“The best of the bull market is still ahead of us.” That’s how Nick Griffin, Founding Partner and CIO of Munro Partners, sees it. The Australia-based global growth investor joins In the Money with Amber Kanwar to explain why the AI boom isn’t a bubble — it’s the start of a once-in-a-generation expansion. Griffin says we’re only in year three of a bull market that could last a decade, with trillions of dollars still to be spent building the infrastructure for artificial intelligence. From data centres and chipmakers to clean energy and sports entertainment, he breaks down where the biggest opportunities lie — and why staying optimistic could be the smartest move in markets right now.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information.

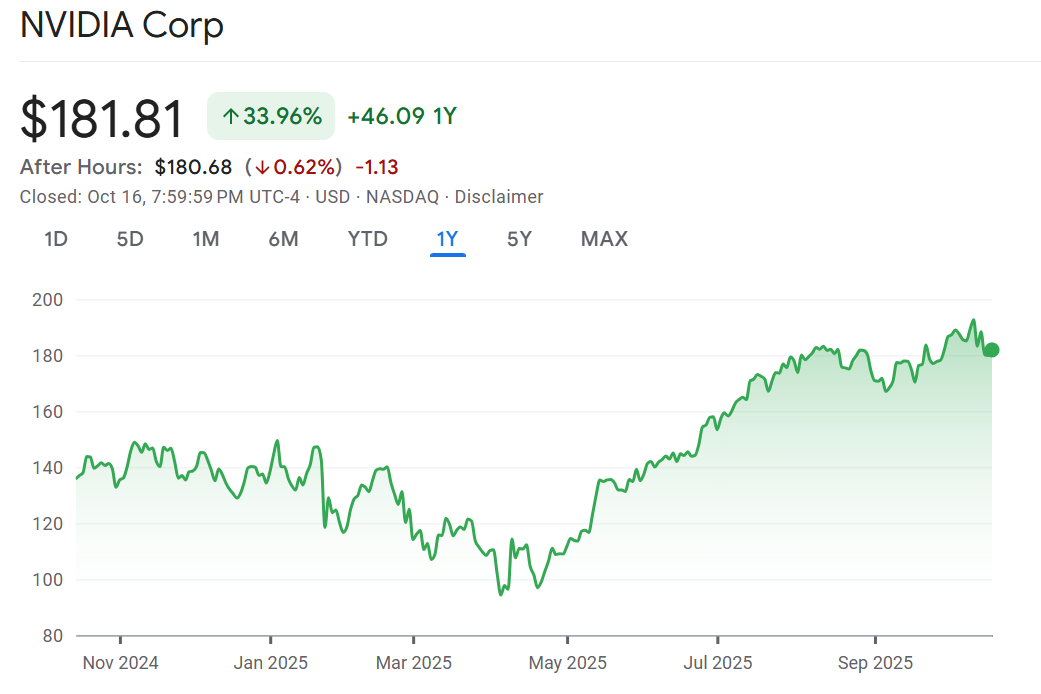

1. NVIDIA (NVDA) “The next NVIDIA is still NVIDIA.”

Why It’s a Top Pick: NVIDIA remains the dominant force in AI infrastructure, and the market still undervalues the scale of upcoming demand.

Most Compelling Reasons to Own

- AI data center build-out is not fully priced in. If hyperscalers spend what they’ve committed, those data centers will be “predominantly filled with NVIDIA chips.”

- Valuation vs. Growth: Trades at 27x forward earnings while growing 30–40% annually for the next 5 years.

- Two possible outcomes: P/E multiple compresses or share price rises roughly 30% per year.

- Apple analogy: NVIDIA is to AI what Apple was to the iPhone cycle—a long-term compounding machine. Griffin sold Apple early and missed a 27x return. He won’t repeat that mistake.

