“I hate this market. It’s funny because we are strongly outperforming, but I still don’t like this market.” That’s how dividend investor Rebecca Teltscher, Portfolio Manager at Newhaven Asset Management, sums up today’s market on this episode of In the Money with Amber Kanwar. Value is working. Dividend stocks are back. Utilities, pipelines and energy have seen major inflows. And yet, Rebecca says this is one of the hardest environments she’s seen to deploy capital, with sectors moving quickly from unloved to fully valued.

The kids were oddly quiet this morning. The kind of quiet that as parents we have learned not to trust. By 7:20am no one had come down to our room. Turns our Child 1 had jacked an iPad from dad’s office and was stowed away under a blanket with the siblings watching YouTube. A big no-no in this house. But they knew that and once busted it induced the kind of compliance we can only dream about and we had one our smoothest mornings ever. Now I’m thinking about whether I can plant candy under their pillows to catch them in the act and see how much smoother our weekend could be.

Here are five things to know this morning:

TGIF: US futures are sharply lower this morning after a read of producer prices came in significantly higher than expected. Producer prices excluding food and energy were up 3.6%, much higher than the 3% expected and the fastest growth in 10 months. The prospects of rate cuts were already diminishing this year, but eroded even further after the print. In Canada we got a read of GDP which showed the economy contracted 0.6% for the fourth quarter, worse than the 0.2% contraction feared and the Bank of Canada’s own projections. However, December’s growth was much stronger expanding 0.2% from the previous month. “While the Bank has suggested that weak GDP readings are largely the result of structural rather than cyclical factors, that explanation will be harder to sell if progress on reducing unemployment stalls or reverses,” wrote CIBC’s Andrew Grantham.

AIverse: AI is a wrecking ball this morning, separating winners and losers.

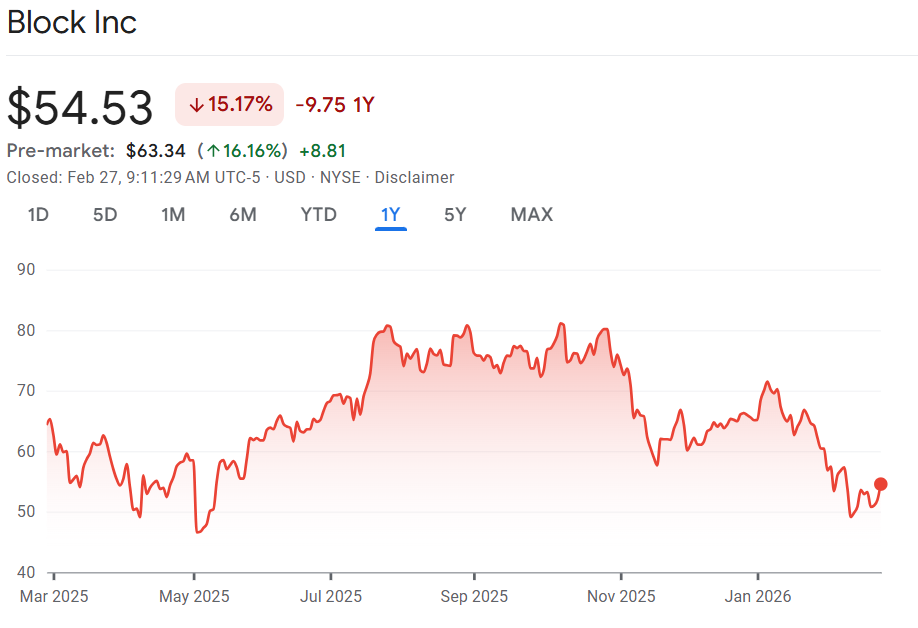

- Block +16%: Less than a week after the Citrini report came out that warned about a dystopian AI future characterized by huge job losses, Block announced it was cutting 40% in a bet that AI can replace those workers. That’s 4,000 jobs lost as a result. The financial services and digital payments company helmed by Jack Dorsey is soaring 20% in the pre-market on the news. If you are the CEO or CFO of a struggling software company, maybe you look at this announcement as a model. On the other hand, Block has been restructuring for years and is seen as a bloated enterprise so AI could just be an excuse to make long overdue moves. We will see who goes next.

- CoreWeave -12%: A bigger than expected loss and warning of bigger than expected spending plans for 2026. The AI cloud computing company rents out access to AI semiconductors and computing power boasting customers like Microsoft, OpenAI and Meta. “Revenue bracketed guidance versus a traditional ~$hundred-million beat, and adj. operating income missed with stronger capex and other costs ramped faster than expected,” wrote Citi’s Tyler Radke, calling this a delayed gratification story, “Stepping back, Coreweave is delivering one of the fastest ramping infrastructure businesses seen in the tech industry. We believe the combination of growth + scale and more evidence of ramping margins (something expected more in the 2H of 2026) will help reinforce the company’s standing.”

- Dell +11%: Outlook for AI server sales exceeded expectations. Dell’s AI servers are used by company’s like CoreWeave so their spending plans are bullish for Dell’s prospects. The reported quarter was strong, earnings were a record, it boosted its dividend and showed healthy margins despite rising memory prices.

