Futures soft, loonie clipped, Mag-7 records, Trump trade updates, BlackBerry bump

Heading to Florida with the family this morning. We are attempting something we have never tried before: travelling without a stroller. The kids are now 7, 5, and 3 and this feels like the right time. Stay tuned for tomorrow’s missive to find out how misguided this was.

Alrighty then: Let’s hope today’s newsletter isn’t made immediately useless by the resignation of another political figure. Finance Minister Chrystia Freeland resigned from cabinet hours before the Fall Economic Statement. Serves me right for trying to stick my nose into politics. It seems obvious to everyone, except Prime Minister Justin Trudeau, that we are careening toward an election. The fireworks yesterday overshadowed a gaping hole in Canada’s fiscal situation. Canada’s budget deficit for 2024/25 is now estimated to be $48.3 billion, 1.6% of GDP. This is larger than the estimated $39.8 billion projected earlier this year. This comes as the deficit for 2023/24 ballooned to $61.9 billion. “Cumulatively, the shortfall between FY23/24 and FY28/29 is now tracking $45 billion deeper than in the 2024 budget,” wrote Robert Kavcic at BMO. On the back of all this drama, the Canadian dollar fell to the lowest level in 4.5 years. As for the markets, watch National Bank’s deal to buy Canadian Western Bank. “Yesterday’s surprise resignation from Canada’s Finance Minister created some excitement and intrigue across the political landscape in Canada,” wrote John Aiken of Jefferies, “and in our view, may have added some uncertainty to the approval timelines of the NA-CWB deal.” While ultimately Aiken sees the deal getting done, he says there is a risk it won’t close until the latter half of 2025 if there is an early election.

Bad breadth: Even thought the S&P 500 finished a whisper below all-time highs, once again there were more stocks down than up. One of my favourite strategists, Jim Reid at Deutsche Bank, has been keeping a close eye on this trend. He notes that this is now the 11th session in a row of bad breadth in the markets. “On my calculations this is the longest such run for 40 years,” he wrote in a note to clients this morning. Tech stocks are holding up the index with the Nasdaq notching a record high. Four Magnificent 7 stocks closed at new records: Amazon, Apple, Alphabet, and Tesla. Interestingly, Nvidia fell on the day, is in “correction territory” down 10% from its all-time high, and has been notching conspicuous underperformance given the rally in tech. Investors have been rotating into Broadcom which soared yesterday to a record high after Goldman Sachs raised their price target. This morning futures are lower as we await retail sales data out of the US and the Federal Reserve sits down for its two-day meeting on interest rates. Retail sales are expected to show continued strength and likely cast further doubts on the Fed’s ability to continue cutting rates in 2025. In Canada, we will get a read of inflation at 8:30amET which is expected to come in at 2% year-over-year.

Trumpdate: President-elect Donald Trump continues to make waves in the market. Yesterday, he vowed to “knock out” the drug middlemen. This sent shares of CVS Health, United Health, Cigna all lower. This morning shares of EV battery makers are under pressure on concerns that Trump will cut support for electric vehicles and charging stations. This is weighing particularly on Korean EV battery stocks which could also be on the wrong side of the near-shoring trend. On the flip side, shares of Tesla are up again in the pre-market after Mizuho upgraded the stock in part because Trump policies could favour the EV maker. I’m also tracking shares of Brown-Forman, the owner of Jack Daniels and Woodford Reserve. JP Morgan is downgrading the stock in part because of tariff risks. “While potential tariffs on imported goods from Mexico and Canada have grabbed more of the headlines recently, more pertinent for (Brown-Forman) is potential return of retaliatory tariffs on exports to the E.U. at the end of March that could double from previous levels to 50%” wrote the team.

