The investing playbook may be changing—and Tyler Rosenlicht, Portfolio Manager, Global Infrastructure at Cohen & Steers, says investors need to be ready. In this episode of In the Money with Amber Kanwar, Rosenlicht makes the case that we’re moving from an era of abundance to an era of scarcity—where inflation is higher, more volatile, and driven by structural shifts like deglobalization, supply chain reshoring, and rising geopolitical risk. He explains why real assets—like infrastructure, natural resources, and commodities—could play a much bigger role in portfolios, and why now may be the time to move to the higher end of allocation ranges.

In a moment of weakness I agreed to let my eldest get press on nails. Before I opened my eyelids this morning I was being commanded to restore one that fell off. This has repeated five more times since then. Obviously I am in a mess of my own making. My husband is graciously declining to point this out, but I can tell he is thinking it. According to the Marriage Act of 1753, I think this means I can still get mad at him.

Here are five things to know today:

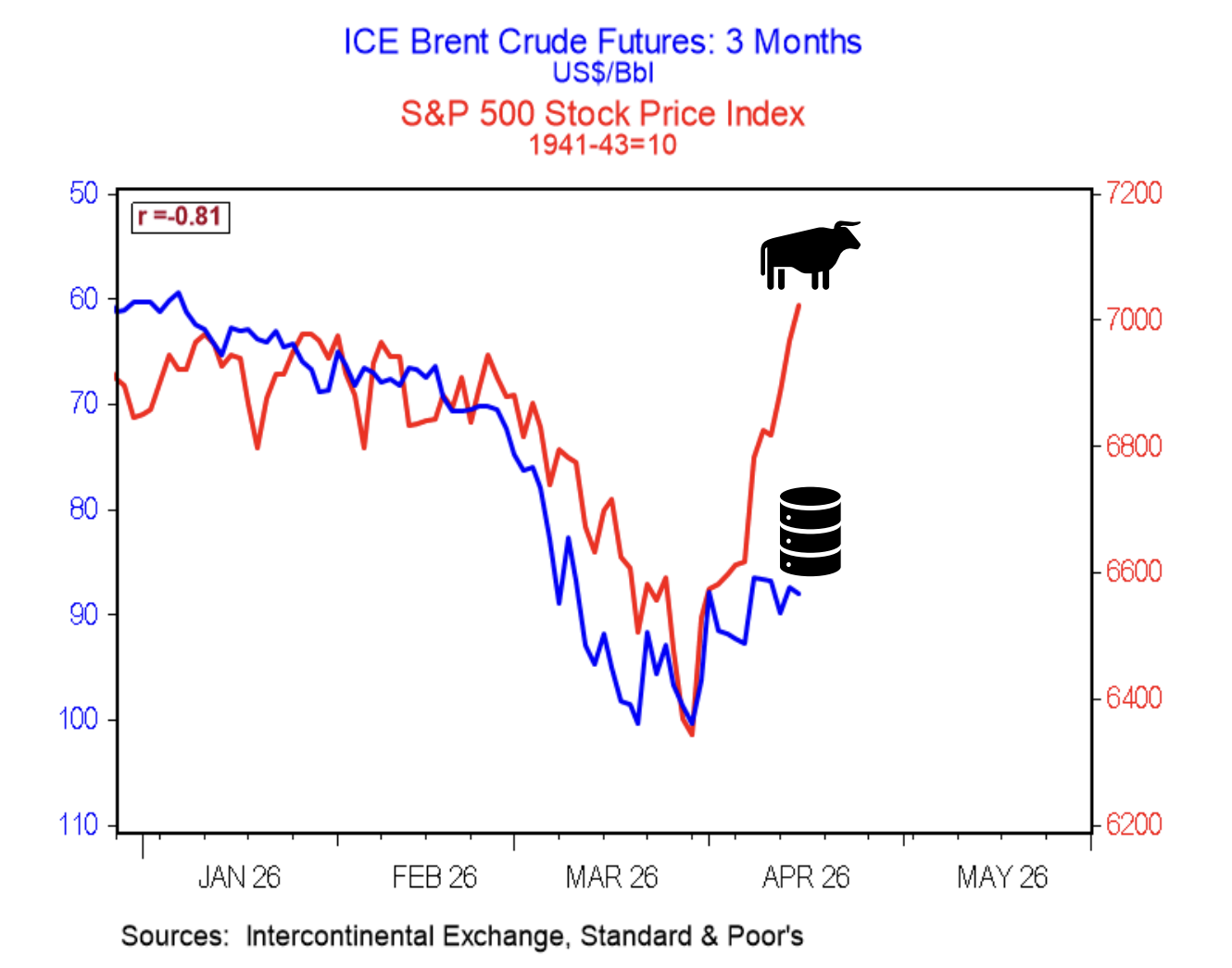

V is for V-Shaped: US markets continued their stunning recovery with the NASDAQ advancing for a 12th session in a row – the longest win streak since 2009. If it goes for 13 today it will be longest streak since 1992. The TSX wasn’t so fortunate, falling on weaker performance for materials and financials despite strength in energy. I’m also keeping my eye on consumer staples stocks. TSX consumer staples are near a 3-month low falling into a similar malaise as US staple stocks. This morning futures are higher and oil is falling as US President Donald Trump says “we’re very close to making a deal” with Iran. Trump also announced a 10-day ceasefire between Israel and Lebanon. ” After closely tracking oil prices almost tick-by-tick through March and early April, stocks have seemingly moved on (i.e., have lost interest), forging steadily higher even as oil stays stuck at an elevated level,” wrote BMO’s Doug Porter,” The charitable explanation is that equity investors are convinced the end is nigh for the conflict…although maybe someone should tell the oil market.” Despite the stunning rally in US stocks, breadth (aka the number of stocks participating in the rally) is not at extreme levels. “In January, 68% of NYSE stocks were trading above its 200 day moving average. Yesterday at index record highs that figure stood at 57%,” wrote Peter Boockvar of One Point BFG Wealth Partners.

