AI was supposed to supercharge software. Instead, it’s threatening to disrupt it. Ivana Delevska, Founder & CIO of Spear Advisors, joins In the Money with Amber Kanwar to break down whether the brutal software sell-off is justified — or overdone. She explains why she isn’t picking up software stocks right now and why the best bet is in the capital equipment sector like the stocks mentioned below.

This segment is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

- Early Innings of a New Cycle: The stock has risen from cyclically depressed levels, but Ivana sees this as the start of a multi-year theme in optical components, driven by AI demand.

- Significant Earnings Reacceleration: A new product launch in the second half of the year is expected to drive earnings nearly doubling, justifying the current valuation despite the recent run-up.

- Compounding Potential: Meets criteria for over 20% annual compounding, with room to double over five years as hyperscalers ramp up infrastructure.

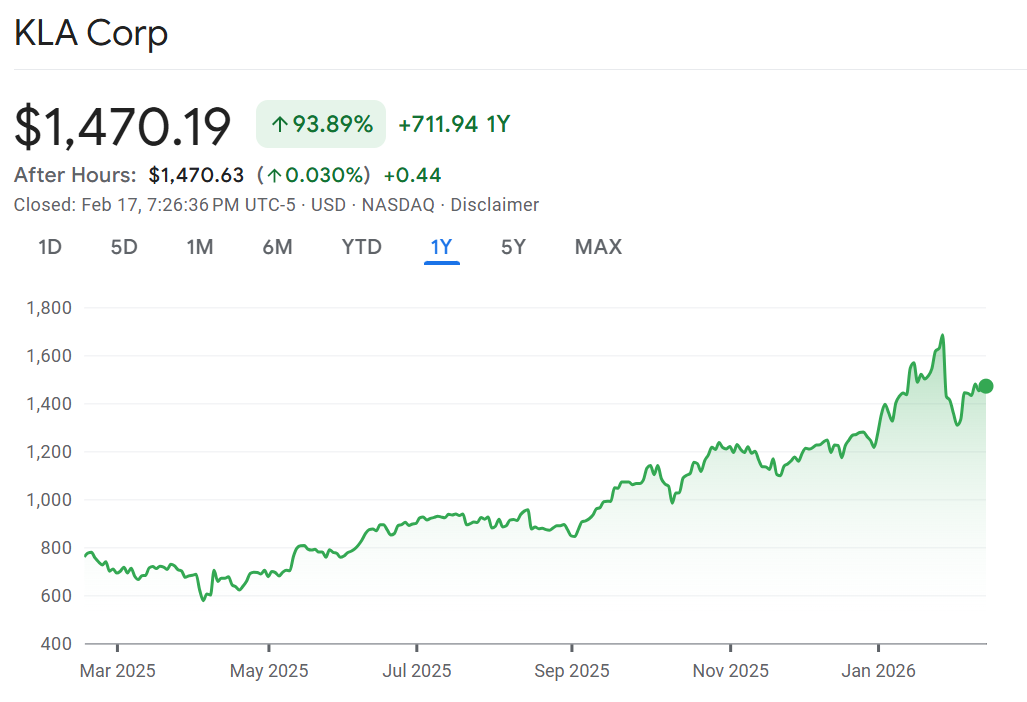

KLA Corp (KLAC) – Semiconductor Capital Equipment

- Early Cycle Growth: The semicap equipment cycle turned mid-last year, with KLA and peers like ASML, LRCX, and AMAT just beginning to see earnings acceleration—far from peak performance seen in past cycles.

- Supply Constraints Driving Upside: Growing AI chip production is creating capital equipment bottlenecks, positioning KLA for strong multi-year gains as demand outpaces supply.

- Long-Term Doubling Potential: Despite recent moves, the stock can still double over five years, with 2027 shaping up as a key year for ASML and the broader group.

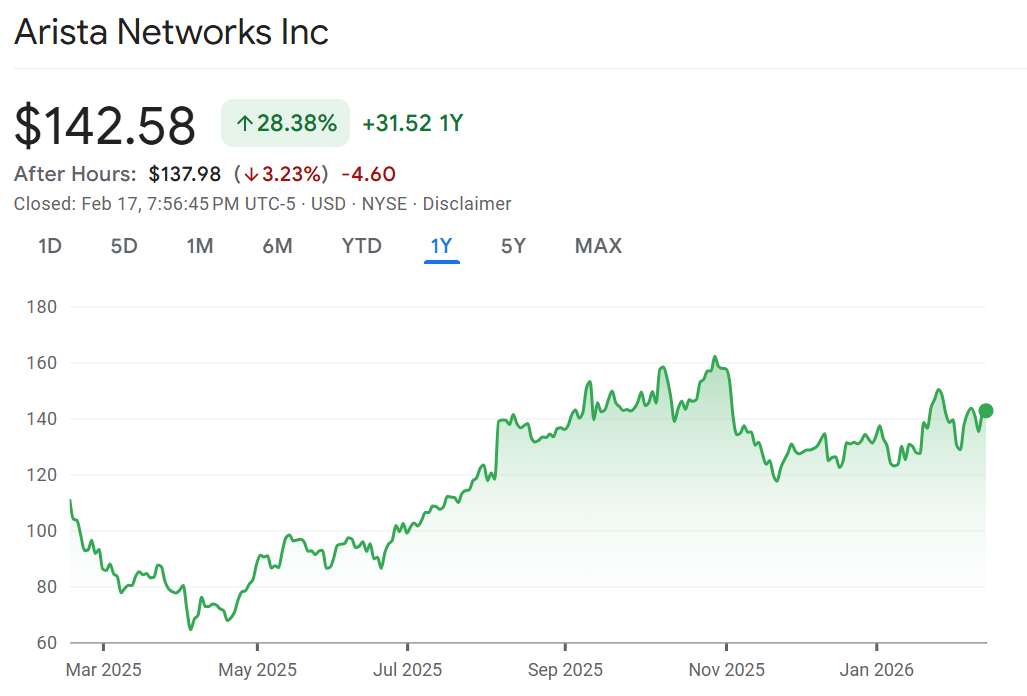

Arista Networks (ANET) – AI Networking Leader

- Timing-Driven Pullback as Opportunity: Recent softness stems from project timing, not fundamentals—creating a valuation entry point after a quarter without blowout numbers.

- Strong Growth Trajectory: Expected to nearly double revenue from $6 billion in 2023 to $11 billion this year, fueled by hyperscaler and enterprise AI spending; margins concerns are overstated due to hardware-software mix shifts.

- Tied to Capex Boom: Growth is a multiple of hyperscaler capex, with high confidence in sustained spending; potential for even higher rates if enterprise adoption accelerates, supporting 20%+ annual compounding.

Don’t miss the next episode!

![]()

DISCLAIMERS: This text AI generated and should be checked against actual delivery. The content provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.