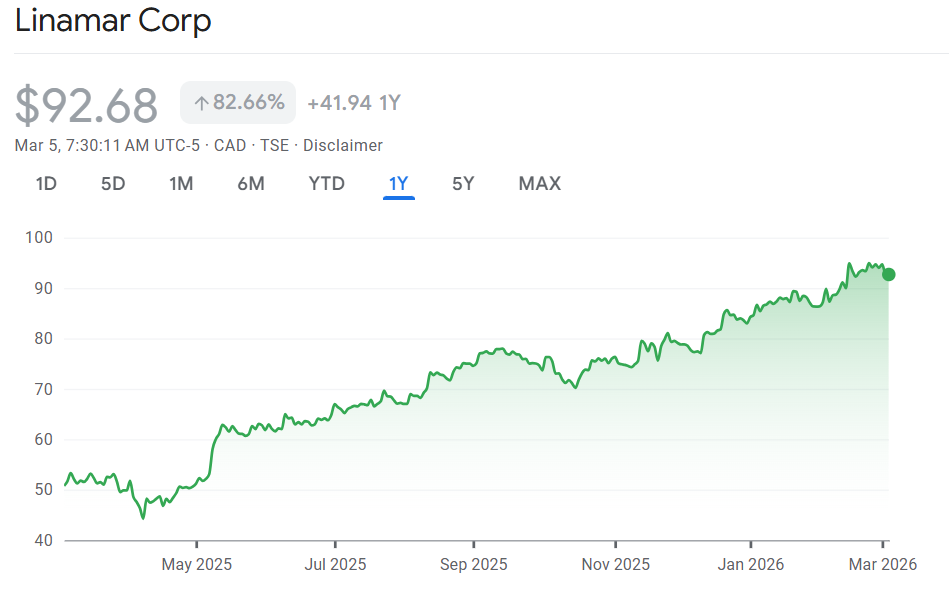

What trade war? Watch shares of Linamar at the open after it beat profit and sales expectations despite a raft of headwinds. Muted auto market? Slow agricultural segment? These are barely blips in the radar for the precision parts maker. The company exited 2025 with record earnings for a second year in a row. “Linamar results have continued to be quite strong in the face of some notable headwinds …with very strong free cash conversion,” wrote Michael Glen of Raymond James, “Clearly any concerns we have had regarding how headwinds would impact results were misplaced, as we have continued to progress with a series of positive earnings revisions.”

Flexing: Shares of Canadian Natural Resources are higher in the pre-market after profit, production and sales came in higher than expected. Canada’s most valuable energy company recently surged to a record high for the first time since 2023 and is outperforming peers in 2026 after a period of doing nothing. CNQ also boosted its dividend 6% (25 years in a row) and signaled it is prepared to send even more money to shareholders. CNQ eased the net debt threshold that needs to be met in order to pay 100% of free cash flow to shareholders to $13 billion from $12 billion previously. Nuttall called this stock ridiculously expensive and not a name he owns right now. I own it.

Energized: Watch Tourmaline Oil after a mixed set of results. Cash flow per share beat expectations and it cut its capital spending plans by $400 million. However, the production forecast was lowered slightly and the company said there would be no special dividend in the first quarter because of lower natural gas prices. “Overall, we view the event as modestly negative,” said ATB Cormark’s Patrick O’Rourke in a note to clients. I’m a shareholder. Surge Energy will also be in focus after it missed cash flow per share estimates. Nuttall was quite negative about this name on the podcast. Lastly, watch Vermilion Energy cash flow per share came in significantly above expectations. However, TD is downgrading the stock saying it is fully valued here after nearly 40% surge in the stock so far this year.

Don’t miss our next episode on small-caps! Email questions@inthemoneypod.com

![]()