The Nasdaq 100 went from a seven-month low to a record high in April—posting its biggest monthly gain since 2002. But as tech stocks rip higher, Kieran Moore says the real opportunity isn’t owning everything… it’s knowing what to avoid. In this episode of In the Money with Amber Kanwar, Kieran Moore, Equity Partner & Portfolio Manager at Munro Partners, breaks down what’s really driving the explosive rebound in growth—and why he’s getting more selective, not less. He explains why AI demand is quietly surging beneath the surface, with usage (or “token demand”) tripling in just a few months, and how that’s creating massive winners—but also real disruption risk.

My husband sent me a photo of a tiny stuffed penguin tucked into the balcony door handle. It made me smile thinking about the secret lives our kids live and the little treasures they leave behind. I already feel anticipatory nostalgia for the day there’s no longer a random rock collection on my bedside table or a teeny-tiny sock in the cutlery drawer.

Here are five things to know:

All in: Stocks are higher this morning and oil is edging lower, although still above $100/barrel. While stocks are content to ignore higher oil prices, the bond market isn’t. The US 10-year yield hit a 10-month high yesterday and is currently yielding 4.4%. If it weren’t for the rally in tech stocks, the S&P 500’s 10% gain over the past month would be half that. The semiconductors have been carrying the market and continue to do the heavy lifting this morning up more than 1%. Intel is rallying 4% on reports that Apple is weighing using Samsung and Intel to build device processors as a second option to Taiwan Semiconductors. AMD could provide a boost to the sector when it reports today after the bell. “Real world” stocks could support a broader rally with companies like Cummins and DuPont painting a rosy forecast.

Shop til ya drop: Shopify is falling in the pre-market on fears that sales growth will slow the next quarter. The e-commerce platform’s sales this quarter grew 34% – much better than expected, but the forecast implies only high 20s growth. It seems unfair to beat the stock up for that considering high 20s growth is better than current estimates for 26% growth. Clearly the bar remains high even though the stock is down 20% in 2026. Investors are also picking up on the free cash flow outlook which is below expectations and could be due to elevated spending on AI initiatives. The conference call just started at 8:30. Aside from the reaction, the results are strong. The dollar value of transactions on the platform hit a 4+ year high and grew over 30% for the fourth consecutive quarter.

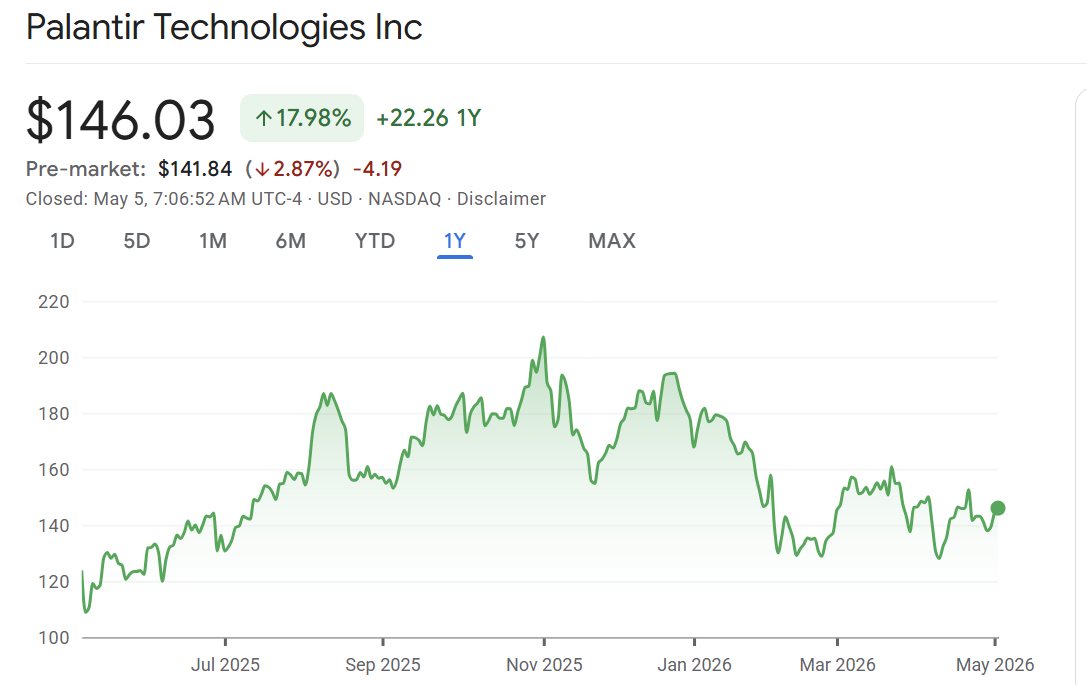

No cigar: Palantir is dipping 3% in the pre-market despite sales surging 84% from last year and earnings per share quadrupling – both better than expected. The AI-enabled software company benefited from government demand, particularly in the US. I guess two wars in the span of three months and a national drive to reduce illegal immigration is good for business. If you want to quibble, sales to businesses came in slightly weaker than expected but still grew 133% (!!) from last year. The stock is down 30% from November peak as investors put it in the software penalty box. Or maybe its the valuation penalty box. The stock trades at 104x forward earnings, but as I mentioned earnings are up 4x from last year. The company also increased its forecast – not that investors care this morning.

Penalty box: Several stocks that are in investor’s bad books are in focus today.

- Thomson Reuters (-55% from record high) reported results this morning beating expectations, increasing its dividend, and firing back at the idea that it can be disrupted by AI. Shares have been hit after Anthropic released several enterprise facing AI updates. Thomson Reuters said their legal, accounting and professional clients are choosing their AI products because they can produce verified and audited results in what they call “fiduciary-grade” AI. “In a normal environment we would call this a solid but somewhat uneventful quarter,” wrote TD’s Vince Valentini, “However, with massive valuation contraction LTM, and swirling uncertainty about AI disruption, we call this a confidence-inspiring quarter that should spark a 5%+ rally for the share price.”

- ServiceNow (down 50% from peak in 2025) is slightly higher after hosting an analyst day trying to signal its relevance in AI as its stock has also been caught up in the saas-pocalypse. ServiceNow says it can grow revenue 20% per year out to 2030. While investors worry their software business will be eroded, the company notes that half of their new clients are already on the AI pricing model. The key is that ServiceNow is switching from a pay-per-user model to a pay-for-use model. On the podcast, Moore said he is staying away from anything software including names like ServiceNow.

- Propel Holdings (down 44% from 2025 height) reported better than expected results in a quarter investors were nervously anticipating because of the goeasy blow up earlier this year. While Propel is a very different beast (business primarily in the US and does shorter term subprime loans) the stock has been caught up in the anxieties around credit quality. This quarter may put these fears to rest. Provisions for credit losses came in below expectations as its loan book increased more than expected and net charge offs remained stable. It also boosted its dividend 7%.

Glowing: Cameco is popping in the pre-market showing that it is able to capitalize on the nuclear renaissance. Profit and production was better than expected aided by higher realized prices for uranium. The stock has been listless recently, taking a pause after a 152% increase over the past year. Westinghouse, which Cameco jointly owns with Brookfield, was engaged by the US government to build reactors with commitment to purchase $80 billion worth of Westinghouse technology. Investors still have questions about the timing of this, and it will likely be a major focus of the earnings call says TD’s Craig Hutchison. Recall, when we interviewed Tim Gitzel a month ago he said the deal was progressing nicely. Kieran Moore talked about Cameco on the podcast, saying he thinks its too expensive to buy right here but likes nuclear in general.

Send questions for our next guest! Questions@inthemoneypod.com

![]()