In a market obsessed with AI and momentum trades, dividend investors are quietly cashing in. In this episode of In the Money with Amber Kanwar, Laura Lau, Chief Investment Officer at Brompton Funds, shares how she’s finding dividend income in a market chasing growth. With stocks at record highs, Lau explains how to balance yield, total return, and capital appreciation.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information.

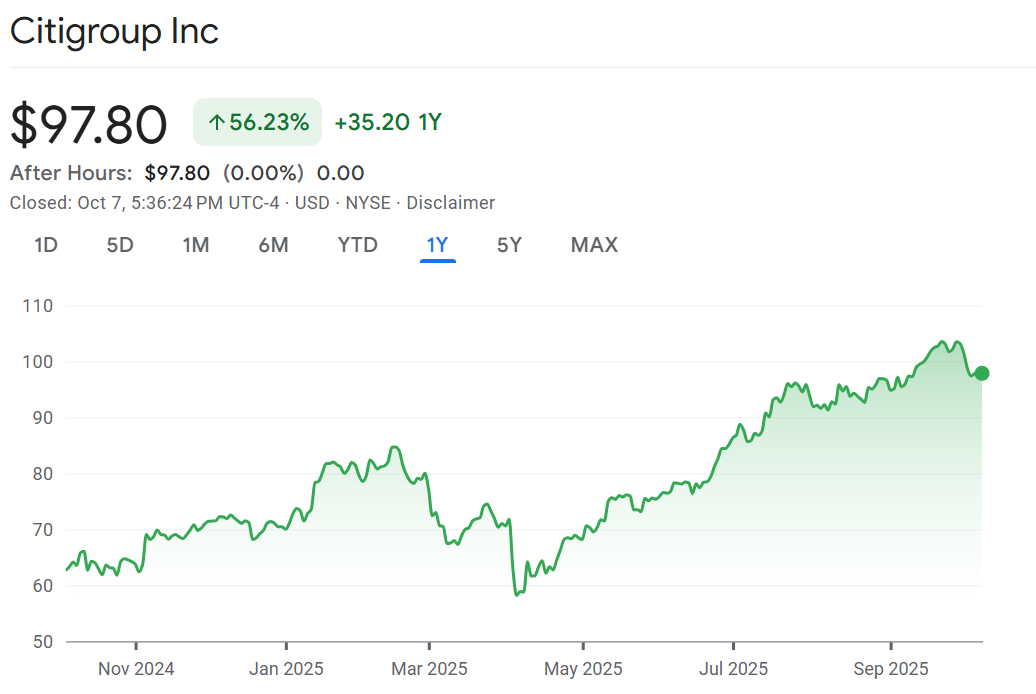

Citigroup (C)

Why own it: Citigroup has been a laggard since the financial crisis, but 2025 may mark a structural turnaround.

- Deregulation tailwind: U.S. banks are facing lighter capital requirements, freeing up cash that had been locked for safety buffers.

- Cost cuts + AI efficiency: Citi is cutting ~20,000 jobs and leaning on AI to automate processes, improving profitability.

- Capital return: $16B in excess capital could fund share buybacks of up to ~10% of market cap over the next 12 months.

- Capital markets rebound: ~30% of Citi’s revenue comes from banking & markets, which are strengthening again.

Valuation: Still trades below pre-crisis levels despite a 40% run in 2025 and is outperforming the S&P Bank Index recently — management believes the inflection point has already passed.

