Tune in NOW! Listen on Apple, Spotify, or YouTube.

It’s been a rough ride for Canadian small-cap growth stocks, and investors are looking for answers. Jordan Zinberg of Bedford Park Capital is back on In the Money with Amber Kanwar to break down what’s driving the selloff, where the fear is justified, and where the market is simply mispricing good businesses.

1 minute before leaving the house for school Child 1 declares, “I just want to have a quick bath.” It’s the kind of time blindness I find particularly triggering. And it’s genetic. Pre-departure showers when everyone else was already in the car were common place for my dad. Growing up my parents were late to everything. I was the last to be picked up from school, we were that family trying to bud everyone at the airport because we were late for flights, we missed flights and connections routinely. I thought I broke the cycle, with an obsessive need to be on time for things. Clearly it just skipped a generation.

Here are five things to know:

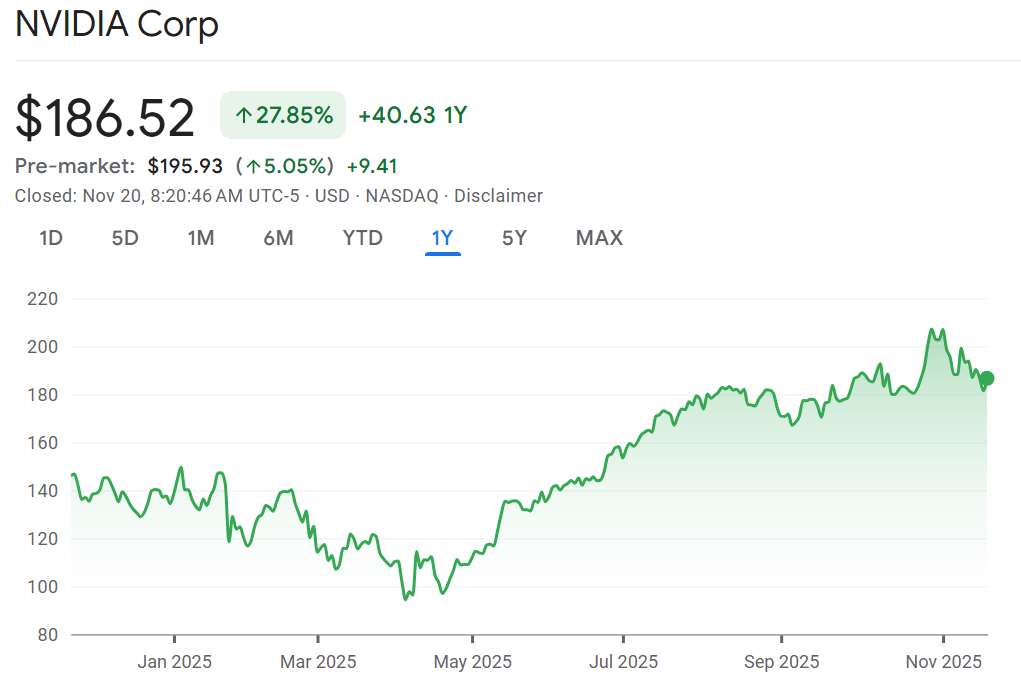

With arms wide open: Futures have their groove back thanks to Nvidia restoring faith in the AI trade. Then we got the delayed jobs report for September which showed the US economy added more than double the number of jobs expected. 119,00 jobs were added in September vs the 51,000 expected. It also marked a resurgence from August which was revised lower to a loss of 4,000 jobs (the second time we’ve seen job losses in 2025). The unemployment rate ticked up 4.4% as the labour force rose. This all shows the job market stabilized right before the government shutdown which will distort the economic data for months (if we get October readings at all). The market is still betting of a low chance of a rate cut by the Federal Reserve. This is the last jobs print before the rate decision on December 10. For now, however, markets are just thrilled to have the void filled with Nvidia results and some data.

Nvidia we trust: Nvidia did what had to be done this quarter, it beat sales and profit expectations and raised its forecast more than expected. Shares are trading up 5%. It’s actually unusual that Nvidia does this well post earnings, notes Deutsche Bank strategist Jim Reid. “Perhaps the difference this earnings season is that this was one of the weakest months before earnings Nvidia has had in the last three years,” Reid wrote in his morning note. Here are the raw numbers: sales grew 62.5%, earnings per share increased 66% and free cash flow exploded to more than $33 billion in the quarter. Demand remains off the charts and the entire tech space is booming this morning with enthusiasm. “While the first steps in AI deployments are around Nvidia chips and the cloud stalwarts, importantly we estimate that for every $1 spent on Nvidia, there is an $8-$10 multiplier across the rest of the tech ecosystem,” wrote Dan Ives of Wedush, “We also believe Nvidia will enter the $6 trillion market cap club over the next 12 to 18 months as the vision and numbers around the AI spending trend prove themselves out.” Meanwhile, accounting sleuths are pointing out some red flags like rising inventory (why if demand is so hot?), aggressive revenue recognition (ie recognizing deals as revenue before shipments), and growing investments in their customers (investments in non-marketable securities jumped to $8 billion from $3 billion at the beginning of the year).

