Healthcare takes centre stage as Jeff Elliott, Managing Director and Head of Global Equity at BMO Global Asset Management draws on his deep sector expertise to unpack one of the most politically exposed — and misunderstood — areas of the market. He explains why policy noise can create sharp dislocations without permanently damaging businesses, and how active managers look for mispriced opportunities across pharma, biotech, and med-tech while others retreat from the sector.

This segment is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

Three misunderstood healthcare stocks:

Boston Scientific, a leader in medtech, has been a core holding for BMO since inception. After a recent pullback from highs around $106-108 to sub-$90, it’s positioned for renewed growth through innovative devices for atrial fibrillation (AFib) treatment and strategic acquisitions.

- Attractive Valuation Post-Pullback: Trading at 25-26x next year’s earnings with teens-level growth, the stock offers a favorable PEG ratio, making it undervalued relative to its high-growth medtech peers after rotation out of the sector.

- Strong Core Product Momentum: Farapulse (pulse field ablation) continues to drive adoption as a safer AFib treatment, representing a $3-5 billion opportunity on a $12 billion topline, with competition concerns overstated.

- Upside from Acquisitions and Pipeline: The Penumbra acquisition is accretive and enhances growth in core areas, while the Watchman device shows promise with upcoming data potentially boosting adoption over oral anticoagulants.

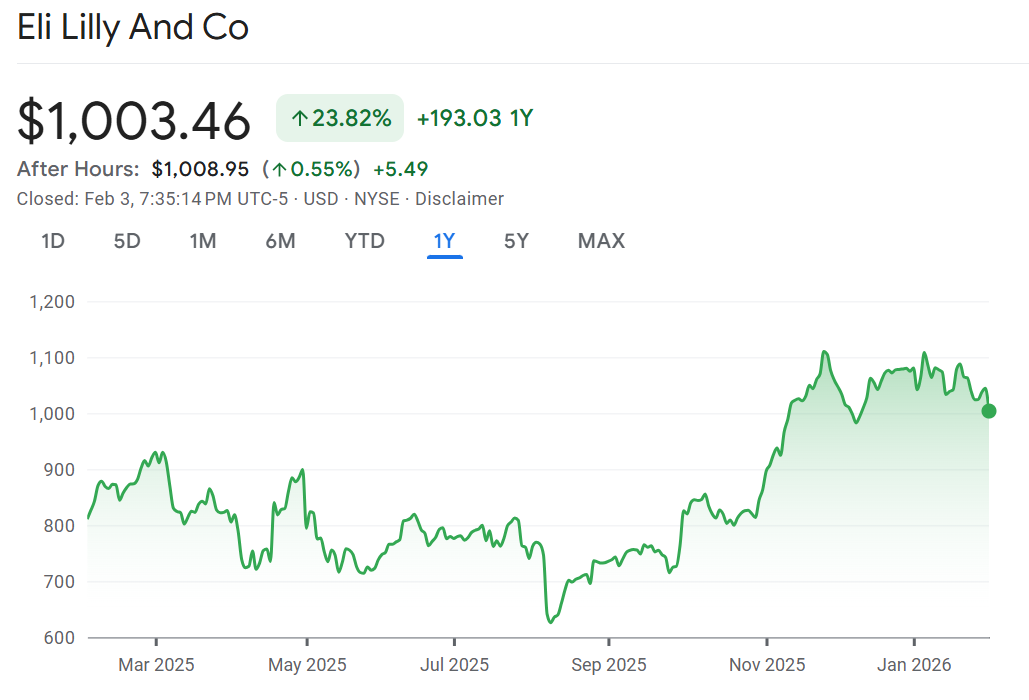

2. Eli Lilly (LLY)

Eli Lilly stands out in the GLP-1 space with superior pipeline depth compared to competitors like Novo Nordisk. Despite trading at a premium, its growth trajectory justifies the multiple, with topline expected to double by 2030.

