Futures lower, Scotia & BMO beat, Home Depot grows, TFI changes its mind

I had a dream someone was asking why I looked so tired all the time. I replied that every morning my eldest is at my bedside no later than 6am. Everyday, no matter what time I sleep, I am always up by 6am, seven days a week. I never got a chance to get their response because it was 6am and you-know-who was doing her morning rounds.

A new episode of In the Money with Amber Kanwar is out now! We talk about investing in the space race. Some of these stocks have rocketed up 500% or more. I spoke with Justus Parmar of Fortuna Investments to find out what is behind the rally, where to find opportunities and why the sector isn’t just for billionaires any more. Listen on Apple, Spotify, or here. YouTube will be out later today!

Today’s newsletter is brought to you by BMO. We all want to make the most of our investments. That’s why BMO InvestorLine is here. Their easy-to-use platform, packed with tools, resources, and commission-free trading on over 100 popular ETFs, can help you trade with confidence and take control of your financial future. Learn more here.

Weary: Futures are indicating a lower open after a weaker session yesterday driven by tech stocks. The TSX was saved once again by a rally in gold and other defensive sectors like consumer staples. The NASDAQ is now in the red for the year and the Magnificent 7 has slumped to a nearly 2-month low. Investors were selling the big winners of 2025 yesterday with shares of Palantir and Super Micro the biggest losers. In fact, Palantir was the best performing S&P 500 stock just last week, today it isn’t even in the top 10. (We touched on Palantir on the podcast today, Parmar said he would buy). Today on the TSX is all about bank stocks with Scotia and BMO reporting (more on that below). Nvidia is in a funk ahead of earnings tomorrow, the stock has lost 7% in the last two trading sessions. Crypto is succumbing to the weaker sentiment in tech with Bitcoin dipping below $90,000 for the first time since November and is now at 3.5 month low.

Scotia earnings: Bank of Scotia reported better than expected profit driven by strength capital markets. Positives in the quarter include the earnings beat ($1.76 vs $1.65 expected), strength in capital markets (+37%), and an increase in all-bank net interest margins (the difference between what they make on loans and pay for deposits). Negatives in the quarter were that provisions for loans that could go bad was higher than expected ($1.16 billion vs $1.11 billion expected) and higher impaired loans and delinquencies in the Canadian banking division. These could stunt the stock today. “Scotia’s results were solid,” wrote John Aiken at Jefferies, “and we would expect to see some relative outperformance. However, given a miss on Canadian Banking and the fact that capital markets was the driving force, we would expect some of the enthusiasm to be muted.” So far in 2025, Scotia is the worst performing Canadian bank stock. On the conference call, Scotia said investors can look forward to a dividend increase next quarter. Scotia hasn’t increased it’s dividend since 2023 and sports a nearly 6% dividend yield. They also said they expect to engage in share buybacks later this year as their capital levels remain strong. While provisions for credit losses were higher than expected, management said those provisions should be going down this year notwithstanding the impact of tariffs (feels like a bit notwithstanding!)

BMO earnings: Bank of Montreal beat by a wide margin ($3.04 vs $2.41 expected) driven by strength in capital markets, strength in Canadian banking and lower than expected provisions for loans that could go bad. Investors will focus on the better credit quality as that haunted the company last year and led to underperformance. Gabriel Dechaine at National Bank calls this a “great rebound quarter.” When it comes to possible concerns in the quarter, Doug Young at Desjardins says “nothing material stands out.” BMO is the second best performing big 5 bank stock so far in 2025. Canadian banks with US exposure have been outperforming given concerns about tariffs and what that might do to the Canadian economy.

