Jobs day, Amazon dips, smaller tech pops, BCE downgraded, Nike cut

Child 3 is on the verge of a new milestone: dropping his nap. I don’t know if I am prepared to have all my kids awake for the entire day. Having all three talk back to me is already quite an adjustment.

If you missed this week’s episodes of In the Money with Amber Kanwar you can watch Barry Schwartz of Baskin Wealth and Martin Pelletier of TriVest Wealth on YouTube now! Next week we are talking crypto with Matt Hougan of Bitwise Asset Management and tech with Ross Gerber of Gerber Kawasaki. You can email your questions to questions@inthemoneypod.com

Jobs day: Canada added many more jobs than expected in the month of January while the US added fewer jobs than expected. Canada added 76,000 new jobs compared to the 25,000 that was expected and on top of 91,000 created in December. Under the hood it looks pretty solid. Yes there was a big gain in part-time (+41,000), but there was also a surge in full-time (+35,200). Public sector employment fell (-8,400) while private payrolls (+57,200) and self employment (+27,400) increased. Furthermore, the unemployment rate actually fell to 6.6% against expectation it would increase to 6.8%. In the US, futures are mildly lower and bonds are dipping after job growth disappointed. The US added just 143,000 new jobs in January vs the expectation for 175,000 new jobs. The unemployment rate fell to 4% and average hourly wages rose. With that out of the way, enjoy a restful weekend and lets hope there is no ugly surprise waiting for us like the last two Mondays (DeepSeek and tariffs).