- Superior Pipeline Advantage: Innovations like orforglipron (oral) and retatrutide (triple G, showing ~30% weight loss) position Lilly ahead in both oral and injectable markets, outpacing Novo’s offerings.

- Robust Earnings Growth Path: Valued at 40x this year’s earnings but dropping to 29x next year, the stock supports a premium due to strong, sustained growth from market expansion and rational pricing in the oligopoly.

- Resilience to Competition: With a clean growth outlook and limited threats from rivals, Lilly benefits from broader indications beyond diabetes/weight loss, including potential in Alzheimer’s (though conservatively viewed as upside).

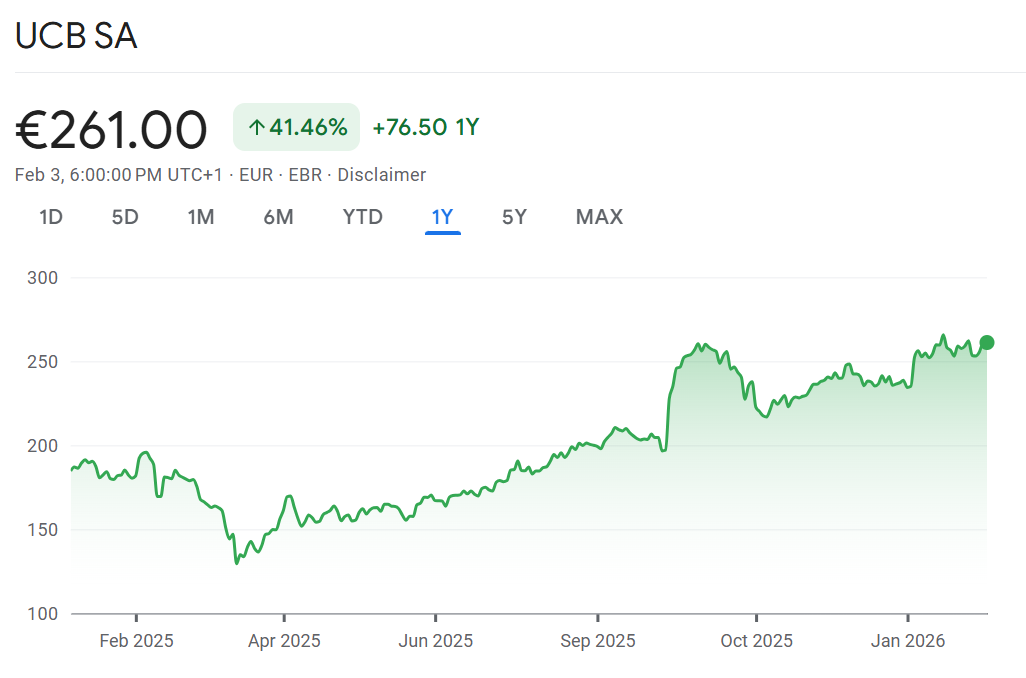

3. UCB (UCB.BR)

UCB, a Belgian biotech firm, is an under-the-radar play with transformative potential from its autoimmune drug Bimzelx. As a smaller company, it offers outsized growth at a low multiple, with limited liquidity adding to its “hidden gem” appeal.

- High-Growth Driver in Bimzelx: Expected to generate $4-5 billion annually in psoriasis and other autoimmune indications, surpassing competitors like Skyrizi and Cosentyx, effectively doubling UCB’s size.

- Exceptional Valuation Metrics: Trades at a PEG of 0.7 with fantastic long-term growth, similar multiples to larger peers like Lilly but with cleaner patent and competitive risks post-Moonlake’s trial failure.

- Well-Managed, Durable Story: Strong management and science-backed profile make it a high-quality opportunity, benefiting from investors hunting international smaller-cap stories amid market broadening.

Don’t miss our next guests! Father and son money manager duo!

![]()

DISCLAIMERS: This text AI generated and should be checked against actual delivery. The content provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.