For a preview of the week ahead, ready my Globe and Mail column on everything from earnings and government shutdown to the federal budget and economic data. Forgive my absence last week, we were on the road for the podcast. Our house was in a funk yesterday after the Blue Jays game. It was the first thing I thought about as I opened my eyelids Sunday morning. The thought was quickly replaced by my panicked daughter who came rushing into the room to tell me there was water flowing out of her bathroom on the third floor. Long story short, we had to cut into the ceiling on two of three floors of the house to deal with all the water damage. The perfect allegory to the Jays, technically intact but a little broken.

Here are five things to know today:

The hunt for red October: The first trading day of November is getting a strong hand off from October. The TSX and the S&P 500 advanced for a sixth month in a row for the first time since 2021. Bonds were also strong with the US 10-year yield trading around a 1-year low. Even gold managed to put up a monthly gain, despite the 7% pullback within the month. Silver posted its sixth month of gains in a row, the first time since 1980! Despite the US government shutdown and the lack of economic data, markets are getting a boost from earnings with 83% of companies beating expectations – this is historically high. Six of the seven Magnificent 7 reported earnings last week showing a combined 27% jump in the bottom line. This is much better than the 15% expected. This morning US futures are getting a lift from positive developments on the trade front between the US and China. The US will be lowering tariffs on China by 10% and extend relief on some tariffs for another year. China will suspend rare earth export controls and retaliatory tariffs, and buy more soybeans. Earnings from Palantir after the close could set the tone this week on the AI trade.

Merger Monday: $75 billion worth of deals has been announced this morning. The biggest is Kimberly-Clark announcing they will buy Tylenol-maker Kenvue. Shares of Kenvue are soaring as the mostly stock offer values the company around $20/share based on Kimberly-Clark’s Friday close. Kimberly-Clark is taking advantage of weakness in the stock due to the US administration linked Tylenol us in pregnant women with autism in children. Investors don’t like this for Kimberly-Clark with the stock plunging 13% (more than the typical sell-off in the acquirer). Clearly investors are nervous about what the Kleenex and toilet paper-maker is getting into with the purchase of the embattled consumer goods company. Other deals today include a gold mining: Coeur Mining is buying New Gold in a $7 billion tie up. The all-stock deal values New Gold at $8.51/share representing a 16% premium and a record high for the stock. The deal will mint a new top 10 senior gold producer with a combined $20 billion in value with assets in North America.

