Futures lower, tech hit by Marvell and MongoDB results, Parkland in play

Shout out to my other half. I know he is the subject of a lot of good-natured ribbing in this newsletter, but getting our children out the door was no easy task today. I don’t know what demons took possession of their senses this morning, but that man has fought a war – all before 9am.

This is a can’t miss episode of In the Money with Amber Kanwar. I spoke with David Burrows of Barometer Capital who says a massive shift in the market is taking place – and it has nothing to do with tariffs. Unlike the current consensus which is still massively overweight tech – he barely has any exposure and talks about where leadership will come from next. It is packed with actionable ideas. Listen on Spotify, Apple or here.

Today’s newsletter is brought to you by BMO. We all want to make the most of our investments. That’s why BMO InvestorLine is here. Their easy-to-use platform, packed with tools, resources, and commission-free trading on over 100 popular ETFs, can help you trade with confidence and take control of your financial future. Learn more here.

Somewhat: Futures are indicating a sharply lower open this morning after a rally yesterday fueled by “somewhat friendly” talks between Canada and the US and a 30-day tariff reprieve for the auto sector. This morning we got a read of jobs in the US that showed a 103% jump in layoff announcements, led by cuts in the government sector. US President Donald Trump’s DOGE has been laser focused on shrinking the federal workforce. This is the highest number of layoff announcements since July 2020. Tomorrow we get official payroll data in both the US and Canada as well as speech from Federal Reserve Chair Jerome Powell. The tech sector is under pressure this morning and the NASDAQ stands as one of the worst performing global markets in 2025 (-4% so far this year). David Burrows of Barometer Capital started reducing tech exposure last summer and only has 3% of the portfolio in tech stocks. He explains why he thinks tech leadership isn’t coming back and where he thinks the next big move will come from. Semiconductor companies are all down as China’s Alibaba says it has developed its own AI model that uses a fraction of the data. Whether the claims are true or whether it works just as well is still up for debate, but investors are using it as an excuse to take profits. Disappointing earnings are also weighing on the tech-heavy index (more below).

Nothing to marvel at: Shares of Marvell Technology are plunging nearly 20% in the pre-market and poised to open at a 6-month low. The maker of custom AI chips handily beat profit expectations as data centre revenue soared nearly 80%. The problem is that the outlook for next quarter failed to live up to lofty expectations (projecting +61% sales growth, but investors wanted more). The reaction reflects a “skittish” nature around AI stock right now according to Stifel’s Tore Svanberg. Just last quarter Marvell beat expectations and soared to a record high. Loop Capital is upgrading Marvell on the pullback. “…We feel shares of compelling risk-reward consideration,” wrote Gary Mobley of Loop. Their price target is $110/share.

