Futures higher, Nvidia tonight, National Bank mixed, EQB beats, Lowe’s beats

People always ask how I manage to get the newsletter out with three kids in the morning. All the credit goes to my husband and my nanny. Today both are out. Dire straights this morning.

The full episode of In the Money with Amber Kanwar featuring Justus Parmar of Fortuna Investments is now up on YouTube! Click below to watch.

Today’s newsletter is brought to you by BMO. We all want to make the most of our investments. That’s why BMO InvestorLine is here. Their easy-to-use platform, packed with tools, resources, and commission-free trading on over 100 popular ETFs, can help you trade with confidence and take control of your financial future. Learn more here.

Nvidia we trust: Futures are indicating a modestly higher open this morning ahead of Nvidia’s quarterly results after the close. If Super Micro is any indication this morning, investors are primed for good news. Shares of the high-performance computer and server maker are surging 24% in the pre-market after finally releasing its delayed financial results and removing the threat of de-listing that hung over the company for months. The results themselves showed sales growing at nearly 55% as it benefits from AI demand. However, that is the slowest pace of growth in more than a year. This is squeezing the shorts this morning, nearly 19% of the shares outstanding are short. Super Micro is the best performing stock on the S&P 500 so far in 2025. Nvidia is set to report quarterly results against this backdrop and the stock has been weaker into the print losing 10% over the last three trading sessions. On the TSX we’ve got 12 companies reporting quarterly results, including National Bank (more below).

Bank beat: National Bank beat earnings expectations following in the foot steps of the other Canadian banks which have also reported higher than expected profit. And just like the other banks, capital markets was the star performer with profit in that division up 62% from last year. There were some blemishes in the quarter. Provisions for loans that could go bad were higher than expected, impaired loans rose (+78% from last year but only 0.79% as a proportion of total loans), and profit in its Canadian banking division was lighter than expected. The stock could take a hit on those issues. RBC’s Darko Mihelic calls the results negative and notes that the bank appears to be warning that provisions for loans that could go bad are set to increase. “Overall, we have a negative view of Q1/25 results as core EPS was results were stronger than our estimate across the board,” wrote Mihelic, “but credit has deteriorated and we have not yet seen any potential tariff impact.”

Small but mighty: Shares of EQB may get a lift after it beat profit expectations and demonstrating better credit quality in the quarter. The alternative mortgage lender managed to beat profit expectations by setting aside far less than expected for loans that could go bad. This comes as the lender saw a big improvement in its embattled long-haul truck leasing business. “We believe this outcome will be particularly well received by investors considering the elevated level of impairments and losses it has generated for over a year,” wrote National Bank’s Gabriel Dechaine, “As such, we view the quarter as a ‘clearing event.’” However, loan growth was a bit muted in the quarter and that could restrain the enthusiasm.

Love it or list it: Lowe’s is up nearly 4% in the pre-market after profit came in better than expected and comparable sales increased for the first time in two years. This is similar to what we saw from Home Depot yesterday. To be sure, growth is still tepid. Comp sales only rose 0.2%, but growth is growth. Home Depot’s results were peppered with caution about demand. While Lowe’s signaled it will grow sales this year by 1% that is less than the 1.4% analysts were expecting. Nevertheless, the stock is in rally mode as it had been under pressure going into the results and the quarter demonstrated improving trends (however minor).