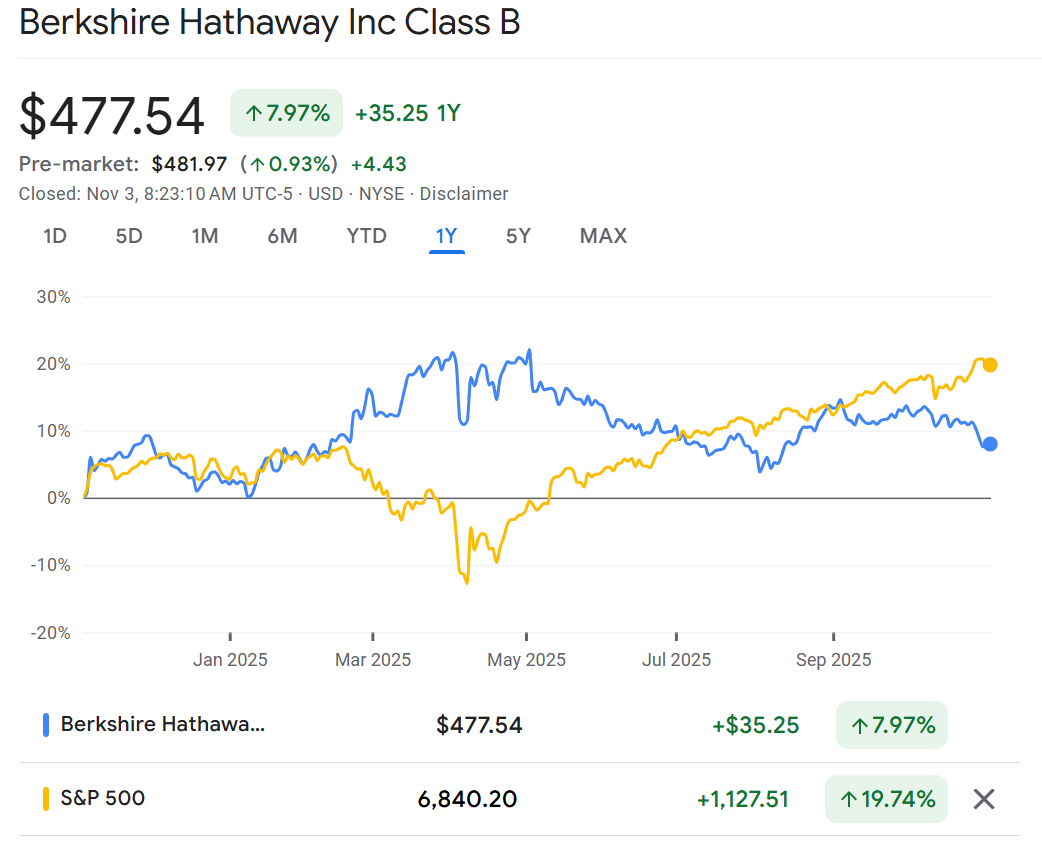

What does the Oracle know: Against a relentless bull market, Berkshire Hathaway’s cash pile grew to a record $381.6 billion and it was a net seller of stocks for a 12th straight quarter. 95-year old Warren Buffett is handing over the company with quite a war chest. But investors are penalizing the stock for the prudence, shares have underperformed the S&P 500 so far this year. Or maybe it is because Buffett will be stepping down this year and his premium is coming out of the stock. Still, earnings were solid with operating earnings up 34% and insurance profits tripled. Berkshire neglected to buyback any stock for a fifth straight quarter.

Pause: OPEC+ said they would increase oil production slightly in December and then pause adding new oil to the market in the first three months of next year. Oil is flat on the news. Fears of an oversupplied market have kept crude in check, trading below $65/bl for all of October. Russia is a complicating factor for demand after the US placed further sanctions on producers that would curb demand from other countries as well.

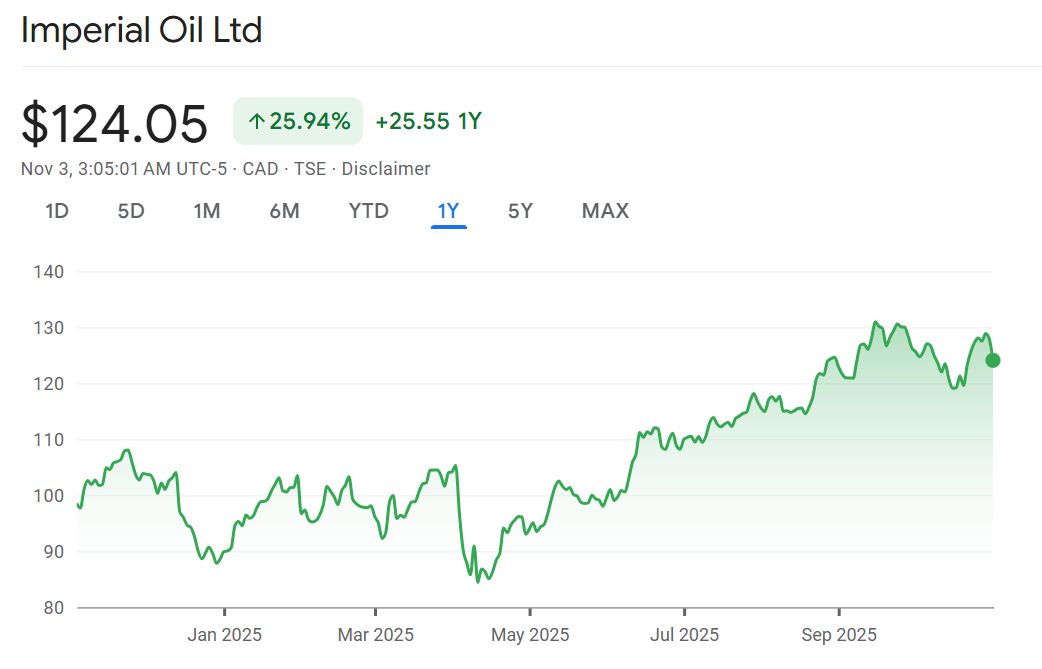

Dynasty shift: Imperial Oil was cut to sell by Peters & Co after messy results on Friday that showed a drop in profit on impairment and restructuring charges. The stock has been a massive outperformer, up 42% so far this year compared to just 16% for the group. No small feat considering crude is down 15% over the same time. Very few analysts are willing to say this can keep going, with just three buy ratings, eight holds, and eight sells.

Don’t miss our next episode!

![]()