WATCH: It’s the biggest takeover battle in Canada right now. Adam Waterous returns to In the Money with Amber Kanwar to make his case for why MEG Energy shareholders should vote for his offer. As Founder & Executive Chairman of Strathcona Resources he’s going head-to-head against Cenovus in a high-stakes bidding war.

We had curriculum night at Child #2’s new school. The school has a uniform and like fools we thought that could simplify mornings. Instead, the school has decided that the five-days-of-the-week are a relic and go by a day system: Days 1-8. Every Day 1 she can wear her street clothes, but Day 1 can fall on any day of the week. And despite eschewing the days-of-the-week system as a guidepost, they made an exception for Thursday’s where she must wear her gym clothes all day. So that’s where 25 minutes of my day now goes to understanding.

Here are five things to know this morning:

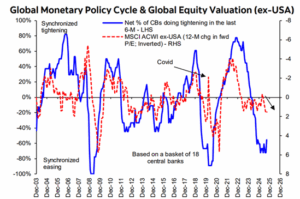

Cool down: Futures are slightly lower this morning after the TSX, S&P 500, Dow Jones Industrial Average, and NASDAQ hit fresh records yesterday. Gold is hitting a record this morning again. This is all in anticipation of the Fed’s rate decision next week. They are widely expected to cut rates by 25 basis points with some hoping for the hint of something larger (50 basis points). The higher inflation from yesterday (though in line) was not enough to derail easing hopes especially after jobless claims came in well above expectations. The Bank of Canada also makes its rate decision next week and is expected to cut rates. What does this mean for markets? As we know, central bank easing is typically bullish. Scotia’s Global Monetary Policy index, which tracks policy changes for 16 banks over a rolling 6 month period, shows that the world is still in “synchronized easing.” In those easing phases, notes Scotia, we tend to get multiple expansion. Bears complain about markets being expensive, but Scotia’s work suggests that multiples could have more room to rise.

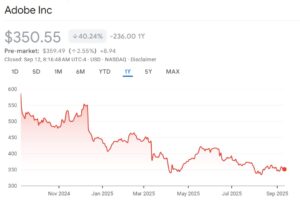

Airbrushed: Shares of Adobe are popping 2.5% after the software provider beat expectations and boosted its full-year forecast. Adobe has been down in the dumps, losing 40% over the past year. Investors are worried that AI is a disruptor to Adobe’s platforms and people won’t pay for things they can do for free on places like ChatGPT. However, Adobe says that their AI-influenced annual recurring revenue has now hit $5 billion (out of $18.5 billion). Another key metric, their net new annual recurring revenue also came in higher than expected. However, Evercore’s Kirk Materne says the results still leave room for concerns. “While F4Q guidance is slightly ahead of consensus, it still implies revenue and (net new annual recurring revenue) deceleration, which will feed into the bull/bear debate regarding the durability of revenue growth…,” he wrote in a note to clients.

Burn the furniture: Shares of RH (formerly Restoration Hardware) are plunging 9% in the pre-market after cutting it’s sales forecast due to weakness stemming from tariffs. RH warned that sales growth will only be 9-11% this year vs the 10-13% in their previous outlook. They said they’ve had to absorb $30 million in costs because of tariffs. Their fall catalog is also delayed due to tariffs because they had to figure out pricing, meaning $40 million in revenue will be pushed out to next year. This will also weigh on the bottom line as the company’s CEO said retailers like them have no choice but to resort to discounting to “stay afloat.”

If you build it: Prime Minister Mark Carney announced the first projects that will be reviewed for fast-track approval in attempt to spark some life into the Canadian economy. The five projects represent a total of $60 billion of new investment and focus on energy and mining: LNG Canada Phase 2, Darlington New Nuclear Project, Terminal Container Project, Saskatchewan Copper Mining Project, mining project in BC. “There is optimism that suggests a ‘buy Canada trade’ continues to emerge, potentially with favourable implications for the Canadian dollar versus the U.S. dollar,” wrote Scotia’s Patrick Bryden of the announcements, “We believe there is an opportunity to foster superior earnings and GDP growth, through several parts of the economy, accompanied by expanding equity valuation in the marketplace.”

Notable calls: General Motors is higher after being upgraded at Barclays. While tariffs are still a blight, analyst Dan Levy says these are “well understood” by the market at this point. Levy believes GM will see a favourable environment due to EV regulations easing while also having strong pricing power. Applied Materials was cut to neutral at Mizuho. The analyst is warning of more competition coming from China. The semiconductor capital equipment company is also exposed to uncertainty regarding Intel’s capital spending plans. Novartis is getting its wings clipped by Goldman Sachs which is downgrading the stock to sell. Novartis has been a rare bright spot in a beaten up healthcare sector. Goldman is ringing the register saying valuation looks “stretched.”

Don’t miss our next episode on Canadian value stocks!

![]()