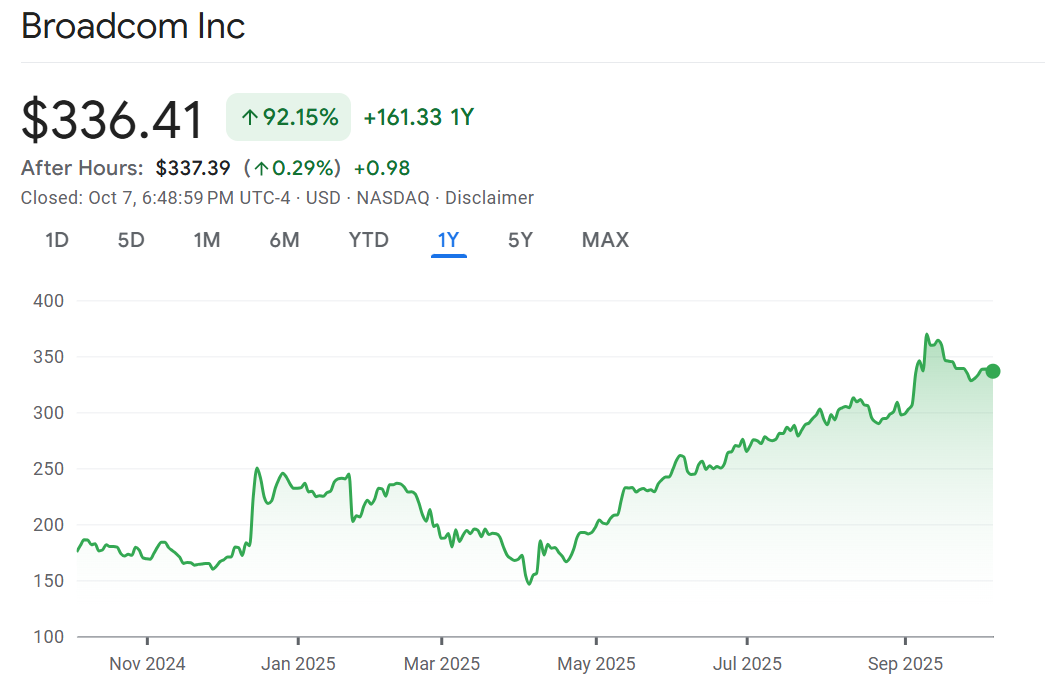

Broadcom (AVGO)

Why own it: Broadcom is a balanced way to play AI and infrastructure growth — while getting paid to wait.

- Two engines: ~50% recurring infrastructure software + custom & networking chips used in AI data centers.

- AI demand: AI-related revenues grew 100%+ YoY, with strong pricing power thanks to dominant market share.

- Income growth: Dividend has grown at a 13% CAGR over the past 5 years.

- Downside cushion: Software revenue smooths the cyclical chip business, making it attractive for dividend investors.

Valuation: Cheaper than Nvidia and offers a higher dividend yield — a more balanced AI winner for value + income portfolios.

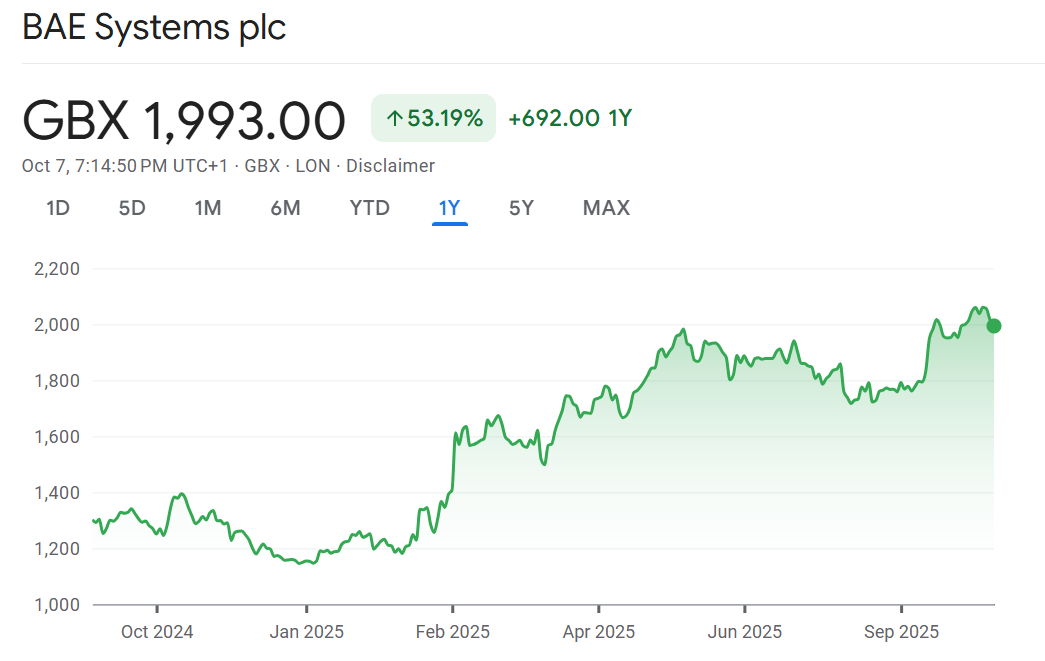

BAE Systems (BA-LON)

Why own it: Europe is in a multi-year defense spending catch-up, and BAE is positioned to benefit most.

- Defense supercycle: NATO allies are being pushed to increase military budgets — Europe’s spend is rising from 2.1% to 2.5% of GDP and is targeting ~3.5%.

- Diversified platforms: ~55% air (planes, missiles), ~35% naval (frigates, ships), ~15% land (tanks).

- Political tailwind: Heightened geopolitical risk + U.S. pressure to share the defense burden support sustained demand.

- Guidance up: Management already raised sales guidance for 2025 and sees a long runway.

Valuation: Shares are near all-time highs but management believes the upcycle isn’t priced in, with years of underinvestment still to catch up.

Bottom line

- •Citi (C): Deregulation + buybacks = deep-value bank turnaround.

- •Broadcom (AVGO): AI + software balance + dividend growth at a reasonable price.

- •BAE Systems (BAESY): Europe’s defense spending boom is just starting.

Coming up on our next episode!

![]()