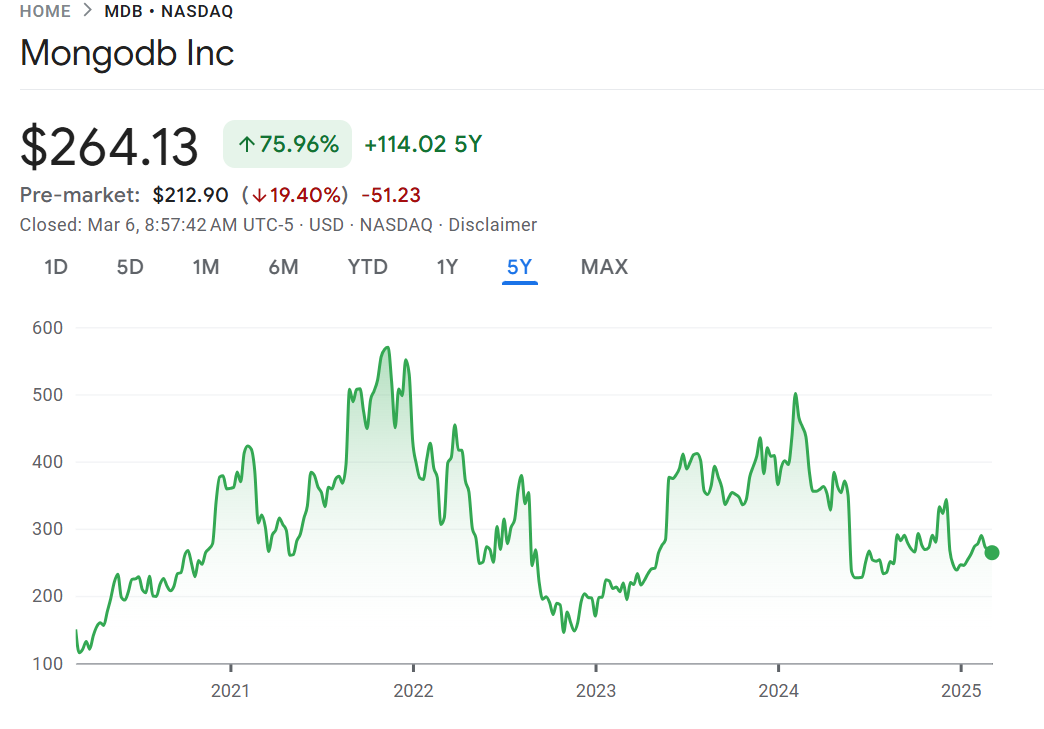

Big data: Shares of MongoDB are also losing ground down nearly 18% and poised to open at a near two-year low. The database engine beat profit and sales expectations, but like Marvell, its outlook is weighing on shares. MongoDB says sales will grow 12-14% for the year and that is lower than the 14% expected. “We are buyers of the pullback,” wrote Citi’s Tyler Radke, “as we see more prudence in guidance given ongoing CFO transition and have more conviction in upside to numbers…” he said in a note to clients. “Following the (post-earnings) stock move, shares trade at steep discount to historical valuation (NTM Ev/Sales of ~7x) and at a discount to other data/infrastructure takeout multiples,” argues Radke. Not everyone agrees. Wells Fargo is downgrading the stock. “With a smaller pool of multi-year deals, we believe it will be difficult to significantly outperform expectations in FY26 and therefore expect shares to remain range-bound,” wrote Wells Fargo’s Andrew Nowinski.

In play: Parkland is officially in play and is shopping itself around according to a release from the company. The fuel retailer has hired Goldman Sachs and Bank of America to review its “strategic options” including a possible sale amid investor pressure. It’s largest shareholder, Simpson Oil, owns about 20% of the company and has been agitating for a sale since last year. Shares of Parkland are down about 15% over the past year. The interesting part will be who kicks the tires. Rival Couche-Tarde seems set on trying to acquire Japanese-based 7/11 owner. The current polticial environment would be a test for Ottawa if a US suitor were to come knocking. “It’s worth noting, reports in August 2024 revealed PKI has turned down a takeover offer in summer 2023 of ~$45 per share,” wrote ATB’s Nate Heywood, “It remains unclear if a potential transaction would face resistance with current political tensions between Canada and the US surrounding the ongoing trade war.”

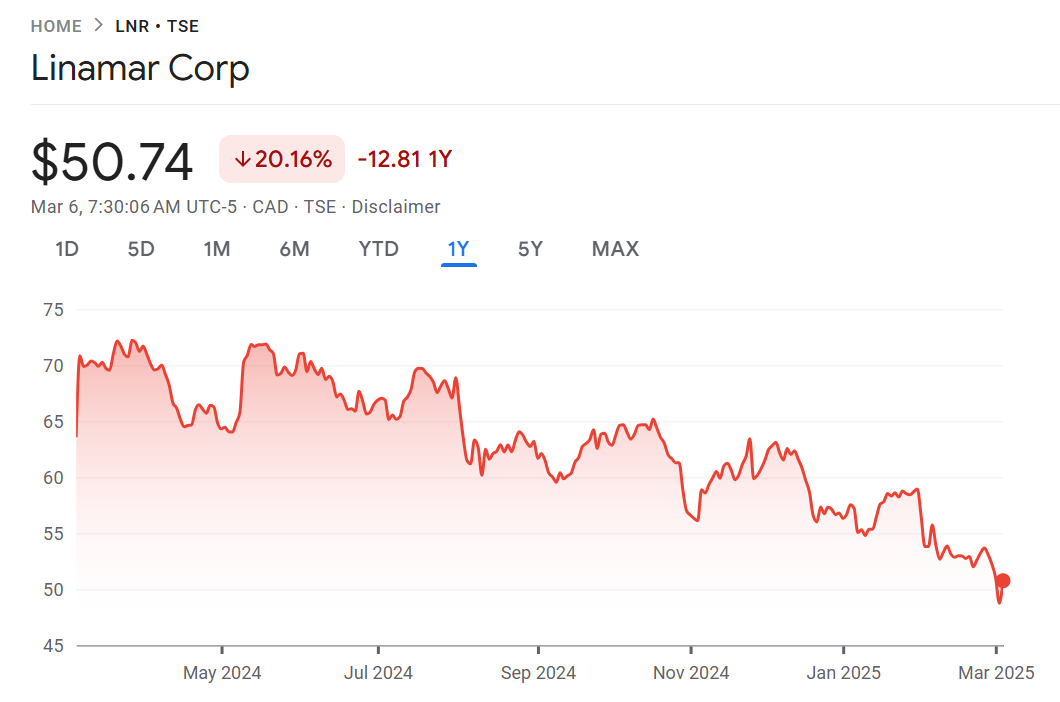

Rubber hits the road: Auto-part maker Linamar reported better than expected sales and profit in the quarter but given the tariff situation, it may not matter all that much. Linamar will no doubt benefit from the 30-day reprieve on tariffs for car makers, however management warned it is not really possible for these care makers to devise “fool-proof” tariff mitigation strategies. Linamar lowered its outlook for overall profit, sales and profit in its industrial segment, and sales outlook in its mobility segment. If you are a sucker for a cheap stock, Scotia’s got the stats for you. “Linamar shares trade at 2.8x EV/EBITDA on our 2025E, 1x below the company’s 5-year average of 3.8x, and a high DD% FCF yield,” wrote Scotia’s Jonathan Goldman, “The company has the lowest leverage among our supplier coverage (0.8x) and ample liquidity ($1.8 billion), which positions it well to be a buyer of distressed assets (particularly in Europe, as was brought up on the call) and win takeover work from struggling suppliers.”