Hedge fund manager Eric Jackson tells In the Money with Amber Kanwar why he’s doubling down on Opendoor (OPEN) and Better (BETR), while adding two Bitcoin miners that are morphing into AI infrastructure plays: Cipher Mining (CIFR) and Iris Energy (IREN). He breaks down why both could ride the surging demand for data centre capacity and why retail investors are once again getting there before Wall Street.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information.

Pro Pick 1: Open Door Technologies (OPEN)

- Why Eric Likes It:

- Sees it as a turnaround story similar to Carvana, which recovered from near-bankruptcy to become a 100-bagger due to management conviction and business model resilience.

- New leadership changes (former Shopify COO as CEO, co-founders Keith Rabois and Eric Wu back on the board) provide strong tech expertise and vision, addressing past mismanagement under Carrie Wheeler.

- Business model disrupts residential real estate by acting as a national platform matching buyers and sellers, focusing on quick, certain home purchases and sales; potential to expand into mortgages and title insurance for higher margins like Carvana’s financing arm.

- Currently undervalued with a 0.1x forward P/S multiple (down from 7x), and sales forecasts are outdated; expects rerating as profitability improves with falling interest rates unfreezing the housing market.

- Not a meme stock but a “cult stock” like Tesla or Palantir, with durable growth potential as the “Uber of real estate.”

- Upside: Short-term target of $82 (based on 5x forward P/S by 2028, assuming $12B revenue or 0.5% US market share); long-term (3-5 years) potential for $500/share and $350B market cap if it dominates the sector.

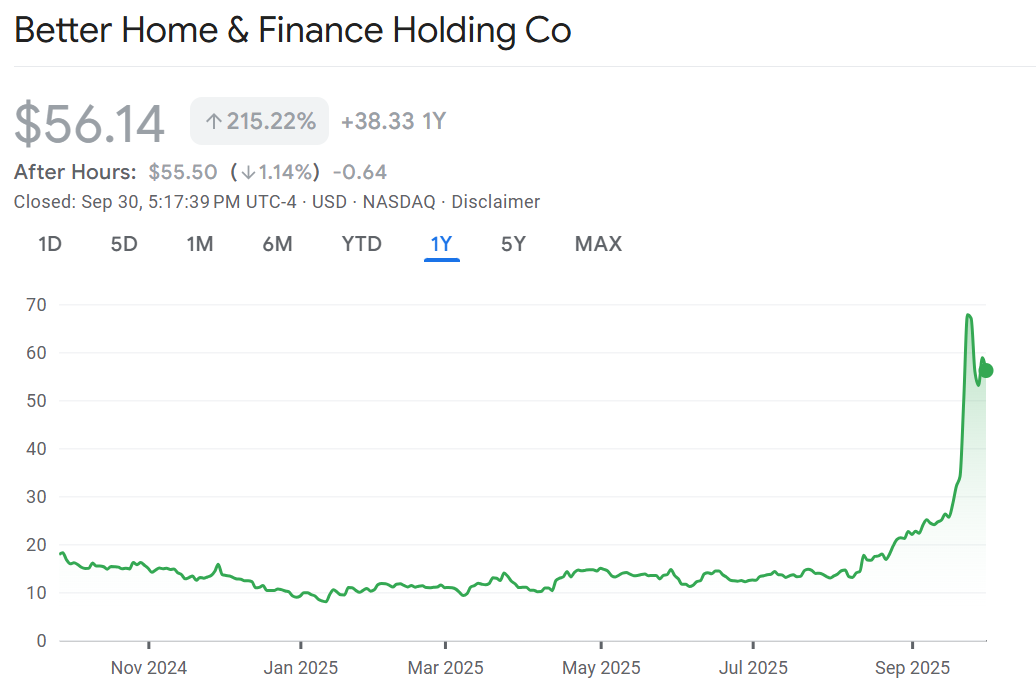

Pro Pick 2: Better Home & Finance (BETR)

- Why Eric Likes It:

- Distressed mortgage origination business similar to Carvana/Open Door post-pandemic bust, but now recovering with AI (Betsy system) replacing manual labor, enabling scalability without rehiring staff (e.g., could handle 5x past peak volume of $54B).

- CEO Vishal Garg is a technical genius despite past controversies (e.g., mass layoffs); company delayed SPAC due to SEC/political issues but now positioned for growth.

- Rate cut play: Every 25 bps drop in rates boosts volumes and refinancing; business could return to $243B potential originations (limited by manual processes before).

- Undercovered by analysts, trading at ~1x forward revenues vs. comparables; competes with big players like Rocket Mortgage but with superior AI efficiency.

- Transforms from boom-bust cycle to profitable, AI-driven model; not just mortgages but potential in related financing.

