Tech is starting to crack and value is outperforming. Where should you be positioned? On this episode of In the Money with Amber Kanwar, the show heads to Phoenix, Arizona for a special on-the-road episode with Bill and Cole Smead of Smead Capital Management, the father-son investing team behind $5.5 billion in assets under management. In a wide-ranging and candid conversation, the duo explains why today’s market setup looks increasingly fragile and where disciplined value investors are still finding opportunity.

You’ll be happy to know my husband came back in one piece from his cat-skiing adventure. After roughing it in a lodge with no heating on a single bed and skiing on over 2,000 metre high mountains he says the most physically taxing part of the trip was sitting in the middle seat on a Rouge flight.

Here are five things to know:

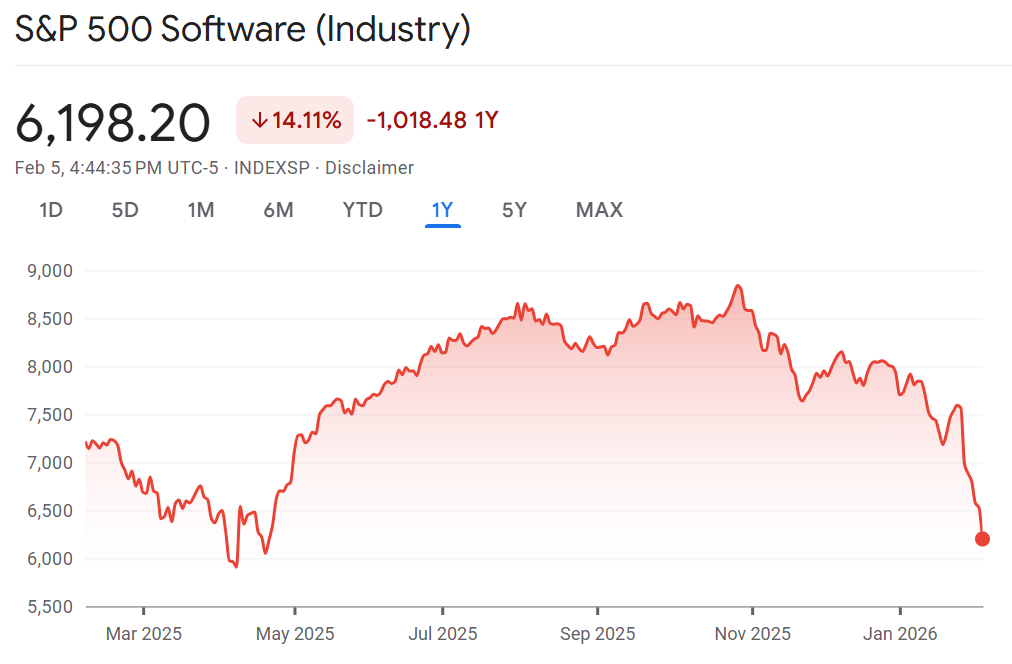

Drunken sailors: Futures are indicating a positive open after a sloppy week for US stocks. Canadian stocks meanwhile enjoyed another week of outperformance despite a nearly 2% sell off yesterday on weaker materials prices. Tech is the eye of the storm. The software sector in the US is down 35% from its peak and trading at a 1.5 year low on fears that AI will eat their business. The tech sector on the TSX is down a similar amount. Amazon joined the spending parade yesterday announcing an eye watering $200 billion in capital expense. With most spending plans laid out, this now means the tech sector is poised to shell out $650 billion this year on AI buildout up from $356 billion last year. “What’s interesting about this is these businesses were asset light and they’re now going to a transition of being the most capital intensive businesses in the world,” said Cole Smead on the podcast, “Now, what naturally happens when you become a capital intensive business, your returns go down…They were the ones that didn’t have to spend the capital in ’99. Now, they’re the ones that have to spend the capital. History never repeats itself, but it rhymes.”

River runs red: Jeff Bezos named the company Amazon after the biggest river in the world to signify the scale of the company’s ambitions. Today, the company is earning its moniker announcing $200 billion in new spending plans – $50 billion more than expected. Amazon shares are down 7% in the pre-market as the higher spending overshadows solid quarterly results. Revenue grew 14% better than expected while its cloud business (Amazon Web Services) grew 24%, the best pace of growth since 2022. The problem is that all this spending will take a bite out of profits. Indeed, the spending plans that Amazon will have negative free cash flow this year (Meta, Microsoft and Google’s spending out of operating cash flow). “The AMZN (return on AI) proof-points are in its AWS results, and AMZN is doubling down,” wrote Evercore’s Mark Mahaney, “We agree with this strategic move. We just don’t like the near-term evisceration of FCF (we estimate approx. negative $10B in FCF in 2026).” Mahaney believes the stock will be range-bound until the market sees potential for free cash flow snapback and/or revenue acceleration this year. I own Amazon.

Edit undo: Canada unexpectedly lost nearly 25,000 jobs in January vs expected 5,000 gain. This is a bit of giveback from the stronger than expected job growth we’ve seen over the last four months. The manufacturing sector continues to be punished by tariffs shedding 27,500 jobs. Public sector employment increased 13,300 while private sector payrolls fell 52,000. Some positives: The unemployment rate fell to 6.5% (fewer looking for work + less immigration), most of the losses in part-time (-70,000), full time employment +45,000. Yesterday, Bank of Canada Governor Tiff Macklem suggested that rate cuts would not aid structural problems.

Into the unknown: Arc Resources may come under pressure after removing an embattled natural gas development, Attachie, from its forecast and pausing development on a once promising new growth area. “Pads at Attachie, brought on stream in late 2025 and early 2026, have been variable and below expectations,” the company said in its earnings release. While the company is maintaining its overall production forecast (Attachie is only 7% of production) analysts warn this could overshadow solid results. “ARC now lacks a near-term catalyst for improved Attachie I performance, any credit for Phase II potential, and a multi-year liquids growth strategy,” wrote Aaron Bilkoski of TD Cowen. The development overshadows stronger than expected production in the quarter and significantly higher cash flow per share. Bilkoski expects this will be overlooked but ultimately believes Arc is doing the right thing. “Attachie has lagged expectations for over a year. It still isn’t working as expected and, as painful as it may be, pulling Attachie-level guidance in face of obvious asset uncertainty is the most prudent course of action at this point.” The company will be redirecting planned spending of $350 million toward a share buyback instead.

X marks the spot: TMX Group beat sales and profit expectations on the back of strong organic growth and contribution from its US-based options exchange. This could provide relief to investors who have been anxious about how generative AI will hurt exchanges like the TMX Group. Shares of TMX Group are down 20% from their July record high. I’m listening to the call for colour on how they will defend against AI. They’ve referenced the sell-off this week as creating potential opportunities on the M&A front. RBC says so far there is nothing in the results to indicate an AI-related slowdown. TMX Group increased its dividend 9%.

Don’t miss our next guest! Email your value questions to questions@inthemoneypod.com

![]()