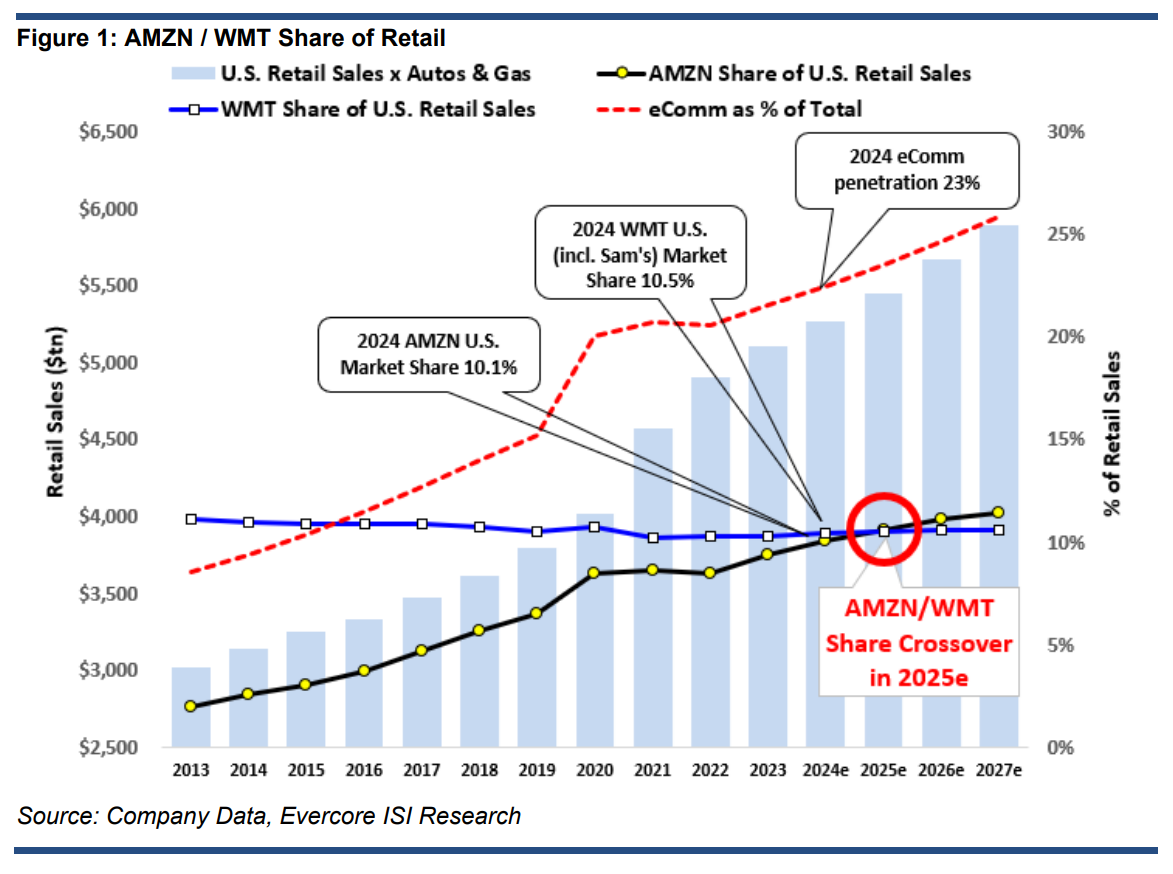

Crossover year: Shares of Amazon are falling 3% despite beating quarterly expectations as cloud growth of 19% failed to impress investors and its forecast for the upcoming quarter was lower than expected. CEO Andy Jassy said growth for its cloud business will be “lumpy” due to capacity constraints but said “its hard to overstate how optimistic we are…” While many know Amazon as an online retail giant, the bulk of their profit comes their cloud business, Amazon Web Services. The cloud business was 15% of sales this quarter but 50% of profit. While the business is growing at a respectable clip the reaction in the stock mirrors what we saw from Alphabet and Microsoft. This now makes four of the Magnificent 7 that have sold off after reporting quarterly results that didn’t live up to expectations (Microsoft, Alphabet, Microsoft, Apple). Like the others, Amazon has big spending plans for AI forecasting $105 billion in capital expenditures for 2025 (compared to $75 billion for Alphabet and $80 billion for Microsoft). The three companies alone make up $260 billion of spending and doesn’t include the “hundreds of billions” Meta plans to spend. This should all be bullish for Nvidia. Under the hood, Amazon showed plenty of strength in the quarter. Total sales increased 10%, operating income was 11% higher than expected, and its operating margins were at a record high. And while cloud is important for investors, 2025 could be a milestone year for Amazon’s retail business. For the first time Amazon’s total revenue is expected to exceed Walmart’s total revenue. Considering these two retail giants have been battling it out for decades, it is remarkable it has taken Amazon this long to reach this point. Evercore’s Mark Mahaney is recommending you buy the dips this morning. “So what we have here is an Expectations Corrections…not a Fundamentals Correction,” he wrote in note to clients. He sees 20% upside from here and plenty of catalysts including a comfortable $100 billion cash pile.

Heavy lifting: It’s not all bad in tech. Shares of Pinterest (+20%), Expedia (+11%) and Cloudflare (+10%) are working to offset the drag coming from Amazon. Pinterest is soaring after hitting $1 billion in sales for the first time ever and forecasting double digit sales growth. Its a nice lift for a stock that is down 60% from the pandemic. This quarter Pinterest’s monthly active users grew 11% to 533 million and key measures of engagement rose. Put simply, more people are on Pinterest and those people keep coming back. “With AI relevancy driving engagement…we emerge from 4Q with greater conviction that Pinterest is in the earlier days of its transition to an always-on, performance platform,” wrote Citi’s Ronald Josey. Expedia is headed for its best day in a year as it posted stronger than expected bookings, signaling strong demand for travel. It echoes what we have heard from the US airline carriers and we are seeing shares of Airbnb and Booking.com rally in the pre-market. Cloudflare is higher after besting expectaitons and doing a better job of selling its software. However, with the stock up 70% over the past year and trading at 178x forward earnings, Oppenheimer is downgrading on valuation. Nevertheless, even Oppenheimer admits the business is doing well. “Sales force productivity has inflected and bookings are starting to grow, which along with improved product and evidence of a dominant AI inferencing advantage, will drive growth above 30% again,” wrote Oppenheimer’s’ Timothy Horan.

Class pet: Arc Resources is one of the most universally loved energy stocks on Bay Street (17 buys, no holds, no sells). It just reported quarterly results earning that reputation. Production came in slightly better than expected while cash flow was “notably ahead of estimates” says Patrick O’Rourke of ATB Capital. Importantly, he says, the company appears on track with the ramp of its Attachie natural gas play in BC. “…Which should at least partially alleviate some market concerns with respect to start-up and operational risk at the hallmark project,” wrote O’Rourke.

Notable calls: BCE is getting downgraded at JPMorgan after the stock fell 6% yesterday on the back of earnings. With the stock trading near a 14-year low you could argue they are a little late to the downgrade, but I digress. JPMorgan is warning about the increased likelihood of a dividend cut as the reason for the downgrade. Recall, yesterday I wrote about new language that was inserted about the dividend that hinted maybe it was up for debate. JPMorgan believes those comments “leave the door open” for a dividend cut. However, a dividend cut may actually be a catalyst according to Jerome Dubreuil at Desjardins. “Our conversations with investors have shown increasing support for an important dividend cut,” Dubreuil wrote in a note to clients, “especially as the company enters an investment phase in the US. While a cut may not be a silver bullet for the stock, it would put the company on a healthier capital allocation track.” Citi is downgrading Nike after meeting with the new CEO Elliot Hill. Never a good sign when meeting with management makes you feel worse about a company. “After discussing the key building blocks and challenges to achieve a turnaround, we no longer believe F26 will inflect the way we hoped, either on the sales or EBIT margin line,” wrote Paul Lejuez of Citi. “We believe F26 consensus ests are too high, making the turnaround timing much less visible, and we no longer have the patience or conviction to wait another year, especially with the stock trading at 39x our F26EPS and 28x our F26EBITDA.” Too bad, I own Nike for the turnaround. On the flip side, he is upgrading Deckers after a recent sell off. “We believe the 24% sell off in shares post 3Q is unwarranted, and largely driven by fears of slowing Hoka growth, which we view as misunderstood/overblown,” he wrote.