Futures higher ahead of the Fed, General Mills warns, Couche-Tarde beats, rating changes in energy stocks

Our daughters like to tell us how many kids they will have when they grow up. Yesterday, the middle had an update. She only wants two kids. When we asked why, she said “Three is hard to deal with.” I have never felt so seen.

Don’t miss our latest episode! Cole Smead of Smead Capital Management says this is one of the best times in 20 years to buy Canadian energy stocks. As a U.S.-based investor, he sees significant upside in the sector, pointing to supply constraints, capital discipline, and strong cash flow generation.

This newsletter is sponsored by BMO InvestorLine. The newsletter and the podcast may give you some interesting investment ideas. To help you research and potentially act on those ideas, consider BMO InvestorLine. Their platform provides the resources you need to analyze potential investments, with the valuable tools and research you need when exploring the market. Plus, you’ll find the BMO Investment Learning Centre with educational courses and videos empowering you to make informed decisions. Learn how you can earn up to $3,500 cash back when you open a new account.

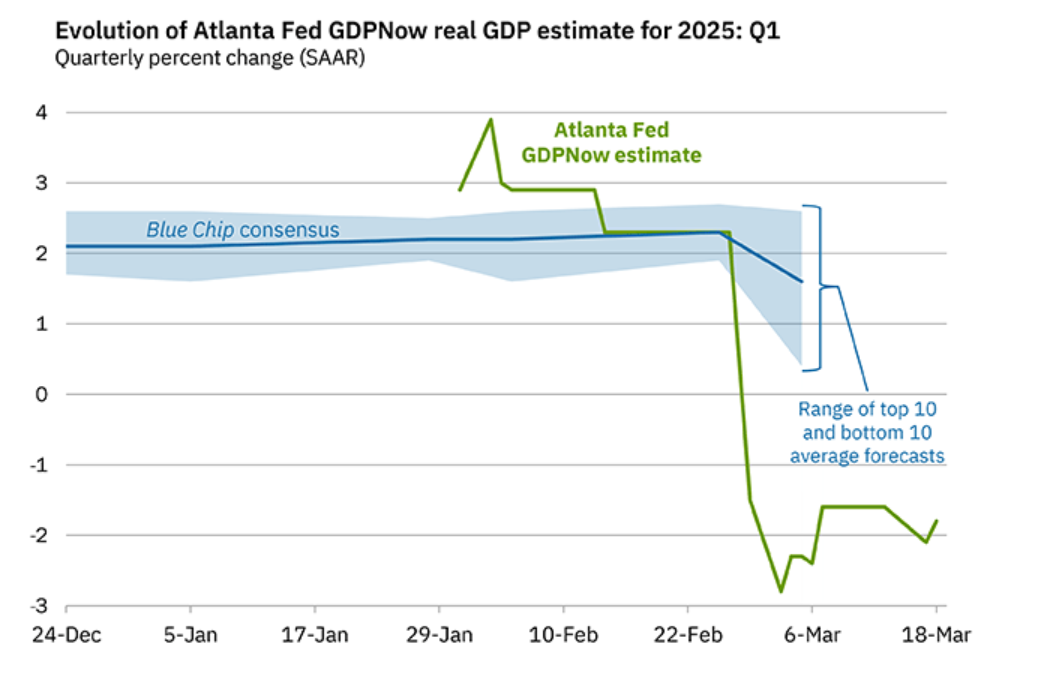

Slow play: Futures are higher this morning ahead of the Federal Reserve’s rate decision today at 2pmET. The Fed is widely expected to keep rates on hold and will likely reiterate they are in no rush to cut rates. However, indicators of growth are starting to slow down. The Atlanta Fed’s “GDPNow” estimate shows the US economy is contracting in Q1. Of interest will be the “dot plots” – the projections by Fed members of where interest rates will be this year. Right now the dots suggest another 50 basis points of easing. Yesterday, markets fell as tariff concerns weighed and there was lack progress on a Ukraine cease-fire. Amidst all these concerns, gold continues to hit new highs and outperform the tech sector. “The market is understandably fixated with how negative the trade headlines have been for US equities,” wrote Jim Reid at Deutsche Bank, “But the reality is that in February when the S&P 500 was only down -1.42%, the Mag-7 were down -8.77%. So don’t underestimate the tech sell-off as being the primary reason for US equity weakness of late.”

Snack Attack: Shares of General Mills are falling 3.5% after the cereal and snack maker cut its sales forecast for the year. Organic sales are now expected to fall 2% after initially projecting a modest gain of 1%. These projects don’t yet factor in the impact of tariffs. Consumers are pulling back on their food purchases and after years of being able to raise prices out of the pandemic, companies like General Mills are now cutting prices.

