Investors are talking about a “sell America” trade — but is the U.S. really done, or is this just another moment where global diversification finally pays? On this episode of In the Money with Amber Kanwar, Amber sits down with Jeff Elliott, Managing Director and Head of Global Equity at BMO Global Asset Management, to break down how a bottom-up stock picker is navigating today’s volatile, policy-driven markets. Healthcare takes centre stage as Jeff draws on his deep sector expertise to unpack one of the most politically exposed — and misunderstood — areas of the market. He explains why policy noise can create sharp dislocations without permanently damaging businesses, and how active managers look for mispriced opportunities across pharma, biotech, and med-tech while others retreat from the sector.

Producer Jillian and I had some downtime yesterday so we decided to go for a hike in the Arizona outback. We went at lunch time thinking it was a 45-minute excursion. Three hours later we descended – famished with only a melted Kind Bar to split between us. A testament to our friendship, we kept it together despite being very hangry and very dusty.

Here are five things to know this morning:

Softcore: Canadian markets reasserted dominance yesterday driven by higher gold prices while a plunge in software stocks weighed on the tech sector on both sides of the border. US futures are indicating another bad day for tech while other areas prop up the S&P 500 (more on that below). Why did software stocks sell-off? Anthropic, the AI platform backed by Amazon and Google, rolled out an AI tool that does legal and research work traditionally handled by paid databases. The software sector in the US plunged to an 8-month low while names in Canada like Thomson Reuters, which sells legal database software among other financial software, plunged 15%. Shopify (-10%), Descartes (-9%), TMX Group (-9%), CGI (-8%) got hammered as well. We are in “sell first, ask questions later” mode. The pain in software is also weighing on private equity companies and stock exchanges. KKR, Blackstone, and Brookfield Asset Management charts look just like the software charts right now trading around 8-month lows. First, it was concerns about real estate exposure. Now it is concerns about their software exposure. Stock exchanges, which effectively have become data companies, are also getting beaten up. TMX Group, Nasdaq and S&P Global plunged with the owner of the TSX now trading at a 52-week low. “Information Services and Exchanges stocks have sold off on renewed GenAI disruption concerns, creating an attractive buying opportunity,” wrote RBC’s Ashish Sabadra in a note to clients this morning, “as proprietary data and deep integration within client workflows—many of which are regulated—create a strong moat around these businesses that LLMs cannot easily replicate.” The big question is what does this say about the overall tech trade? Are these the first dominoes to fall or is this an orderly clean up with the market separating winners and losers? I don’t know…but we will be asking in our upcoming episodes.

I’ll clap when I’m impressed: Shares of AMD are plunging 9.5% in the pre-market despite sales and profit beating expectations on strong AI demand. The culprit here is an outlook falling short of high expectations. Under the hood there was plenty of strength with 39% growth in data-centre revenue and 34% in its PC division. “We think the stock remains in a ‘wait and see’ mode,” wrote Citi’s Atif Malik. AMD is rolling out its next generation chip in the back half of the year, “which carries execution, competitive, and customer concentration risk,” according to Malik.