- Upside: Near-term $626/share (at 19x forward revenues like comparable Figure) or $400/share (at conservative 5x); long-term $12,000/share by 2028 if it scales back to peak potential.

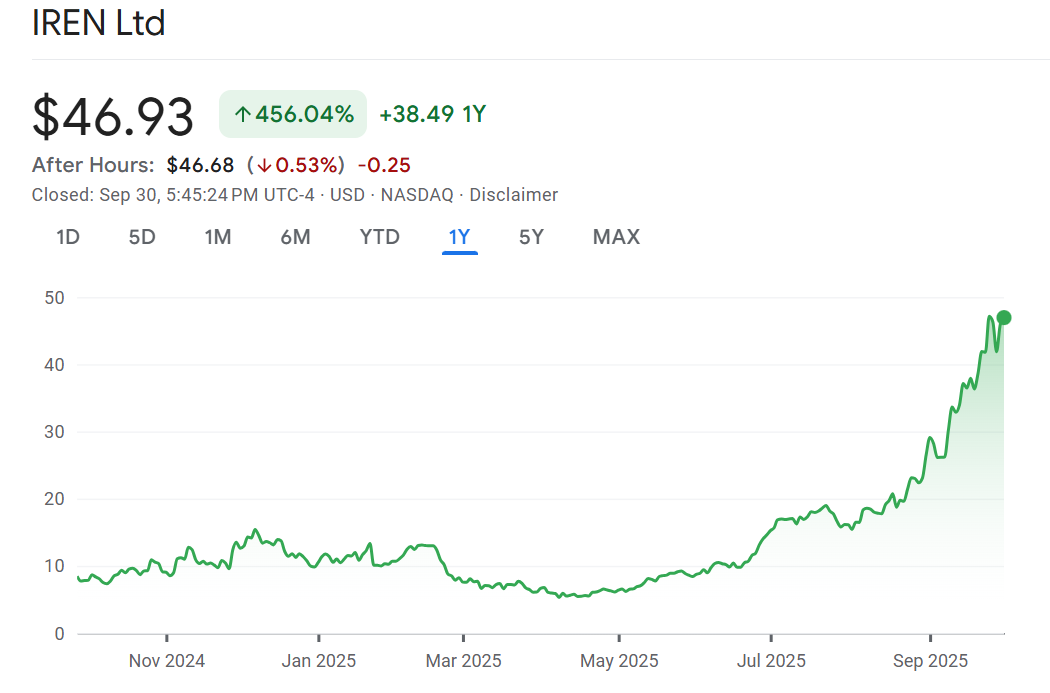

Pro Pick 3: IREN (Iren LTD)

- Why Eric Likes It:

- Transitioning from Bitcoin mining to AI data center provider, using mining profits to fund massive expansion (3 GW of energized data centers in places like Louisiana and West Texas coming online in next 12 months).

- Addresses global shortage of AI infrastructure; hyperscalers (e.g., Microsoft, Meta) are ramping capex by $10B+ quarterly to meet demand from tools like ChatGPT.

- Better positioned than pure AI plays like CoreWeave (which owns no data centers and acts as middleware); IREN owns land, negotiates power, and builds directly.

- Recent rerating by Wall Street (12-13 analysts, mostly buys) as market realizes it’s not just a Bitcoin proxy but an AI growth story; undervalued relative to pipeline.

- Potential for major partnerships (e.g., with Oracle or Microsoft) similar to Nebius’s $18B Microsoft deal for 1 GW (implying 3x value for IREN’s 3 GW).

- Upside: 100x potential in 5 years from entry point (~$9/share), implying ~$900/share, driven by AI data center deals and growth.

Pro Pick 4: CIFR (Cipher)

- Why Eric Likes It:

- Like IREN, evolving from Bitcoin mining to AI data centers, with 3 GW of capacity energizing soon; mining profits fund buildout without distress.

- Recent catalysts: 5% investment from Google and another deal; expected big announcements with hyperscalers (e.g., Oracle, Microsoft) by year-end.

- Disrupts middleware players like CoreWeave by owning and operating data centers directly; meets exploding AI demand from projects like Stargate (Oracle/OpenAI).

- Wall Street coverage (12-13 analysts, mostly buys) shifting from Bitcoin focus to AI valuation; stocks undervalued as group despite Bitcoin recovery.

- Comparable to Nebius-Microsoft deal ($18B for 1 GW over years), suggesting massive revenue potential (3x for CIFR’s 3 GW).

- Upside: 100x potential in 5 years from entry point (high $30s, but current ~$11 after pullback), implying ~$300/share (adjusted for context), fueled by AI partnerships and expansion.