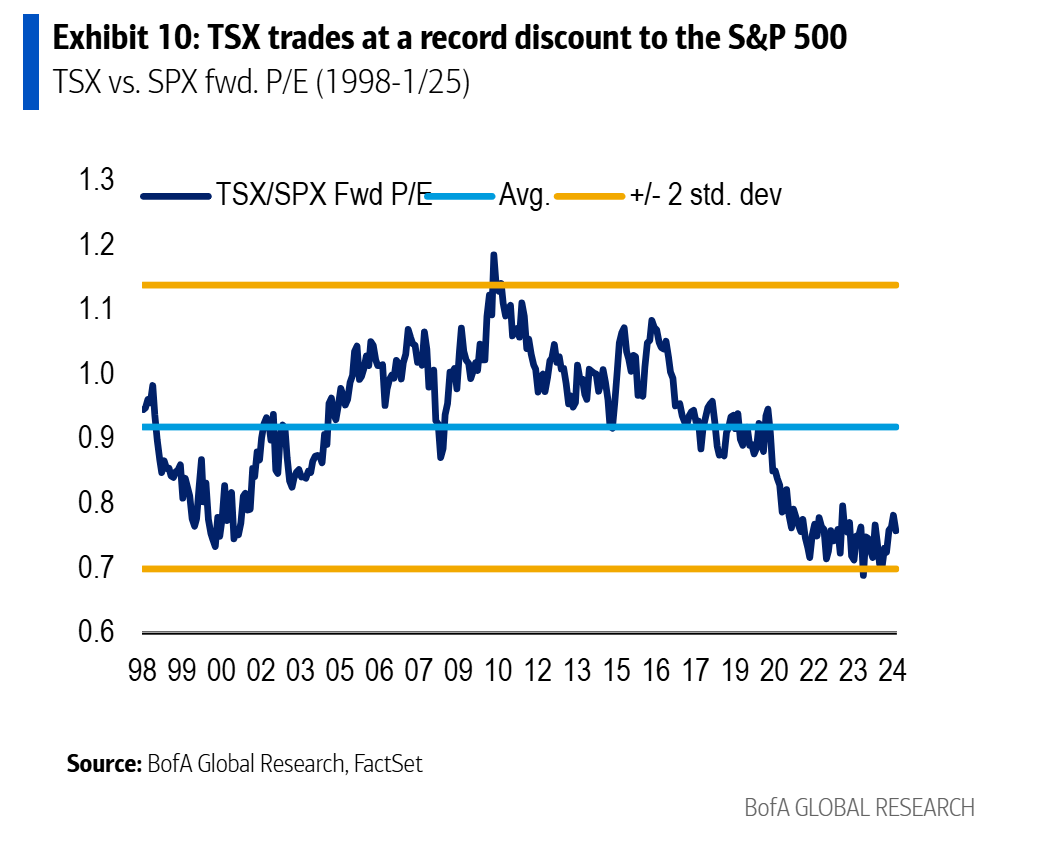

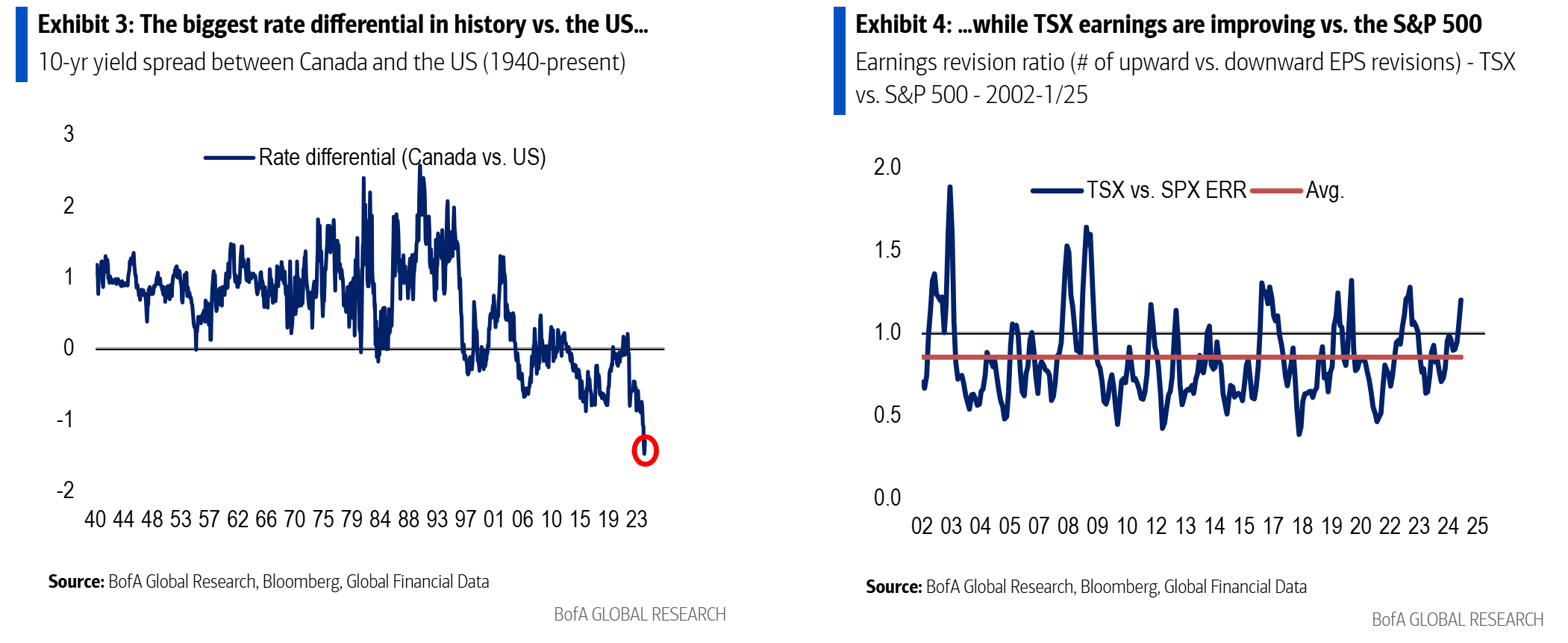

Oh, Canada: Bank of America put out a note yesterday that said Canadian stocks are trading at a record discount to the S&P 500. “On a relative basis, the TSX looks much cheaper, trading at just 0.76x vs. the S&P 500, the steepest discount in history, similar to the Tech Bubble,” wrote Ohsung Kwon of Bank of America. The note goes on to say this is coming at a time when the difference in interest rates between Canada and the US has also never been wider (Canada’s rates are lower while the US is stuck with higher-for-longer). They make the case that this makes a compelling reason to own the TSX especially when you consider earnings are improving. The caveat, of course, is tariffs which could be a 7-11% hit to earnings. However, Kwon notes that so far during this tariff row the TSX has largely performed in line with the S&P 500 which is different from the last tariff tussle in 2018.