Wall Street meets real talk in this week’s In the Money with Amber Kanwar, featuring none other than Downtown Josh Brown — the CEO of Ritholtz Wealth Management, CNBC regular, and host of the hit podcast The Compound and Friends. From surviving the chaos of the 2008 financial crisis to building a wealth management firm with billions under management, Josh shares how storytelling, not spreadsheets, shaped his investing journey.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information.

Uber (NYSE: UBER)

The Case: Autonomy isn’t the threat — it’s the upside.

- Josh Brown calls Uber his largest position, holding since the 40s and not selling a share. He argues Uber is “the cheapest of the large-cap tech platforms,” with roughly 25% expected growth by 2026 and trading at just 16–17x forward earnings — a major discount to peers.

- Critics worry about driverless taxis eroding margins, but Brown flips that narrative: as human drivers are replaced by autonomy, Uber’s biggest cost — the driver take rate — disappears. That means more competition but far higher profitability.

- Even Uber Eats could transform, with drones and robots delivering food instead of cars burning gas for a burrito. “Autonomy isn’t the bear case,” he says. “It’s the bull case.”

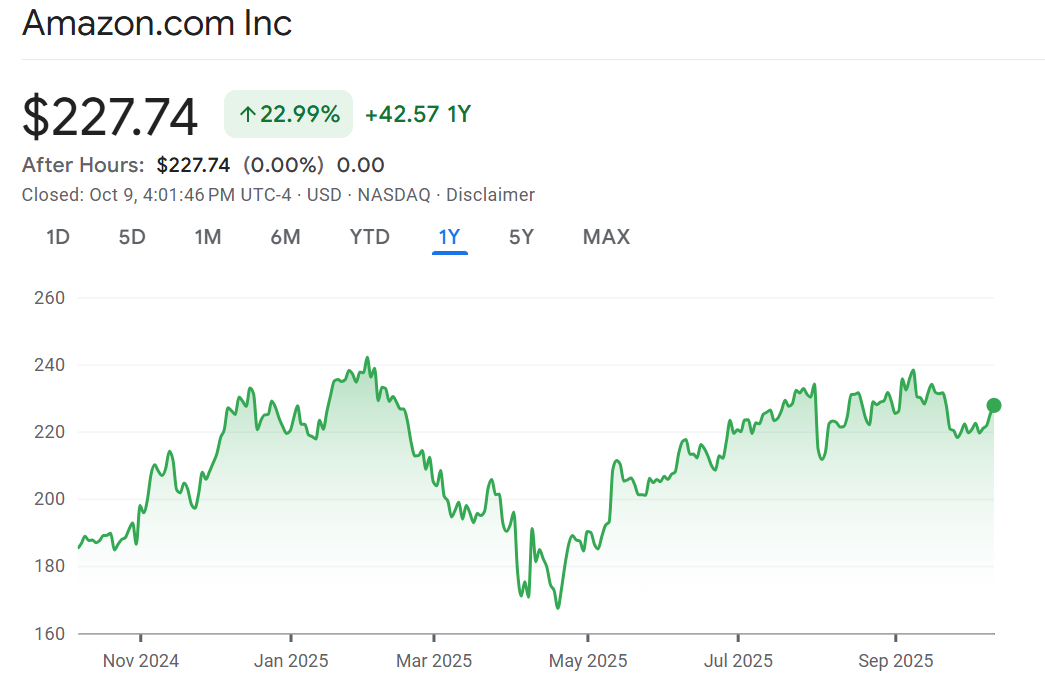

Amazon (NASDAQ: AMZN)

The Case: Anthropic and AI will reprice the cloud story.

- Amazon has been a laggard this year — “a nothing burger,” Brown admits — but he’s adding, not leaving. The core thesis: investors are underrating Amazon’s position in AI through Anthropic’s Claude.

