Global markets keep climbing despite geopolitical tension, shifting rate expectations, and nonstop headlines—but how should you actually build an ETF portfolio in this environment? According to Ryan Lewenza, Senior Portfolio Manager, Private Client Group from Turner Investments, it all comes back to one thing: earnings. Strong revenue growth, record profit margins, and resilient fundamentals are what continue to power equities higher, even as uncertainty lingers.

Looking to invest in high-quality companies without high fees? The HAMILTON CHAMPIONS™ suite of ETFs offers exposure to diversified portfolios of equity champions across tech, financials, utilities, and dividend strategies, all with a low 0.19% management fee, designed to help you stay invested with confidence for the long term. For more information on the HAMILTON CHAMPIONS™ suite, visit: www.hamiltonetfs.com/hamilton-

Attempting a superhero mission of getting the newsletter out and getting all kids ready in time for an 8am (!!) school family breakfast. If there are any typos today, chalk it up to the number of times I had to say “Get ready!” “Brush your teeth!” “Where are your socks?” and threatening “If you do that again we aren’t going to the breakfast!” with zero credibility.

Here are five things to know:

Trillionaire: Stocks are higher and bonds are rallying after a rip roaring US session yesterday. The TSX didn’t play along with weakness pretty much across the board – energy and materials both fell. Oil prices are at a one-month low and gold has remained listless trading at a 2-month low. Strategists, meanwhile, are tripping over themselves to increase price targets on the S&P 500. This morning, Goldman Sachs is the latest to increase their target for the S&P 500 to 8,000 implying a further 6% rally from here. Semiconductors are the star of the show with Micron hitting $1 trillion market cap surging 20% yesterday after UBS said the stock could double (what part of the cycle is this?). The trillion dollar club is getting bigger by the day with 11 companies on the S&P 500 boasting membership. There are only four companies outside the US that can say they are worth over a trillion: Taiwan Semiconductor, Saudi Aramco, Samsung and – just overnight – SK Hynix. As for Canada, we’ve got a long way to go. Our whole market cap is worth less than one Nvidia and the biggest company in Canada – Royal Bank – has market cap of just $366 billion. Cute. Speaking of banks, we’ve got Canadian banks reporting with Scotia, BMO, National all out this morning. EQB reports today after the bell. Salesforce and HP Inc also report this afternoon.

Scotiabank: Profit beat expectations, net interest margins were higher (difference between what they pay for deposits and make on loans), and Canadian & international banking profit were better than expected. The rub is that provisions for credit losses were above expectations and capital markets fell short on higher expenses. Scotia boosted its dividend by four cents. Credit quality may steal focus. While provisions for losses were lower than last year, they ticked up from the previous quarter due to unfavourable macro conditions in Canada and deterioration in international tied to one account. Overall, analysts are positive on the margin expansion and strength in Canadian banking. “Came away feeling slightly better about near-term earnings momentum, but absence of balance sheet growth remains an issue,” wrote TD’s Mario Mendonca. On the conference call the company said credit losses should improve, but not as quickly as they previously anticipated. Reading between the lines: they are incrementally more cautious on credit conditions for the rest of the year. CEO Scott Thompson jumped in on the conference call and indicated that 2026 may have challenges but he is optimistic about 2027 especially given all the policy changes in Canada.

BMO: BMO shares are up 5% in the pre-market and poised to hit a fresh record high after profit beat expectations aided by lower provisions for credit losses than expected while US banking and capital markets came in better. The rub is that Canadian banking profit was lower than expected and margins were slightly worse. The better credit and strength in US is cause for celebration because these have been friction points in previous years. Indeed, loan balances were higher in the US after three consecutive quarters of declines. Capital markets was also a boon to the quarter up 46%, which was 8% better than expected. They also increased the dividend 2%. “Although there will not likely be any complaints on the performance of U.S. Retail or Wealth, we note that much of BMO‘s upside came from strong results in Capital Markets while domestic retail underperformed,” wrote John Aiken of Jefferies who rates the stock a hold, “While we do not believe that this will fully take away from BMO‘s perceived results, it does remove some of the luster.”

National Bank: Profit was slightly higher than expected aided by lower provisions for credit losses but net interest margins were worse and its Canadian business was worse than expected. Capital markets profit slipped from last year but it wasn’t as bad as feared. Profit in the Canadian business surged 169%, aided by the acquisition of Canadian Western Bank. Still it fell short of analyst expectations. Return on equity deteriorated to 11%, below bank peers. The dividend was increased 6.5%.

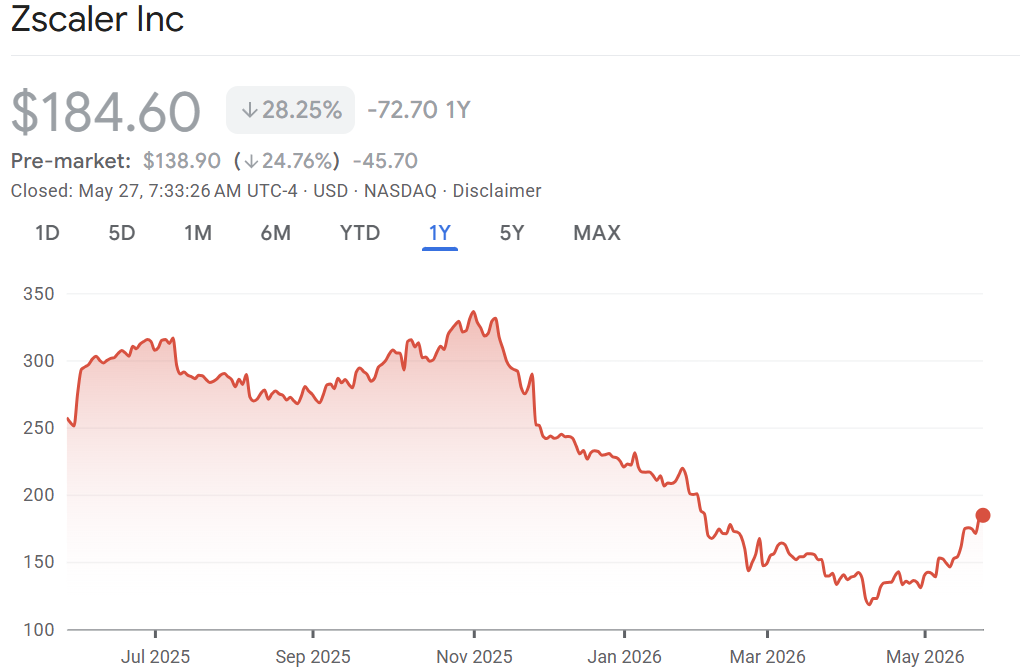

Firewall: Shares of Zscaler are plunging 25% after a tepid forecast overshadowed better than expected quarterly results. Actually, the cybersecurity company increased their profit and sales forecast, they just didn’t do it as much as analysts were hoping. In this environment where investors are skittish around software – there is no room for that. The weaker than expected outlook comes as two senior sales leaders have left the company. Evercore downgraded the stock. “Given what we view as a meaningful shift in the narrative, including a weaker than expected FY27 outlook, sales leadership turnover and the potential for broader disruption, and mgmt’s first acknowledgment of softer net new logo adds, we expect the stock to remain range bound for the next few qtrs and out of favor as the company works through these changes,” wrote Evercore’s Peter Levine in the downgrade.

Don’t miss the next episode!

![]()