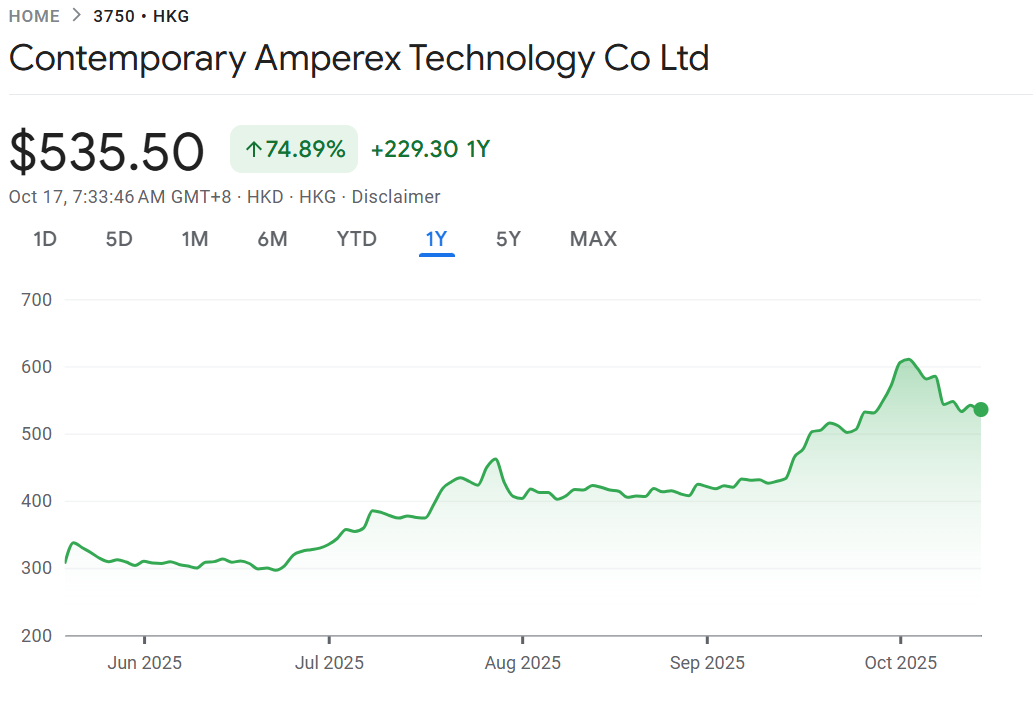

2. Contemporary Amperex Technology (CATL)

Ticker: 300750.SZ or 035.HK

Why It’s a Top Pick in Climate Tech: CATL is the largest battery manufacturer in the world and sits at the center of electrification across vehicles, energy storage, and robotics.

Most Compelling Reasons to Own

- 38% global market share in batteries.

- •Supplies: EVs, electric trucks, grid-scale storage for renewables and data centers, drones, robots, even electric ships,

- Battery demand growing 20–25% per year.

- Electrification and renewable buildout create long-term structural demand.

- Most profitable battery company. “They’re the TSMC of batteries”—dominant, efficient, and essential.

- Valuation still attractive: Trades at low 20s P/E. As earnings grow, share price should follow.

- Now easier to access. Dual-listed in Hong Kong, no longer mainland-only.

3. TKO Group (TKO)

Owns UFC, WWE, and Professional Bull Riding

Sports Are a Structural Growth Theme: Sports are now the last form of live appointment viewing. Everything else is on-demand. Advertisers and streamers pay a premium for guaranteed audiences.

Most Compelling Reasons to Own

- Owns valuable global sports IP: UFC, WWE, Professional Bull Riding

- Media rights and team values keep rising. As linear TV dies, sports become the most valuable content category.

- Strategic media deals expanding reach: WWE on Netflix → doubles the audience, UFC deal with Paramount → ends pay-per-view model → more viewers

- Valuation: Slightly expensive on multiples, but growth is durable.

- Bonus: Formula 1 (FWONA / FWONK on NASDAQ) is also in the fund—another sports IP flywheel.

Don’t miss our next episodes! Get your questions in now! Email questions@inthemoneypod.com

![]()