Less is more: Shares of BlackBerry surged 15% yesterday after announcing the sale of its cybersecurity unit. BlackBerry is selling Cylance for about $120 million in cash to Artic Wolf. It bought the business back in 2019 for $1.4 billion. So, it is taking quite a bit of a haircut on the deal but “…investors would view a sale price above zero as positive, given substantial losses at Cylance,” wrote RBC’s Paul Treiber. Despite being an AI cybersecurity play and, in theory, existing in a hot market, Cylance has been a drag on profitability. Of course, BlackBerry is a shell of its former self and almost no one is talking about it anymore. But, that doesn’t mean there isn’t money to be made. From the August low, BlackBerry shares are up 46%. Treiber doesn’t recommend chasing the stock here. “Even without Cylance, BlackBerry is still seeing relatively slow growth, given its Secure Communications business and the soft auto market for BlackBerry’s IoT segment,” he wrote in a note to clients this morning. BlackBerry reports quarterly results Thursday and could surprise the market with adjusted profitability says Treiber.

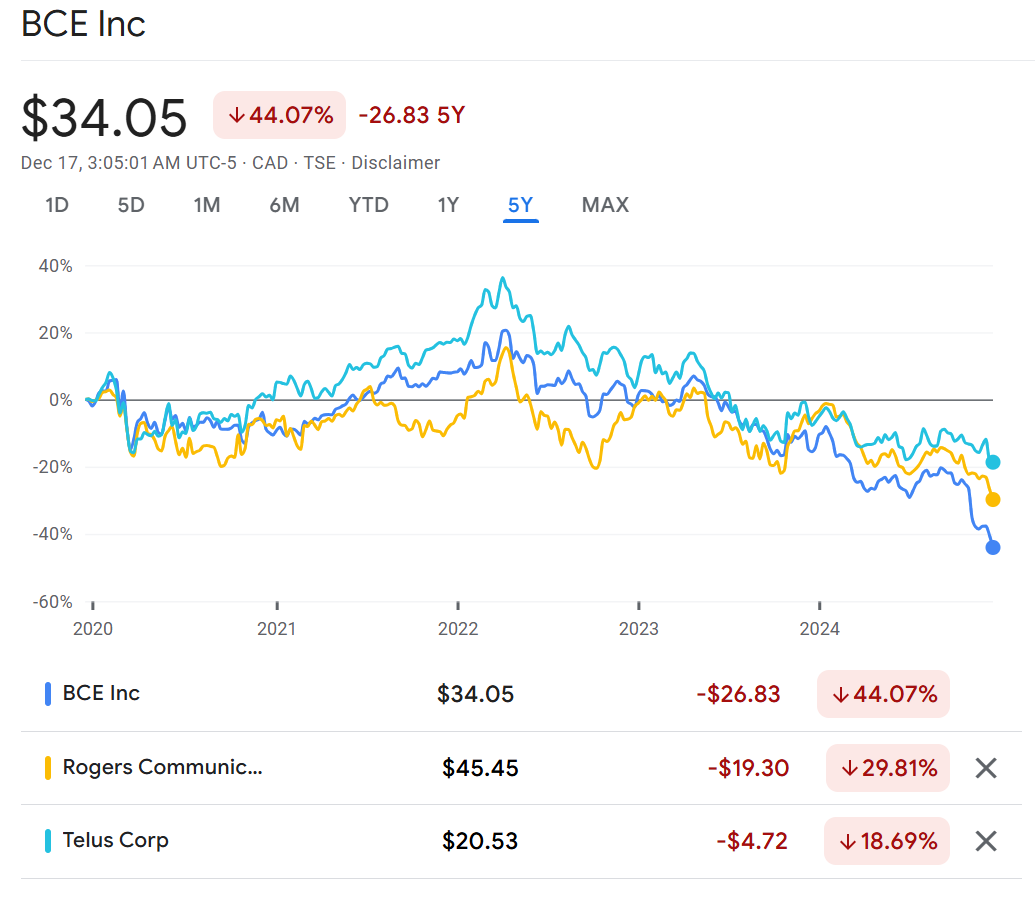

Hold the phone: Telecom stocks in Canada continue to struggle. Shares of BCE closed at a 14-year low yesterday, Rogers closed at a 10-year low, Telus closed at the lowest level since the summer. This is in stark contrast to US telecoms which are trading a couple dollars away from multi-year highs. BCE’s dividend yield is now a whopping 11.7%. Rate cuts have been no saviour to the telecoms while price competition, a hostile regulatory environment and reduced immigration have all weighed on the sector. One has to wonder how much longer BCE can withstand the market pressure on the dividend without blinking.