CI’s Asset Allocation ETFs provide access to globally diversified portfolios in a single trade – designed to simplify investing across market cycles. Their Plus ETFs extend this trusted all-in-one approach by adding a small, permanent allocation to Gold and Bitcoin, helping portfolios adapt to today’s economic realities without sacrificing simplicity. Now available for a limited time with zero management fees. (Available until June 30, 2026)

It is a can’t miss week in the markets. There are five major central bank decisions and five mega cap tech earnings on deck. Read all about the week ahead in my Globe and Mail column.

Here are five things to know today:

Burden of proof: It’s a quiet start to a busy week and North American stock markets are flat this morning. As the war enters its 9th week with no clear resolution in sight – yet the possibility of a resolution at any moment – a few notable trends are developing. First, the US is outperforming again. After ceding dominance over the past two years to global markets, US markets have been quietly outperforming over the past month. Tech stocks have come roaring back. Tech is underperforming commodities in 2026 but over the past month that trend has reversed and tech is handsomely outperforming commodities. Second, oil prices are actually down over the past month. Yes, they are well above pre-war levels, but even without a resolution to the war they haven’t continued to ascend. Why? Ed Yardeni of Yardeni Research says there are a couple of reasons. First, supply is moving through alternative routes. This doesn’t offset the supply gap, but it helps to narrow it. “About 7 million barrels per day (mbd) are going through the pipeline bypasses currently versus the 17-20 mbd shipped through the Strait before the war,” notes Yardeni. Second, emergency Iranian and Russian oil supply “at sea” was accessed to help narrow the shortfall. Third, the cure for higher oil prices is higher oil prices. There is some demand destruction taking place. While much of this can be viewed as a “bandaid” to the current crisis – sometimes bandaids do the trick.

Open season: Arc Resources has agreed to a takeover from Shell in a deal worth $22 billion in a mix of cash and stock. The offer price of $32.80/share is a 27% premium to Friday’s close and a slight premium to the highs over the past year. Arc Resources has been a laggard because it struggled to ramp up its Attachie asset on the timeline investors were expecting. Shout out to Rebecca Teltscher of Newhaven Asset Management who had this as a Pro Pick on February 26th. At the time she said that Attachie issues would be worked through and perhaps Shell’s acquisition of the company demonstrates they believe that too. Shell has a long history in Canada but over the last decade has pivoted away from oil sands and more toward LNG prospects. It sold the bulk of its oil sands assets to Canadian Natural Resources 10 years ago. Today Shell Canada owns a 40% working interest in LNG Canada. “Hollowing out of Canada continues,” wrote Eric Nuttall of Ninepoint Partners when reached for comment this morning. He told us he sold Arc Resources when he was on the podcast in March. “I think Whitecap is the beneficiary here,” he said, “That is where flow of funds will go. No one wants to hold Shell paper.”

ChatIRL: OpenAI is reportedly working on a releasing a phone boosting shares of chipmaker Qualcomm (+10%) which is said to be a supplier. The source of the report is actually a post by an analyst on X who said his checks indicate that OpenAI is working with Qualcomm and others to develop a device. Mass production could hit the market as early as 2028, he says. None of the companies involved have confirmed whether this is true. The response in shares could be less a function of the validity of the report and more a function of how much Qualcomm has underperformed other chip makers with any hint of good news prompting some short covering. Qualcomm fell to a one-year low at the beginning of April as its customers made fewer devices because they were dealing with the rising cost of memory chips and/or preference for spending on AI related endeavors.

Thin crust: Domino’s Pizza is falling 6% in the pre-market after profit and sales missed expectations. Same store sales in the US barely grew. Analysts were looking for 2.5% growth. Sales in international markets unexpectedly fell. The company blamed consumer uncertainty, weather and inflation for the sales woes. Domino’s says it is committed to 3% sales growth in the US and will do more pizza innovation starting in May to drive growth. Domino’s also blamed aggressive competition and promos “out of our playbook.” Clearly a sign that a consumer pinched by higher gas prices are looking for other ways to save money and eating out at restaurants suffers as a result.

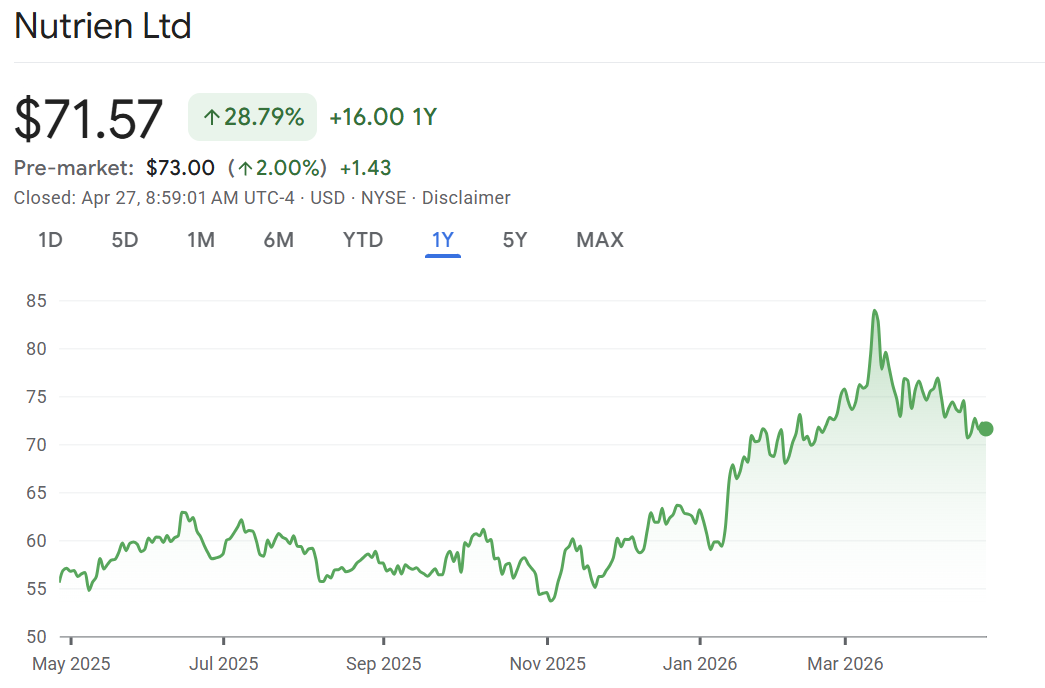

Bull fertilizer: Nutrien is up 2% in the pre-market after catching an upgrade at Barclays. The company should benefit from higher profitability associated with increasing fertilizer prices thanks to supply disruptions from war in Iran. This is not a new thesis, but it is a thesis that hasn’t played out well in the stock with shares erasing all of its post-war gains and back to where it was before the war started. The price target implies about 20% upside from here.

Don’t miss our next episode!

![]()