Semiconductors are ripping, trillion-dollar valuations are becoming the norm, and now the most hyped IPO in years is looming. So… is this the moment everything peaks? On this episode of In the Money with Amber Kanwar, Mark Sebastian, Founder of Option Pit, returns with a view of a market that’s moving faster—and getting more crowded—by the day. From Micron’s explosive run to Nvidia’s “vampire trade” losing steam, Mark explains how capital is rotating across semis in real time—and why he’s not shorting this market, even as signs of froth start to build.

Looking to invest in high-quality companies without high fees? The HAMILTON CHAMPIONS™ suite of ETFs offers exposure to diversified portfolios of equity champions across tech, financials, utilities, and dividend strategies, all with a low 0.19% management fee, designed to help you stay invested with confidence for the long term. For more information on the HAMILTON CHAMPIONS™ suite, visit: www.hamiltonetfs.com/hamilton-

Here are five things to know:

Chugging along: Stocks are paring their losses as we head to the open thanks to a data dump out of the US. The headline is that personal spending and US GDP slowed while inflation surged to a 2-year high. None of that reads positively, but the month over month figures were slightly better than expected and that is enough for the markets. Before the reading, stocks were sharply lower as … surprise surprise … tensions between Iran and the US flared up again. Gold is down for a fourth session in a row and oil is rallying although the magnitude of both is less after the 8:30 data drop. On the TSX the focus remains on the financials with banks reporting. The reaction was pretty muted for BMO and Scotia which were flat and decisively negative for National Bank. Remember the sector is trading at record highs with premium valuation so the bar is high. EQB beat profit expectations but provisions for credit losses increased 16% from last quarter. While the company is controlling what they can with tight expense controls and better margins, deteriorating credit quality could steal focus. “With Canada’s housing market facing persistent downward pressure on valuations and resolution times, this issue could continue to weigh on EQB’s stock price in the foreseeable future,” wrote National Bank’s Gabriel Dechaine.

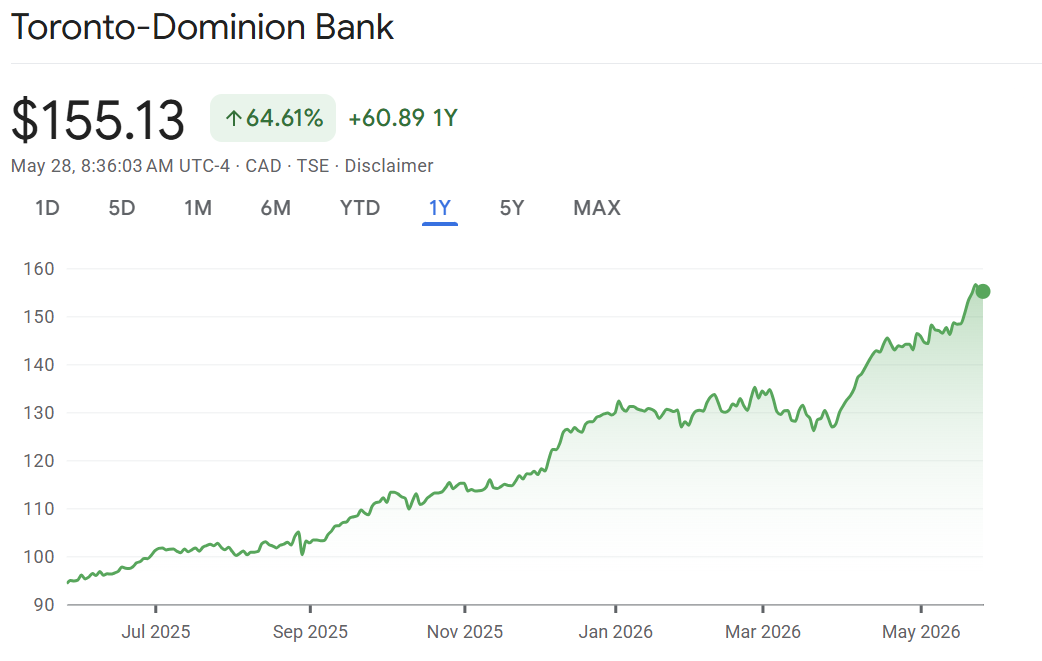

TD: TD Bank beat profit expectations thanks to better performance in every one of its banking lines, aided by lower provisions for credit losses than expected while net interest margins were better than expected. It also boosted its dividend. The bank had record earnings in its Canadian banking division as well as in wealth management. US Banking, where TD faces an asset cap due to its anti-money laundering scandal, performed well with profit up 8% thanks to strong core lending. Having said that, it just barely beat analyst expectations. “While TD did benefit from lower-than-anticipated provisions, we note that it saw solid contributions from each of its operating units, with the U.S. missing largely on the back of performing provisions,” wrote John Aiken at Jefferies, “While the contributions from insurance and capital markets may lower the quality of earnings from the perspective of some investors, we believe that the margin expansion and underlying performances in its retail banking operations are supportive.” We will see if the earnings are enough for investors given the stock is already at a record high. I own TD.

