Small caps are finally having their moment — and according to Greg Dean, Founder & Lead Investor at Langdon Equity Partners, the opportunity set may be bigger than most investors realize. In this episode of In the Money with Amber Kanwar, Greg explains why he focuses exclusively on global small-cap companies and how he searches the world for businesses that can potentially double over the next 3–5 years.

Apologies for summoning second winter.

Here are five things to know

Before times: US futures are trading lower as anxiety over Iran and oil prices overshadow a read of core inflation that came in the lowest since 2021. Core inflation in the US hung around 2.5%. However, this was all before Iran and the inflationary picture for March and beyond is likely to be very different. “…The surge in energy prices will show up in next month’s report, with the risk being that Fed cuts could get delayed, which we currently have penciled in for June and July,” wrote CIBC’s Katherine Judge. Investors also have their eye on reports that JPMorgan is marking down loan portfolios of private credit groups. Private credit has been showing signs of cracks with a recent Fitch report showing credit market defaults hit a record high of 9.2% in 2025. Next week we have the head of Canada’s banking regulator, Peter Routledge, on the podcast and he talks about his concerns around the private credit market and bank exposure. Stay tuned!

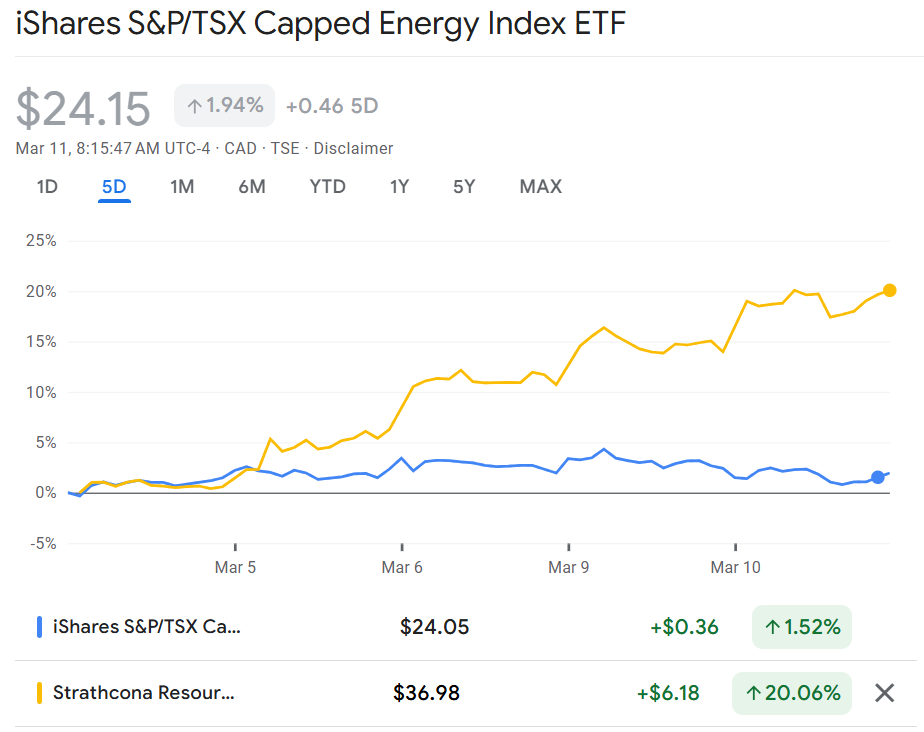

Make it make sense: Oil is trading around $85/bl right now after another wild session yesterday in which oil went from $90/bl to $76/bl within the span of a few hours. The US Energy Secretary posted that a ship successfully passed through the Strait of Hormuz which led to the decline in prices. The post was then deleted and the US Press Secretary confirmed no ship had passed. Crude was also pressured by a Wall Street Journal report that the International Energy Agency may release 400 million barrels of oil – which would be the biggest release ever. However, OECD countries consume 45 million barrels every day so it would only solve a supply crunch for a few days. A spokesperson for Canada’s energy minister says the country is “urgently exploring” ways to boost output. The energy stocks continue to be unmoved by oil volatility. Interestingly, one notable exception in Canada is Strathcona Resources which is up 22% since conflict broke out. Eric Nuttall mentioned it was one of his new buys on the podcast last week.