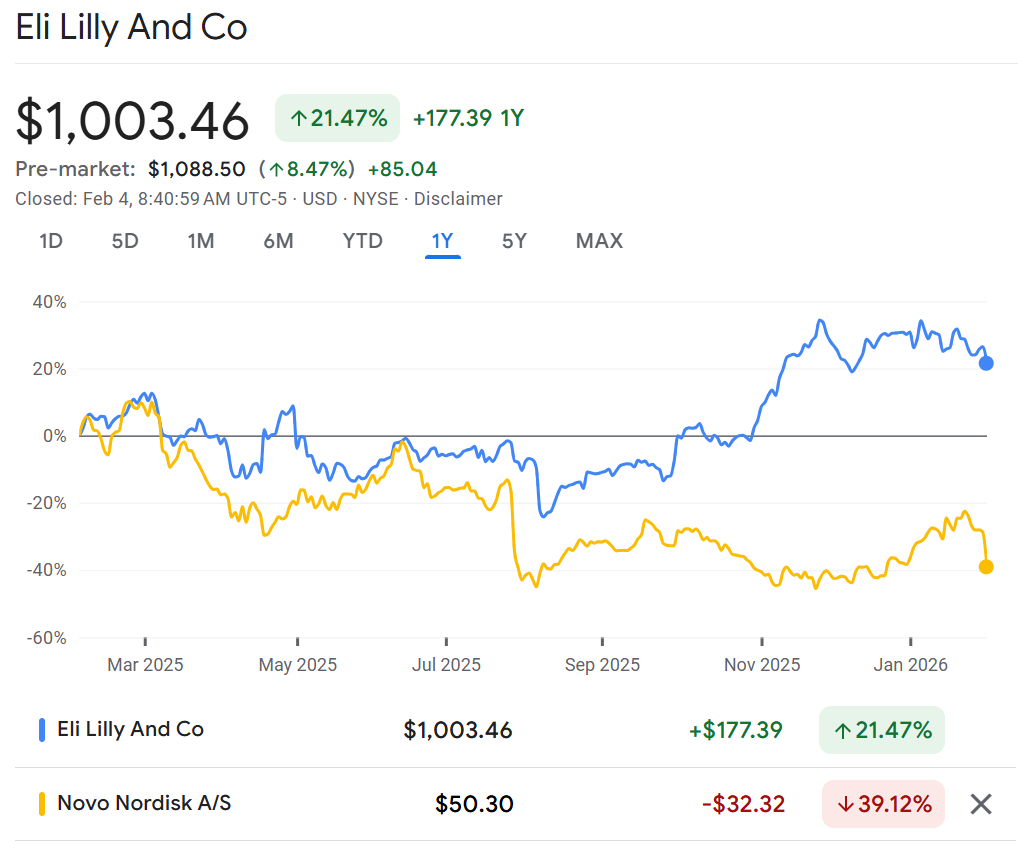

Chewing the fat: Eli Lilly is soaring 8% after results demonstrated it is clearly eating Novo Nordisk’s lunch when it comes to the weightloss market. Novo plunged 14% yesterday and is down another 4% in the pre-market after warning sales would drop for the first time since it launched Ozempic. Eli Lilly’s results this morning demonstrated why. Its forecast was remarkably upbeat, projecting sales growth of up to 27%. BMO’s Jeff Elliott gave us a sense this was going on our latest episode. “There’s just a better growth path for Lilly,” he said. I own Eli Lilly. On the flip side, he had Boston Scientific as one of his Pro Picks and it is plunging 10% after results today. Profit dropped and its sales outlook was underwhelming. Elliott is bullish on the prospects for growth thanks to its Penumbra acquisition and believes an updated product slate for atrial fibrillation (Watchman) will drive results. You can hear his thoughts on both here.

Wham-BAM: Brookfield Asset Management is up 2% in the pre-market after earnings beat expectations and it boosted its dividend 15% which is slightly more than expected. As noted above, BAM has been swept up in the private equity related software sell off. The conference call is at 10am and their exposure to the sector will be important for investors to understand. BAM raised a record $35 billion in the quarter including $5 billion for its inaugural AI infrastrucutre fund. The company also announced Connor Teskey would become CEO and Bruce Flatt would remain as Chair. Flatt says this paves the way for the next generation of leaders “who will guide the company in the coming decades. “We view the quarter positively and expect the stock to move higher today especially following yesterday’s AI/tech related sell-off which sent BAM shares down 8%, a move which we view as overdone,” wrote RBC’s Bart Dziarski.

Keep them wanting more: Suncor beat profit expectations and came out with results largely in-line with the pre-released results in January. Total oil production was a record for the quarter. “With another year of operational outperformance in the rear-view mirror, investor focus shifts toward the March 31 investor day,” wrote Chris MacCulloch of Desjardins, “We expect SU to introduce new operational and financial targets after achieving its previously outlined three-year targets one year ahead of schedule.”

Don’t miss our next guests! Father and son money manager duo!

![]()