Bullish Brian Belski is back—and yes, he’s still bullish. In this episode of In the Money with Amber Kanwar, the CEO & Chief Investment Officer of Humilis Investment Strategies—fresh off launching his own firm—explains why he still believes the U.S. is the best stock market in the world, with Canada a close second. Belski makes the case for an earnings-driven market where stock picking, discipline, and long-term thinking matter more than macro noise. He also explains why he’s underweight the MAG 7, why U.S. banks look unfairly punished, why risks are building in private equity and private credit, and why that could create a major opportunity in small- and mid-cap stocks.

Looking to invest in high-quality companies without high fees? The HAMILTON CHAMPIONS™ suite of ETFs offers exposure to diversified portfolios of equity champions across tech, financials, utilities, and dividend strategies, all with a low 0.19% management fee, designed to help you stay invested with confidence for the long term. For more information on the HAMILTON CHAMPIONS™ suite, visit: www.hamiltonetfs.com/hamilton-

Shorter today, running to a doctor’s appointment!

Here are five things to know:

On second thought: Stocks are giving back some of yesterday’s gains as the Strait of Hormuz remains effectively closed and fighting between Israel and Lebanon threatens a fragile ceasefire. An American delegation led by Vice President JD Vance will be heading to Pakistan for peace negotiations on Saturday. Oil is once again flirting with $100/barrel this morning. A new report from Goldman Sachs warns this is the new normal if the Strait remains shut for another month. However, their base case is that the Strait re-opens this weekend and global oil prices settle around the $80/barrel mark. To the day ahead, we will be getting the Fed’s preferred gauge of inflation (personal consumption expenditure) but it is from February before the war broke out, initial jobless claims, and the third reading of fourth quarter GDP in the US.

Crackberry: Shares of BlackBerry are surging 10% after profit and sales came in higher than expected and it offered a rosy outlook. BlackBerry shares have lost ground over the last few months, down 30% from the September peak on slow results from its turnaround effort. There were also fears about how slowing auto production would affect BlackBerry’s QNX business – which enables driver-assistance and infotainment systems in cars. Those fears were put to rest this quarter after the QNX division posted record revenue for the quarter and grew 20% from last year.