Night owl: We will watch shares of Alimentation Couche-Tard at the open after the convenience store operator showed improved sales growth in the US while organic profit turned positive for the first time in four quarters. Growth in the US is still falling, but not as much as before. “While the muted same-store-sales growth is not exciting, it is nonetheless a sequential improvement from the last five quarters,” wrote Stifel’s Martin Landry, “And better than 7-Eleven which registered a decline of -0.9% Y/Y for a similar period.” Speaking of 7-Eleven, the real overhang on the stock has been its pursuit of 7-Eleven owner Seven & i. Couche-Tard has now signed an agreement Seven & i to discuss options for its US stores. Couche-Tard wants all the stores, not just US, but this does show that at least the door has opened a crack for talks. While the stock is at a 1.5 year low, Cole Smead of Smead Capital said he would buy the dips here (57:30).

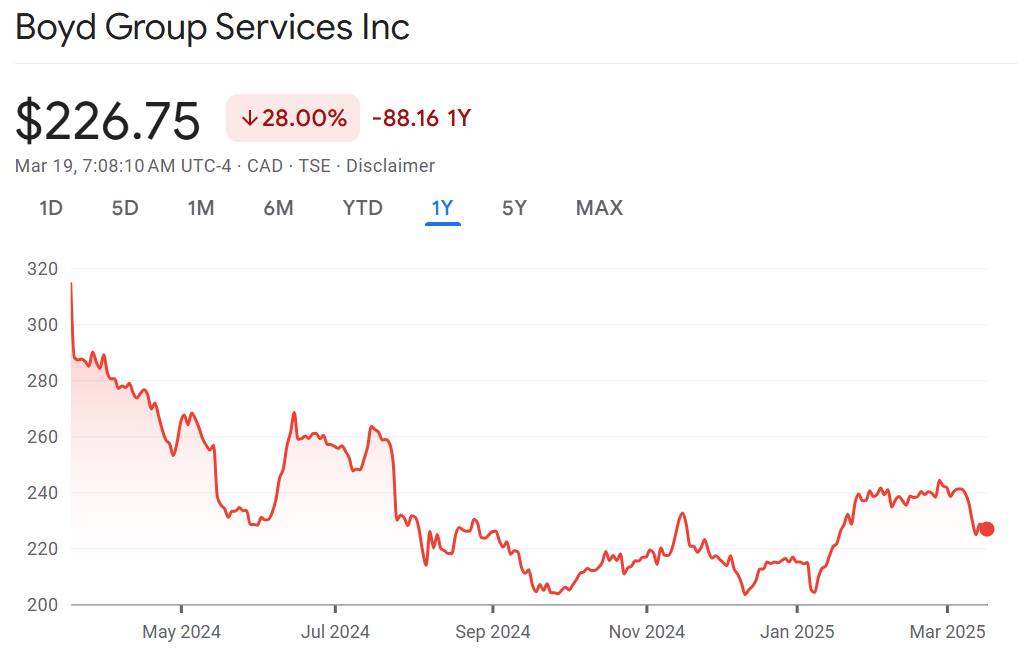

Fender bender: Watch Boyd Group at the open after the collision and auto repair company posted better adjusted profit than expected and better than feared sales growth. While sales growth is still negative, the CEO says it is starting to improve. The company is coming off a terrible year where people held off getting their cars fixed as insurance premiums rose. While sales growth is starting to improve, it hasn’t yet turned positive says the CEO. The stock is down 28% over the past year, but Bay Street loves it. There are 10 buys, 1 hold and 1 sell (Goldman Sachs).

Notable Calls: Scotia says it is time to buy Canadian Natural Resources. “Over the last 12 months CNQ has underperformed its Canadian and International large cap peers due to its tariff exposure and weaker oil prices,” wrote Scotia’s Kevin Fisk. “This underperformance presents an opportunity to buy a high-quality company at an attractive price. We have upgraded CNQ for the following reasons 1) recent underperformance is overdone; 2) fundamentals remains strong; and 3) CNQ will disproportionately benefit when the tariff dispute is resolved and/or oil prices move higher.” On the flip side, Desjardins is downgrading a bunch of energy names including MEG Energy, Tourmaline, Tamarack Valley, and Vermilion after slashing their oil price assumptions. “We have slashed our 2025–26 WTI price deck to US$65/bbl and US$60/bbl, respectively (from US$70/bbl), partially offset by our assumptions of a softening loonie and tightening Canadian oil differentials,” says Desjardin’s Chris MacCulloch. MEG Energy was one of Cole’s Pro Picks, if you are interested in a contrarian perspective (1:02:40).