Mixed markets, Oracle slumps, C3.ai fails to dazzle, Toll Brothers falls

Yesterday I learned one bluefin tuna can cost $100,000, sometimes more! That’s almost the same as one bitcoin. Except its useful for something.

Chop & shop: Futures are mixed after a choppy session yesterday that saw defensive sectors outperform. Overnight, we got a read of Chinese economic activity. Exports expanded less than expected while imports unexpectedly fell, highlighting the need the stimulus announced the day before. This morning, tech is a mixed bag with Oracle weighing (more below) and Taiwan Semiconductor (maker of chips of Nvidia and Apple) falling despite a 34% increase in November sales. We are light on economic data today with the big show being Bank of Canada rate decision and CPI in the US both happening tomorrow. We did get a read of small business sentiment in the US which jumped by a record 8 points to hit the highest level since 2021. I don’t think you can say the same thing in Canada.

Not enough: Oracle is pulling back from record highs this morning, down about 7% in the pre-market. Total sales increased 9% and sales in its cloud infrastructure business (read: AI exposed division) jumped 52%. Solid numbers to be sure, but in line with expectations. Furthermore, the outlook for sales, profit and cloud growth were all below expectations. Even though investors are disappointed with the forecast, RBC’s Rishi Jaluria is worried Oracle is being too aggressive in this forecast. “Management laid out an aggressive trajectory for 2H cloud growth,” Jaluria wrote in a note to clients, “Which we think investors are struggling to underwrite.” He’s got a hold on the stock.

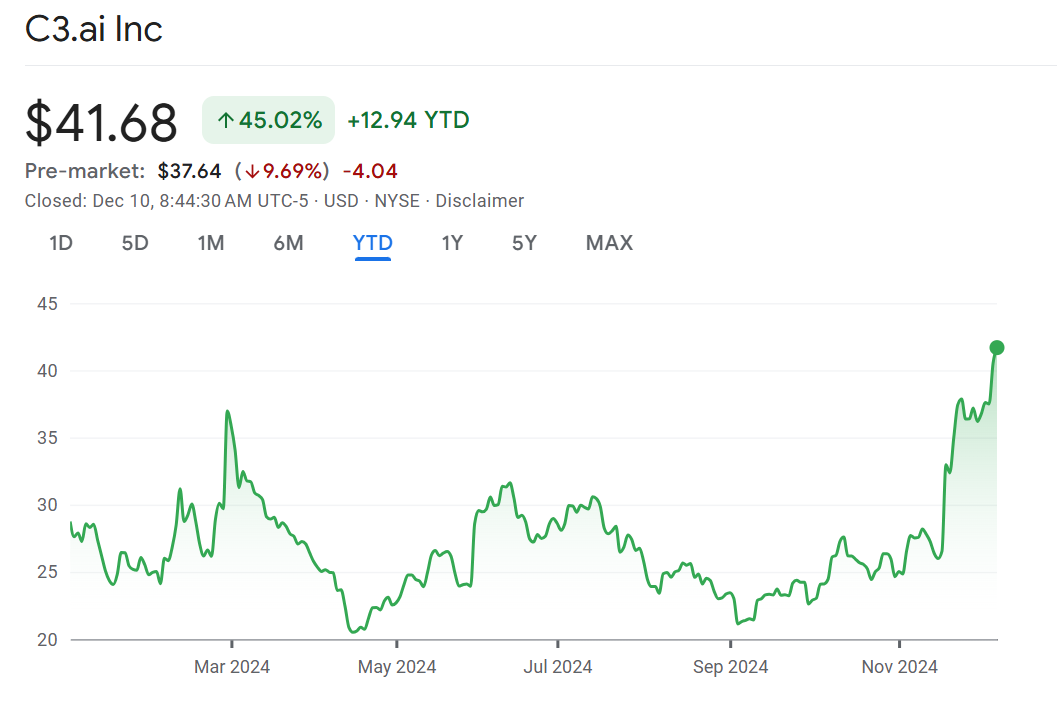

Tough crowd: C3.ai reported a nearly 30% jump in revenue, a narrower loss than expected and boosted its sales forecast in its latest quarterly results. Sounds good right? Well investors have a different view with the stock now down about 10% in the pre-market after initially surging. So what gives? First, the stock has been on a rocket ship. It is up nearly 100% since September to hit the highest level in a year. Second, while the full-year forecast was above expectations the outlook for the upcoming quarter was just in line while the loss forecast was wider than expected and the company pulled its positive free-cash flow forecast. This shows the company, which provides AI and machine learning platforms, is prioritizing growth over profitability says Arvind Ramnani at Piper Sandler. While the stock has had momentum recently, it is down 75% fom the pandemic peak. Analysts are mixed on the stock with only 5 buys, 6 holds and 4 sells (a lot for any company, let alone an AI company). Concerns are around whether their AI software is differentiated enough, their significant operating losses and low visibility into the business model according to Keybanc analyst Eric Heath. More than 20% of the shares outstanding are short the stock.

Builders: Toll Brothers is down 4% in the premarket. The luxury homebuilder warned that Q1 would feature fewer home deliveries and lower margins than expected. That is overshadowing a better-than-expected set of Q4 results on both the top and the bottom line. Buck Horne, an analyst at Raymond James, calls the results “stellar.” While the initial forecast is lighter than expected, it “…likely includes typical (Toll Brothers) conservatism,” Horne wrote in a note to clients. Shares have rallied more than 50% so far this year, so investors could be using this quarter to take some profits.

Opportunity in chaos: Social media is in a frenzy over the arrest of Luigi Mangione in connection with the assassination of UnitedHealthcare’s CEO. It is not for me to enter the fray, but I was struck by a note from Desjardin’s Benoit Poirier who speculated what this could mean for the future of air travel. “…we believe the headline-grabbing nature of the UnitedHealthcare incident could cause companies to take a closer look at flying their executives privately,” Poirier wrote in a note to clients. If companies are more inclined to buy private jets to mitigate risk, Poirier believes Bombardier could be a beneficiary with 20% of its backlog coming from these fleet customers.