- Duoling -25%: Its sales and profit outlook came in worse than expected. The mobile platform for learning new languages has been disrupted by AI platforms that can do much of the same for free. Sales still grew a healthy 35%, but the pace of growth is slowing. I’ve counted at least six downgrades this morning.

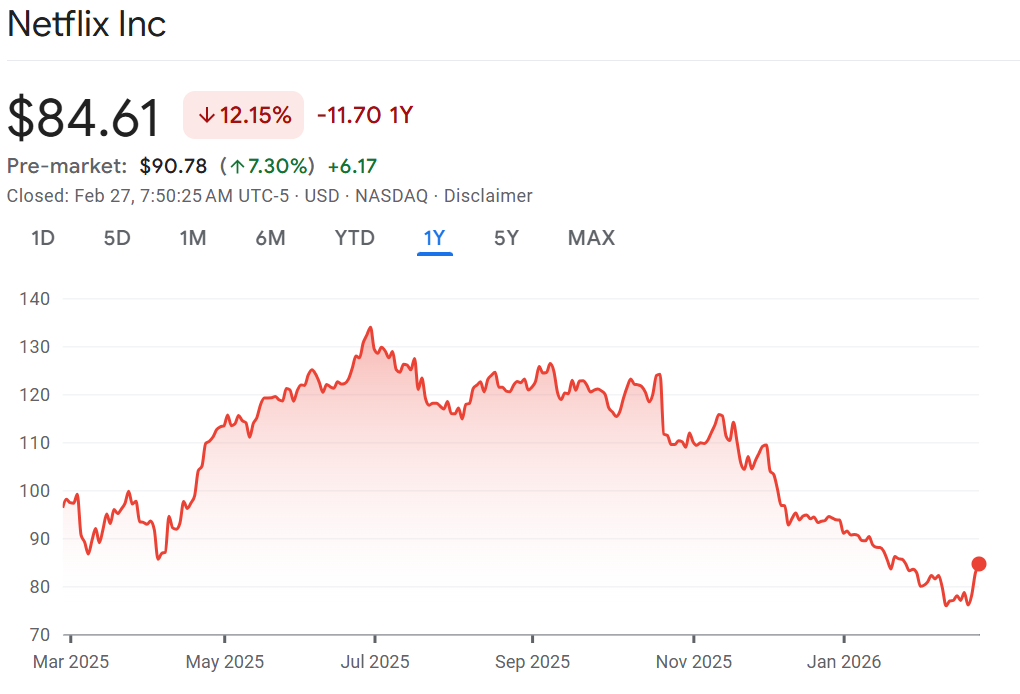

Netflix and chill: Netflix is dropping out of the bidding war to buy Warner Brothers ceding the company to Paramount Skydance. Netflix said the price required to match Paramount Skydance’s $111 billion offer “is no longer financially attractive.” Shares of Netflix are soaring 7.5% in relief. It’s a deal investors never loved with the stock down 18% since the bid was formally announced. Warner Brothers management has now said they are excited about the prospect of joining forces with Paramount Skydance, which is controlled by billionaire Larry Ellison who is an ally of US President Donald Trump . The deal now means that the new company will house TV networks like CBS and CNN under one roof. Netflix will get a $2.8 billion break fee. Netflix says it will spend $20 billion on content this year and resume share buybacks. “We believe those buybacks will be the main use of the freed-up dry powder, but now that the company has gotten a taste of the M&A landscape, we cannot rule out other options,” wrote Ric Prentiss of Raymond James. If you are looking for the next consolidation play in media, consider Lionsgate says Prentiss. Shares are up 3% in the pre-market right now. “LION would be a much smaller and digestible studio to buy than WBD, and we believe the pool of buyers could be larger,” wrote Prentiss. I own Netflix.

ATRL IRL: Watch AtkinsRealis after profit and sales beat expectations and it boasted a record backlog of projects. However, the outlook is mixed. The engineering and consulting company said overall revenue growth would be 5-7% vs the previous outlook of 8%. The company raised its outlook for nuclear sales however lowered its margin outlook in that segment. In the reported quarter it higher revenue than expected in every business line, however adjusted profit was dragged by stalled legacy projects (Eglington LRT etc). We will see if it is enough for shareholders, as the stock has come under recent pressure with other consulting peers. Shares of Stantec and WSP have taken a hit alongside software companies on concerns AI will eat their business. AtkinsRealis is more diversified and has exposure to a small but growing nuclear business. “There were some puts and takes on the outlook that do not structurally change how we think about this name now, which can summed up as a “safer” name to own now for those concerned about the engineering space in general due to company’s 21% top-line exposure to nuclear (and 37% of NAV),” wrote National Bank’s Maxim Sytchev.

Rusty pipes: Pembina Pipeline could come under pressure after profit and sales missed expectations and BMO downgraded the stock after the miss. The pipeline division was the key source of the miss. BMO is downgrading the stock on the back of valuation. “We believe the recent ~15% run-up in PPL shares leaves the stock reasonably valued in the context of its future organic pipeline,” wrote BMO’s Ben Pham in the downgrade. Valuation concerns on the pipes were discussed on the podcast with Rebecca Teltscher saying the sector has gotten overvalued.

Email your questions now! Questions@inthemoneypod.com

![]()