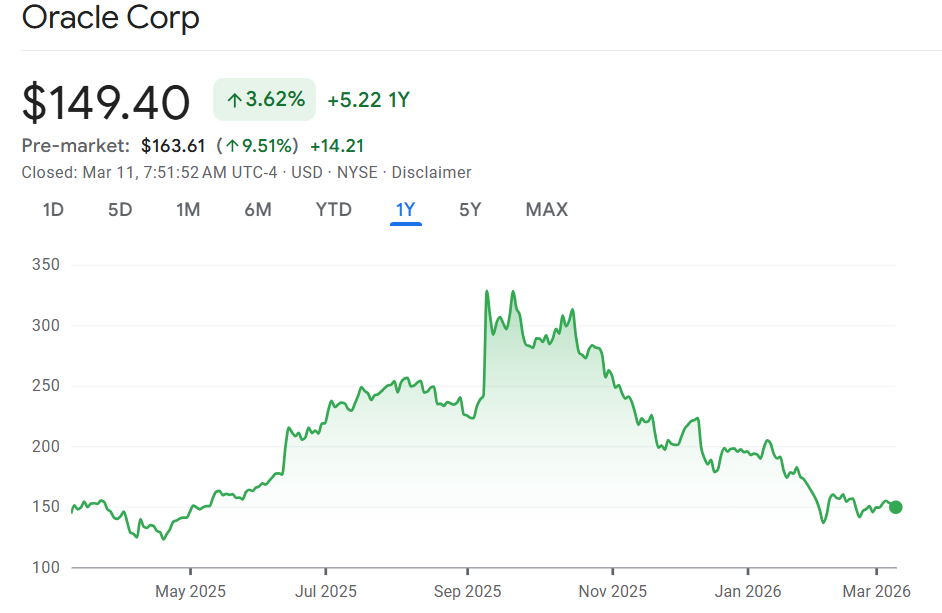

Diviner: Oracle is surging nearly 10% after sales in its cloud infrastructure division increased more than expected and it boosted its forecast. The results show there is no slowdown in demand for AI infrastructure despite pressure on the sector recently. Sales in its infrastrucutre unit increased 84%, better than the 79% expected. Spending to get that business has been a key concern and capex in this quarter came in higher than expected. However, the company maintained its plans to spend about $50 billion in capital costs. The fact they didn’t increase their spending plans could be providing relief to investors worried about their debt levels. Shares of Oracle are down 55% since the peak in September. “Finally, a clean hyperscaler print,” wrote Karl Keirstead of UBS, “Following mixed prints from cloud infra peers Microsoft, Amazon, Google and CoreWeave due to either material capex increases, lack of revs acceleration or margin concerns, Oracle posted a relatively clean print with numbers landing in-line or better and capex reaffirmed and not raised.”

Go difficult: It was a dark day for goeasy shareholders yesterday with the stock falling 57% after warning of losses in its auto-lending business, yanking its forecasts, and suspending its dividend and share buybacks. This comes 6 months after shortseller Jehoshaphat Research said the company was sitting on improperly delayed credit losses calling it a “classic subprime loan bomb.” In retrospect, there were signs. The CFO left shortly after the short report came out, then the CEO left after just 6 months on the job, and goeasy’s quarterly results were delayed by a month (official results are out March 26). This was a pound the table buy according to Jordan Zinberg of Bedford Park Capital when he appeared in November unfazed by the CFO departure and unusually lower chargeoffs. “CFOs leave all the time,” said Zinberg on the podcast and on chargeoffs he said “The business has changed quite a bit… If you have more secured lending in your book as opposed to unsecured lending, logically your charge off should move lower.” We have reached out to Zinberg to get an updated view but reviewing his interview against the news it is clear that even he did not have a sense of the full picture. Most analyst notes on the subject are repeating what has taken place with little accountability for what they missed. Although, price targets coming down and a raft of downgrades tell the story. “Our primary concern is that there may be deeper structural operational issues that could require longer-term remediation,” wrote Stephen Boland of Raymond James, “Finally, the previous CEO indicated on recent conference all that a key issue was an undersized collections department. We believe the company has limited preventive loss mitigation tools, including GPS and starter-interrupt technology, tools common among other subprime auto lenders.” RBC says this now becomes a balance sheet story with earnings less relevant. “The path forward is challenged given ratings agencies are likely to downgrade the company’s debt rating, an equity raise is difficult at current trading levels and earnings are not likely to improve meaningfully and could potentially deteriorate further if we enter a credit cycle,” wrote RBC’s Bart Dziarski. Investors don’t appear to believe this is a cockroach in Canada, with Canadian banks unfazed and trading up yesterday. Andrey Omelchak proved to be prescient in his warning against buying the dip in goeasy last week specifically because of their foray into auto lending. I still own this one.

Darling: Natural gas producer Peyto Exploration reported results last night that came in better than expected. Cash flow per share was above expectation and production was in-line with preannouncements. “Although AECO prices have not recovered following an abnormally mild winter in western North America,” wrote Chris MacCulloch of Desjardins, “The company continues to demonstrate a sustainable business model supported by an industry-leading low‑cost structure, an extensive hedge book and disciplined capital allocation.”

Don’t miss our next episode!

![]()