Value traps can destroy your portfolio—but the right turnaround stock can be a game changer. How do you tell the difference? On this episode of In the Money with Amber Kanwar, Paul Harris, Portfolio Manager at Harris Douglas Asset Management, explains his framework for buying underperforming stocks without getting burned. He also shares why he wants nothing to do with SpaceX at current valuations, arguing the company is priced far ahead of its fundamentals despite the excitement around the space race. The conversation also dives into Elon Musk’s biggest strengths—and what Paul believes are his biggest blind spots as an operator and capital allocator.

Pro Picks is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

LAST YEAR’S PICKS — STILL HOLDING, STILL WORKING

PAST PICKS SCORECARD — March 4, 2025

- Alphabet (GOOGL): +104% ✅ — still owns it, never sold despite the Gemini scare; search hasn’t gone away, YouTube is thriving, cloud is growing, and Waymo is a call option most people aren’t pricing in.

- Stryker (SYK): -14% ❌ — still owns it, still believes the thesis; the cyberattack was a one-time disruption, aging populations need more procedures, and surgeons who train on Stryker equipment don’t switch.

- Canadian Natural Resources (CNQ): +55% ✅ — trimmed when it ran hard (cut from a 2.5% position to 1.5%), wouldn’t add more until oil settles; calls it one of the best-run energy companies in Canada — always on budget, always a smart acquirer when prices fall.

Three unloved stocks with upside:

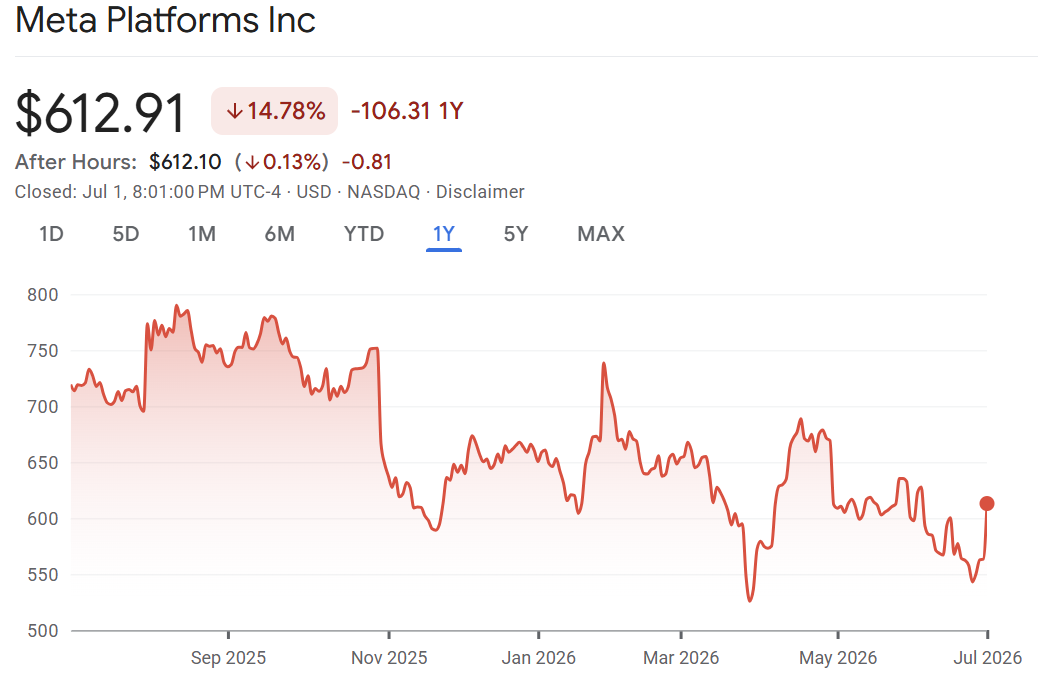

Meta Platforms (META) | AI is visibly working — and the stock doesn’t reflect it

- Trading at roughly 17x earnings, a meaningful discount to the broader market, near a 52-week low when Paul picked it

- The AI bull case here isn’t speculative — it’s showing up directly in advertising revenue numbers, quarter after quarter

- Core brands (Facebook, Instagram, WhatsApp) continue to grow; the advertising machine is being made more efficient by AI in real time

- The risk Paul names explicitly: Zuckerberg’s tendency to pursue expensive moonshots (the metaverse being the cautionary tale) — and unlike Alphabet or Microsoft, Meta has no cloud business to monetize its AI spend externally; every dollar it spends on chips and infrastructure is purely for its own use

- Thesis: cheapness outweighs the risk, especially when you can see AI working in the numbers right now

Microsoft (MSFT) | The “everyone’s going to rip out Office” narrative is absurd

- Hit a new 52-week low in the days before this episode, trading around 22-25x earnings versus 35-40x not long ago

- The bear case — that enterprises will abandon Microsoft’s software stack for AI-native alternatives — misunderstands how deeply embedded these tools are in global institutions; a CTO who gets that decision wrong loses his job

- Azure cloud growing 37% last quarter; the software moat (Word, Excel, PowerPoint, Teams) is more durable than the market is pricing in

- Paul’s honest critique: Copilot is clunky right now — but that’s a timing issue, not a structural one; the enterprise stickiness exists regardless

- Thesis: a world-class, deeply embedded software and cloud business at a multiple you haven’t been able to buy it at in years

EssilorLuxottica (EL.PA — Euronext Paris) | A slow-and-steady global monopoly the market briefly confused for a tech company

- Dominant in both lenses (Essilor) and frames (Luxottica — Ray-Ban, Oakley, Sunglass Hut, plus licensed brands including Chanel and Dior); if you wear glasses or sunglasses, there’s a good chance this company made them

- Invented progressive lenses (bifocals without the line) — a genuinely defensible innovation that generates recurring revenue as populations age and screen time increases

- The market briefly inflated the stock on Meta Ray-Ban smart glasses excitement — then punished it when organic growth slowed and wearables failed to scale

- Paul’s view: this was never a tech company and shouldn’t be valued like one; it’s a 3-5% annual grower with dominant market share, high switching costs, and a global annuity of repeat customers who need new lenses every few years

- Trading in the dumps on misplaced wearable disappointment — a classic case of the market pricing in a narrative that was never the real business

Don’t miss our next episode!

![]()