RY: A mixed quarter out of RBC this morning. On the bright side, it beat profit expectations thanks to strength in personal and commercial banking as well as capital markets. However, the beat was aided by provisions for credit losses that were 13% lower than expected and net interest margins were worse than anticipated. Wealth management also missed consensus. “While we could argue this was a capital markets driven beat, Canadian banking was essentially in line, and the credit trends were better than expected,” wrote Doug Young at Desjardins. They may not get credit for the beat if it was driven by lower provisions and higher capital markets. And it is also trading near a record high, with 16x PE (high!). Although it delivered a peer-best return-on-equity of 17.4%, better than the 16.6% expected, increased its dividend 7%, and announced a new buyback for 3.2% of the company’s float. David McKay was decidedly upbeat on the call. “I see so many positive trends in the Canadian economy,” he said. It’s a sentiment that’s been a common thread across the bank calls I’ve listened to this season. Acknowledging the headwinds around housing and trade uncertainty, but striking an optimistic tone on policy direction. Which, if you ask me, sounds a lot like an implicit endorsement of the current government.

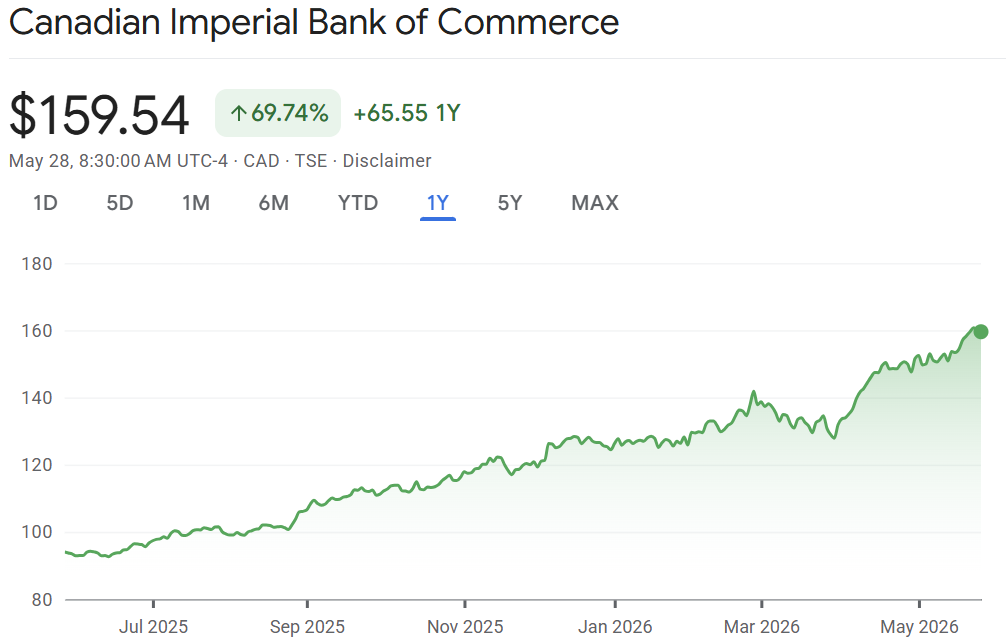

CIBC: CIBC delivered stronger than expected profit, despite higher than anticipated provisions for credit losses. Profit was driven by capital markets which surged 40% from last year and was better than expected. Margins were also higher better than expected. Concurrent with earnings, CIBC also announced the sale of its Caribbean unit for $1.6 billion. It has been operating in the region for more than a century. CIBC will own about 22% of the business after the transaction because part of the payment is in shares. Analysts are expressing skepticism that the earnings quality is strong enough to power the stock this morning. “Good, Not Great, Quarter from CIBC,” titled a report from TD’s Mario Mendonca, “Relative to consensus, earnings were weaker in CAD P&B and U.S. Commercial & Wealth,” wrote Mendonca, “A solid quarter, among best in group, but not as strong as previous quarter,” he concluded. I own CIBC.

Saassy: Shares of Snowflake are surging 37% after giving a stronger than expected outlook and announcing a $6 billion deal with Amazon. The cloud-based data platform has dropped 20% in 2026 amidst broad weakness in software stocks because AI fears. Snowflake said sales will increase 31% this year and that customers using its AI-enabled tools doubled from the prior quarter. Snowflake also said it will spend $6 billion to access Amazon Web Services and its AI data centre chips. This would make the company one of AWS’s largest chip customers. In a single quarter it went from software roadkill to AI darling. “Results are benefiting from AI tailwinds that are driving core platform value,” wrote RBC’s Matthew Hedberg, “We remain bullish as SNOW remains a tier 1 AI beneficiary.” That’s not the case for Salseforce which is falling 2% after quarterly results failed to end the debate on whether the company can benefit from AI or will be disrupted from it. Its forecast for sales was lower than expected. “These suggest organic core growth remains under pressure with minimal total revenue impact from its Agentforce and Data 360 products despite seemingly strong usage,” wrote Citi’s Tyler Radke.

You’ve seen him on CNBC, now you’ll hear from him on In the Money! Send your questions now! Email questions@inthemoneypod.com

![]()