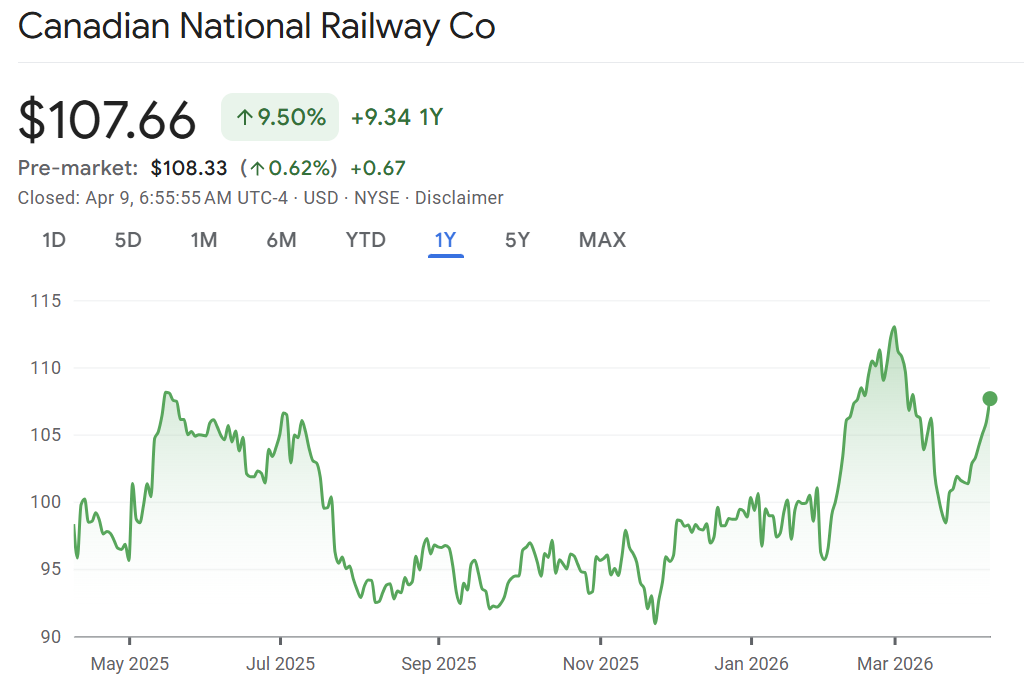

Ride the rails: CN Rail is getting upgraded to Buy at Bank of America this morning. Shares have been volatile plunging 12% in the first two weeks of March but have recovered 10% since the lows. The railway is gaining market share and is on track to exceed its full year forecasts, according to Bank of America’s Ben Hoexter. A record Canadian grain crop and better than feared intermodal and auto volumes are supporting factors in the upgrade. Hoexter also points out that CN Rail is trading a 3-turn discount to peers. I own this one.

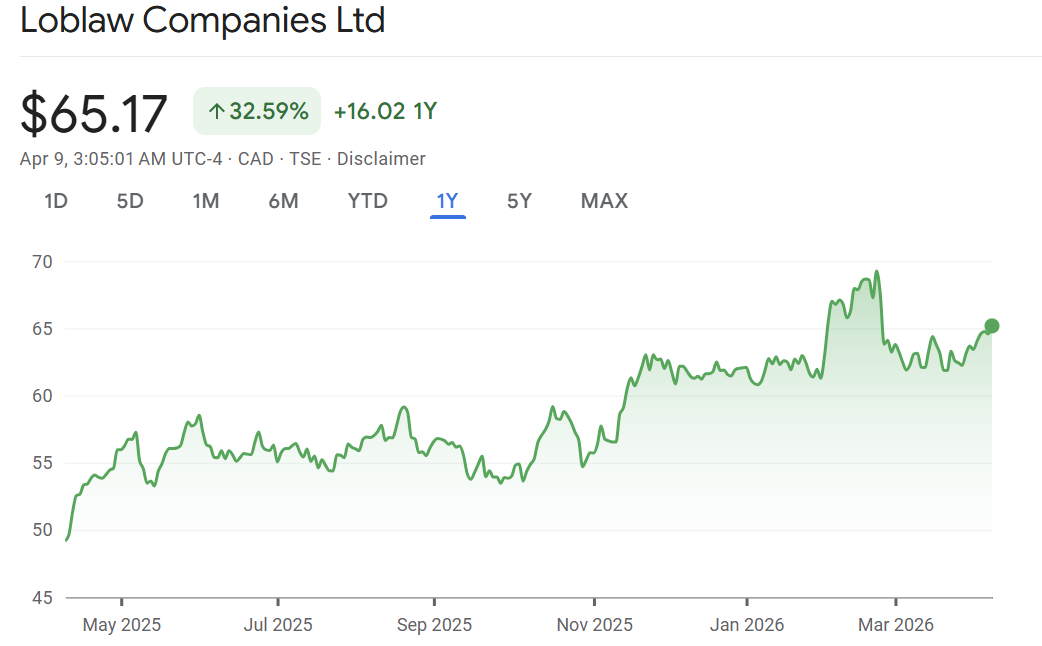

Dieting: Scotia is downgrading all the Canadian grocers this morning ahead of earnings warning of slowing same-store sales growth and lower gross margin expansion as competition heats up. “We believe near-term risks skew to the downside for the grocers,” wrote Scotia’s John Zamparo, “A product of medium-and-short-term outperformance, lower expected core earnings growth this year, and recent results that missed on key metrics, which could signal a more competitive environment than we have been expecting.” Zamparo is downgrading Loblaw, Metro, and Empire to hold from buy. Industry data show that consumers are holding up quite well, but that Costco is the main beneficiary while the grocers underperformed.

Sobering up: Constellation Brands is under pressure in the pre-market after warning that profit will be softer than analyst expectations. The beer and wine distributor said sales are still projected to barely grow and could still fall 1% for the full year. This is overshadowing quarterly results that came in better than expected. Citi’s Filippo Falorni says the outlook is “likely conservative” and sees upside. “Overall, while the initial FY’27 beer topline & EPS guidance were lower than expected,” he wrote, “We believe they embed healthy conservatism (not surprising given a new incoming CEO) and create a favorable set-up considering the beer F1Q’27 momentum & easier comps ahead.” Falorni believes the stock could turn positive today after the conference call.

Don’t miss our next episode! Get your questions in now! Email questions@inthemoneypod.com

![]()