Disclosure: BMO is a sponsor of In the Money with Amber Kanwar

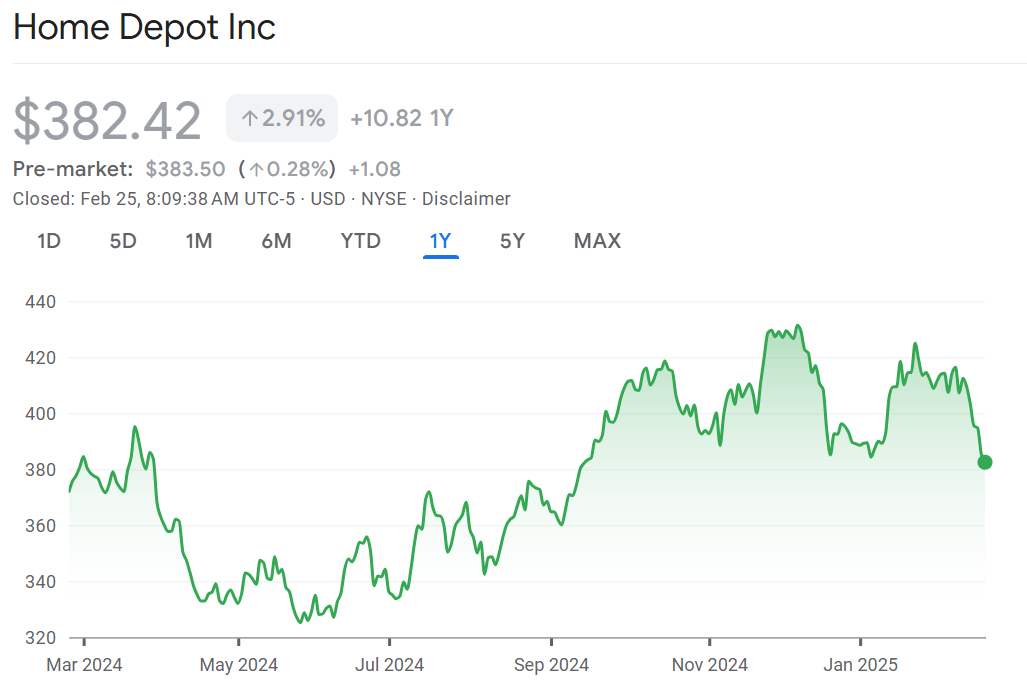

Handy: Shares of Home Depot are flat despite beating profit expectations and posted positive same-store sales growth after eight quarters in a row of declining sales. However, the home improvement retailer’s forecast for earnings was below expectations as they warned sales growth wasn’t going to be as high as analyst forecasts (comp sales +1% in 2025 vs +1.9% expected). Shares of Home Depot have slumped to a 5-month low as consumers put off major home renovations in the face of elevated interest rates and sluggish home sales.

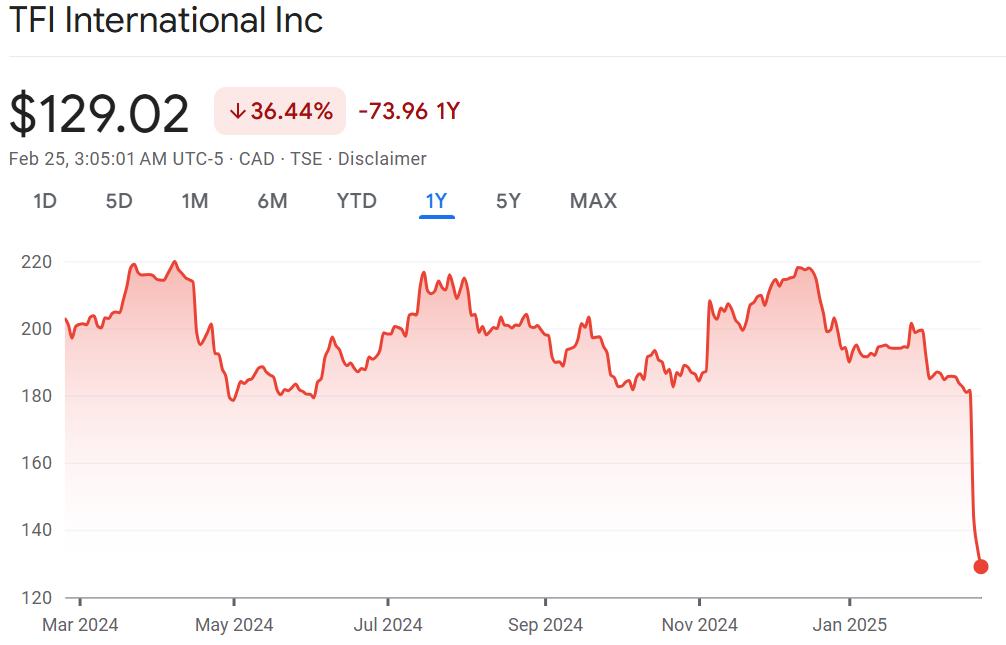

Read the room: TFI International announced that it will not be redomiciling to the US after all. As a recap, the trucking company said it plans to re-locate to the US and saw its shares plunge nearly 20% in a single day. It hasn’t got off the mat since and is trading at the lowest level since 2022. This comes after the Caisse de Depot came out against the move. They are a top shareholder in TFI. The announcement reads like a company who got a tongue lashing and simply declares in a one-sentence press release that they will remain in Canada “based on feedback from shareholders.” On the surface, the decision seemed to make sense. About 70% of its business is in the US. However this comes as Trump has threatened to make Canada its 51st state which has sparked intense patrioitism across the country. I’ll be curious how shareholders respond given TFI’s CEO said the move would help the company win contracts with the Department of Defense. Country over company.