Futures mixed, Nvidia fails to dazzle, clean sweep for Canadian bank beats

If this new venture fails, I might look into a career in traffic management. Two days in a row now I have had to exit my car and direct traffic to get out of an unmoving log jam of cars as Toronto’s streets have all become unbearably clogged thanks to snow banks and bad drivers. Yesterday, I stood at a major intersection telling cars not to turn in while a truck backed up so the 15 cars behind him (including mine) could pass. I ran like mad back to my car to hoots and hollers thanking me for my service. Not all heroes where capes, but sometimes they have snazzy reflective gear.

A new episode of In the Money with Amber Kanwar is out now! Dean Orrico of Middlefield has been investing in REITs for 20+ years and says Canadian REITs are very well positioned and the sector has been unjustifiably penalized relative to American peers. We talk about what is driving REIT underperformance and he gives his three highest conviction ideas. Listen on Apple, Spotify or here.

Today’s newsletter is brought to you by BMO. We all want to make the most of our investments. That’s why BMO InvestorLine is here. Their easy-to-use platform, packed with tools, resources, and commission-free trading on over 100 popular ETFs, can help you trade with confidence and take control of your financial future. Learn more here.

Tariff Man: Futures are mixed as investors try to figure out how to react to Nvidia’s earnings beat (more on that below). Yesterday, the focus was on tariffs yet again after US President Donald Trump threatened 25% tariffs on the EU saying they were coming “very soon.” Markets dipped after those comments but still managed to finish in the green (S&P 500 +0.01% while the TSX outperformed +0.5%). At the same time, Trump seemed to move the start date of tariffs on Canada from March 4th to April 2nd. I’m struck by headlines about interprovincial cooperation. Suddenly, BC wants to work with Alberta to reduce regulatory red ape between the provinces when it comes to energy. Nova Scotia has table legislation to improve interprovincial trade. As James Alison said “give people a common enemy, and you will give them a common identity.” The TSX, by the way, is outperforming the S&P 500 and the NASDAQ so far in 2025 (see below). The European markets are star performers in 2025 with double digit gains across the board. Who knew tariff threats were so good!?

Is that all there is: Investors are struggling to bid up Nvidia after earnings beat and its forecast was higher. While profit beat, it was by the smallest magnitude in two years. Still, it is worth looking at the astonishing numbers. Nvidia grew sales by 78%, profit per share increased 82%, and the company spit out $15.5 billion in free cash. While sales growth is the slowest since Q1 2024, it is still impressive to see a $3 trillion company growing like that. The results were under even more scrutnity because of fears that with the advent of AI models, like DeepSeek that use cheaper chips, demand would be weaker. Jensen Huang, CEO of Nvidia said demand for its next generation Blackwell chips is “amazing.” What to do with the stock? There was something for the bulls (stronger growth that expected) and something for the bears (slight margin erosion, growth slowing on absolute basis). Nvidia has a big conference in March which is usually a catalyst for the stock, but this year might be different says Citi. “While (the conference) is typically a catalyst for the stock, overhang of potential new China restrictions, semis tariffs, and gross margins will likely keep the stock range bound in the near term,” wrote Citi’s Atif Malik, “For long-term investors willing to look through these concerns, valuation looks attractive at 23x CY26 EPS and stock offers an attractive entry point.”

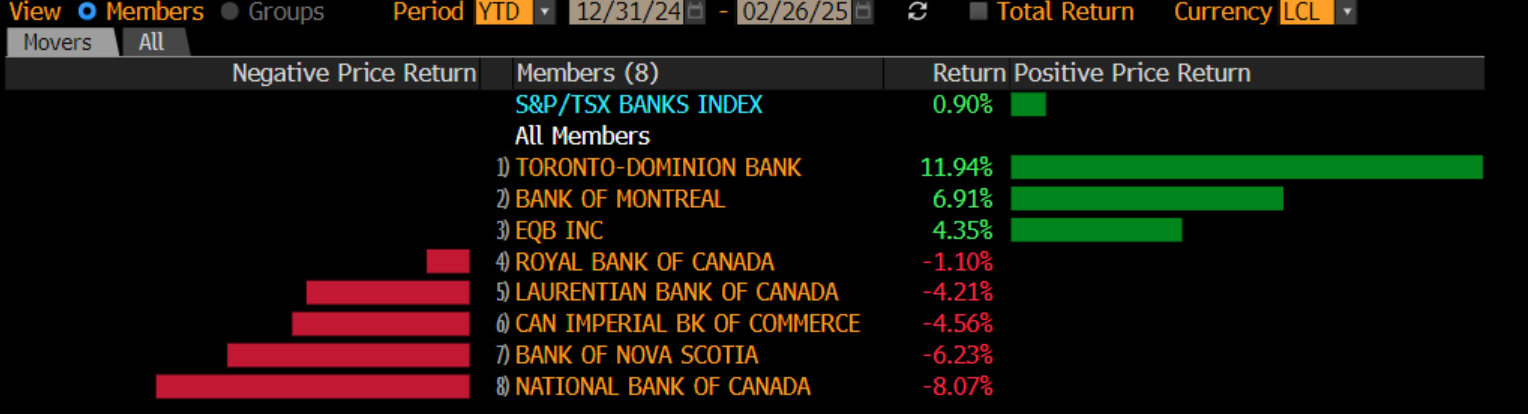

RBC: Royal Bank of Canada beat profit expectations ($3.62 vs $3.25 expected) on stronger growth across most divisions even as provisions for loans that could go bad was higher than anticipated. Like other banks, capital markets was a bright spot (profit +31%) however, as Doug Young of Desjardins points out, it only contributed to about 1/3 of the earnings beat. Investors may choose to get focus on credit quality which featured a 34% increase in gross impaired loans from last quarter. However, this is largely due to one account. “The uptick in impaired loans was a little dramatic, but it largely relates to a single account in capital markets and appears to be contained,” wrote John Aiken at Jefferies. “Outside of that, the quarter was quite impressive and, even with the incremental headwinds from provisions, Royal posted stellar results and reported a peer leading ROE. We believe that the results further highlight why Royal trades at a premium valuation,” he wrote.

TD: TD Bank reported better than expected profit ($2.02 vs $1.96 expected) but the details under the hood are a little fuzzier. Expense growth was higher than revenue growth and the bank warned that expense growth would be elevated next quarter as well. This comes after the bank closed a chapter on its anti-money laundering issues, but not the book. The profit beat was aided by lower than expected provisions for loans that could go bad and the strength in capital markets was not as pronounced as it was in other banks. TD is the best performing Canadian bank so far this year, but could come under some pressure this morning because of those wrinkles.

CIBC: Profit rose more than expected at CIBC ($2.20 vs $1.97 expected) on broad-based strength within the bank. Capital markets was up strongly but, unlike some of the other banks that have reported, it was not the only source of strength. Canadian banking was strong and their net interest margins (difference between what they make on loans and pay on deposits) increased. The bank increased its provisions for loans that could go bad to reflect tariff uncertainty. However, CIBC was still able to beat profit expectations despite the increase. “CIBC’s consistently good (profit) growth, capital strength (bought back 3.5mm shares), and steady credit metrics support a higher relative P/E,” wrote TD’s Mario Mendonca.