- He highlights that Claude now serves more enterprise customers worldwide than OpenAI, and Amazon’s AWS stands to benefit most from that adoption. Add to that Amazon’s in-house AI chips for inference and training, and you get a company poised to surprise skeptics who think it’s missing the AI wave.

- “The market isn’t giving them enough credit,” he says. “We’ve seen that story before.”

Rocket Companies (NYSE: RKT)

The Case: Becoming the “Uber of housing” through full-cycle integration.

- For Brown, Rocket is more than a rate-cut play. After years of a housing bear market, the company has doubled and tripled down on becoming a vertically integrated home-buying ecosystem.

- It starts with search — Redfin, where many buyers begin — now tightly linked to Rocket Mortgage. Then comes origination, via Rocket’s core lending business, and servicing through Mr. Cooper, now rebranding as Rocket. From home search to HELOCs, Rocket wants to control every financial touchpoint.

- When rates fall, that machine ignites: “Rocket’s refi engine is a supernova,” Brown says. “No one will make more money from refi activity than they will.”

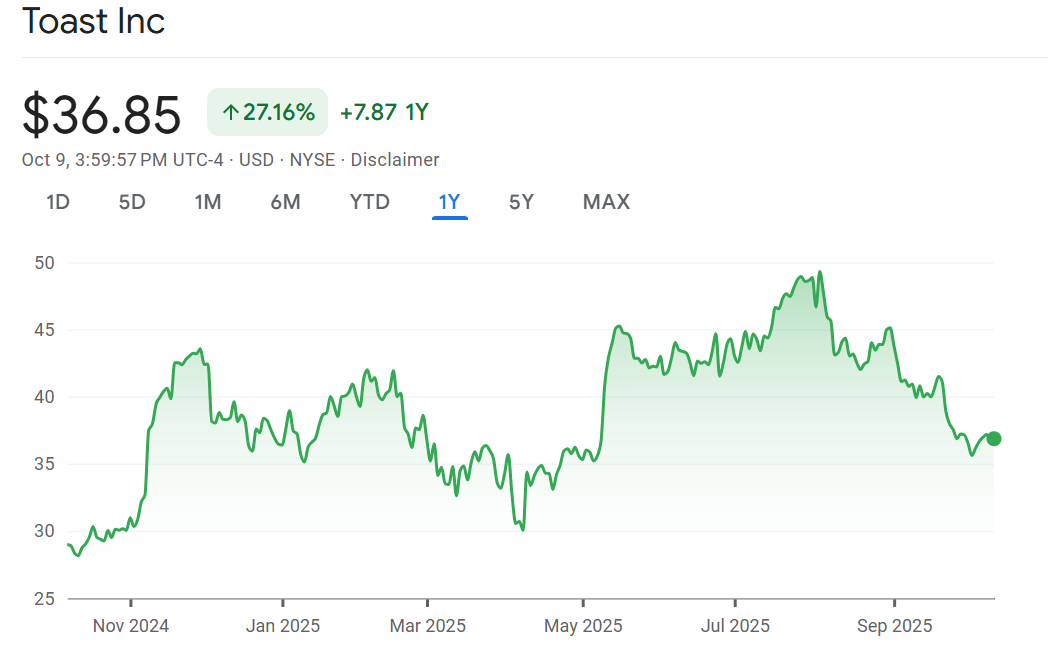

Toast (NYSE: TOST)

The Case: The dominant restaurant platform hiding in plain sight.

- Toast shares have stumbled after tweaking pricing for smaller restaurants, but Brown calls the reaction “silly.” Growth remains strong, and he’s been buying since the teens, even adding at higher prices.

- What drives his conviction: Toast’s expanding software ecosystem. Once its POS terminals are in restaurants, the company layers on tools for inventory, payroll, ordering, and analytics — creating sticky, recurring revenue across the industry.

- “There’s Square and Clover,” he notes, “but Toast could take the entire ball of wax.” With low churn and increasing penetration, Brown sees Toast as a platform play, not a niche software name.

Don’t miss our next episode with the one and only Mike Rose!

![]()