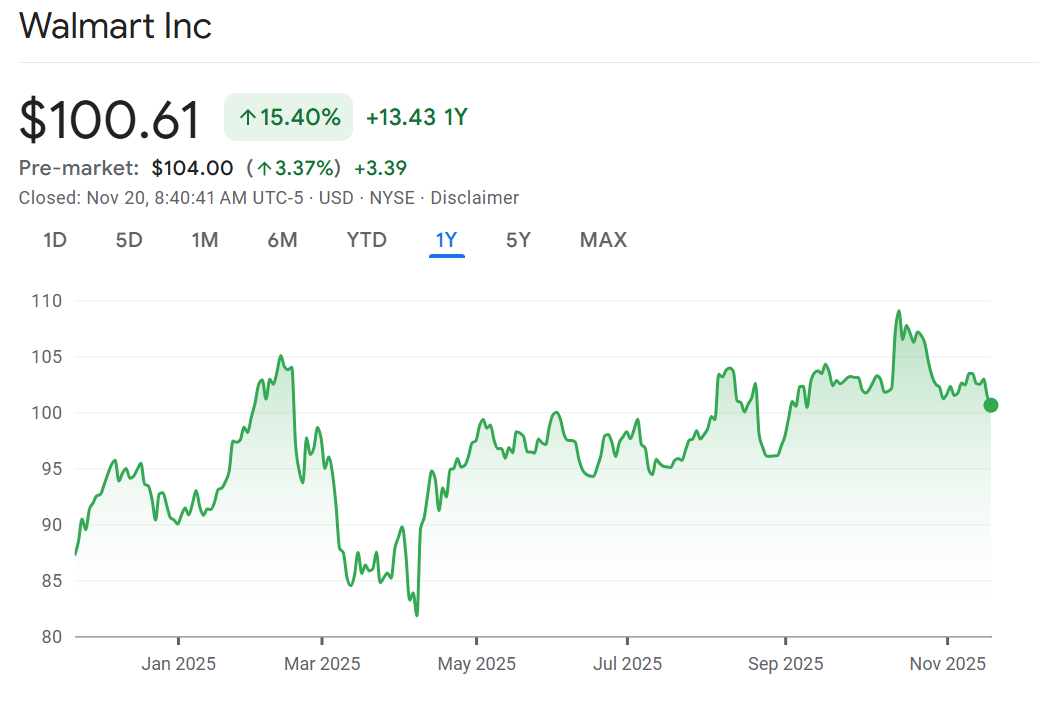

I like big box and I can not lie: Walmart is up more than 3% after beating profit expectations and boosting its forecast. Initially the stock wobbled as the largest retailer on earth warned that higher costs stemming from tariffs, supply chain kinks and rising tech spending. Still, the company was cautiously upbeat about consumer spending saying the holiday season is off to a “pretty good” start. Walmart is spending more time talking about tech, having recently done a deal with OpenAI as showing up in chat bots vs search engines becomes the new entry point for consumers. In fact, the company is doubling down on that tech theme announcing that it will switch its listing to the NASDAQ from the NYSE in December. Considering the stock is trading at nearly 40x earnings, it makes sense that they’d rather be thought of as a tech company than a plain old retailer which typically trades at a much lower multiple.

Hit the showers: Bath & Body Works is plunging 17% after profit missed and sales unexpectedly fell. The retailer is also cutting its forecast now calling for sales to drop this year. The company blamed negative macro environment weighing heavily on consumer buying intent. It is forcing some major changes at the company. It is going to exit men’s grooming and hair care and set up a storefront on Amazon. It’s a win for short sellers with 7.5% of the shares outstanding short.

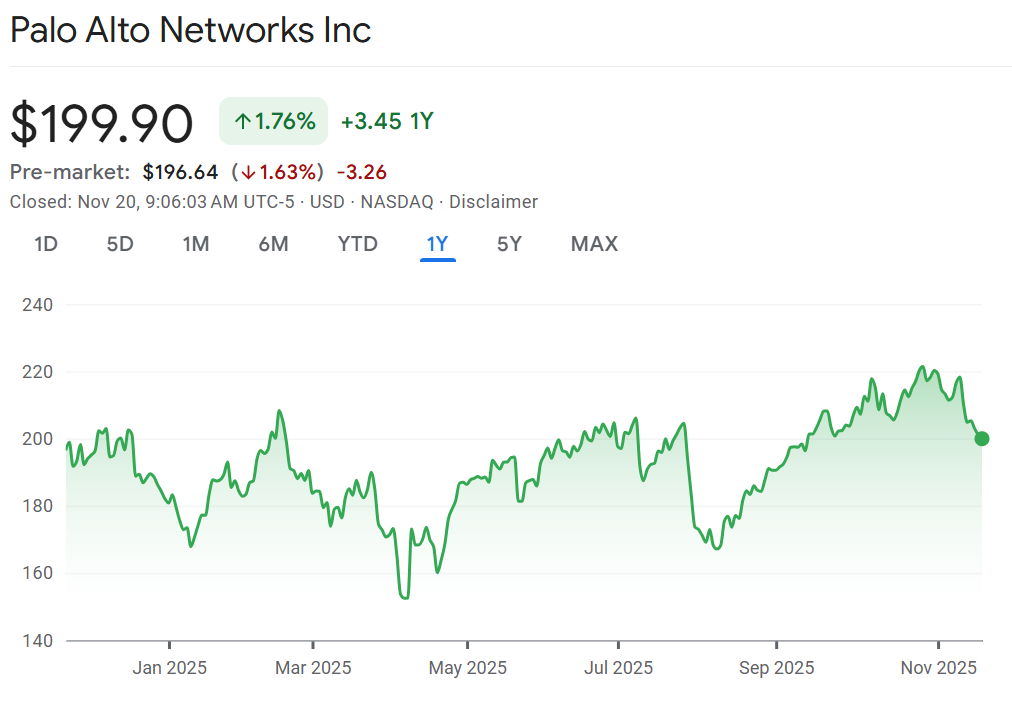

In the dark: Palo Alto isn’t getting the benefit of tech enthusiasm this morning. Shares are under pressure despite better than expected results at the cybersecurity company. Palo Alto announced they would be buying Chronosphere for $3.5 billion and the share price weakness appears to just be on M&A digestion and execution risk. Chronosphere helps big companies find bugs quickly and fix them fast.