Skip intro: Netflix is plunging 10% after its forecast fell short of expectations and it announced that its founder and chairman Reed Hastings would be stepping down. There were many positives in the quarter including higher than expected profit, double the expected free cash flow, and projections that ad revenue would double this year. The streamer recently increased prices and said those were being received well by customers. The rub in the results is that the outlook for sales next quarter came up a bit short of expectations and operating income in this quarter also missed. Investors may also be disappointed they didn’t increase their forecast for 2026 after walking away from the Warner Brothers deal – perhaps stoking fears engagement is waning. “This is a sustainable 20% EPS grower based on the following algorithm – low-teens revenue growth, solid operating margin expansion, and share repos,” wrote Evercore’s Mark Mahaney, “At 26X P/E on (2027 estimates), valuation is reasonable, with the potential for a modest rerating to 30X on a strong content slate and (second half of the year) operating margin expansion.” I bought this before the quarter and I’ll hang on to it.

Tin can: Alcoa is falling as quarterly results showed it failed to capture higher aluminum prices due to the war because of higher costs and operational disruptions. Profit and sales both missed expectations. The Middle East produces about 9% of the worlds aluminum and the war has driven up prices. Alcoa was unable to capture that because higher energy prices drove up their transportation costs. In addition, the other part of its business which refines alumina has been disrupted by the inability to access key inputs. Keep in mind the stock has also run up into the quarter +32% so far this year.

All systems go: Ally Financial is popping 3% in the pre-market after profit came in higher than expected as auto-loan demand remained robust. Despite higher gas prices, consumers are still purchasing cars and financing them through Ally Financial. Against this backdrop, the company maintained its forecasts signaling it doesn’t expect deterioration even with higher gas prices. Its an area of the market investors are nervous about, especially in light of goeasy floundering because of its subprime auto lending business in Canada. Ally Financial in the US appears to be a different beast with auto delinquencies and charge offs falling. “Overall, this was a solid quarter as performance was consistent to better across the company. We are encouraged by the continued net interest margin expansion, solid expense control, and clean credit,” wrote RBC’s Jon Arfstrom.

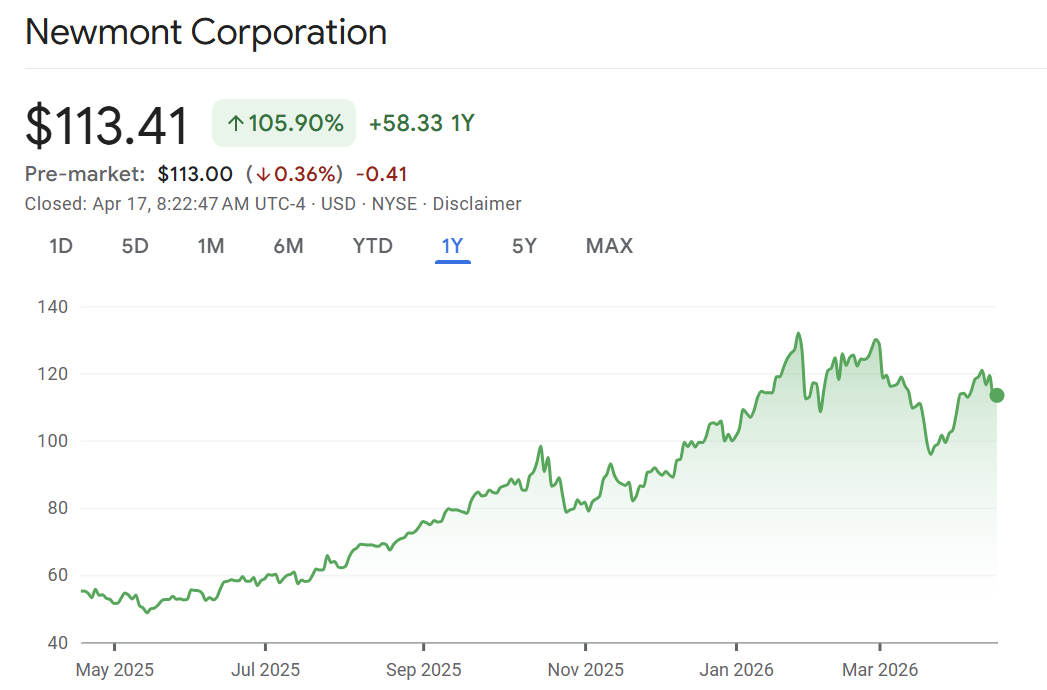

The shine is off: Newmont is underperforming in the pre-market after National Bank downgraded the stock to hold warning of elevated costs. Higher diesel prices, a new royalty tax in Ghana and paused operations at an Australian mine could all drive costs higher warns National Bank’s Shane Nagle. Profit could also be weighed down by production issues at various mines. Newmont reports next Thursday.

Don’t miss our next episode! Email questions@inthemoneypod.com

![]()