It’s a shortened trading week for US investors, but lots of market moving things coming out this week. Here is a preview in my Globe and Mail column.

Here are five things to know today:

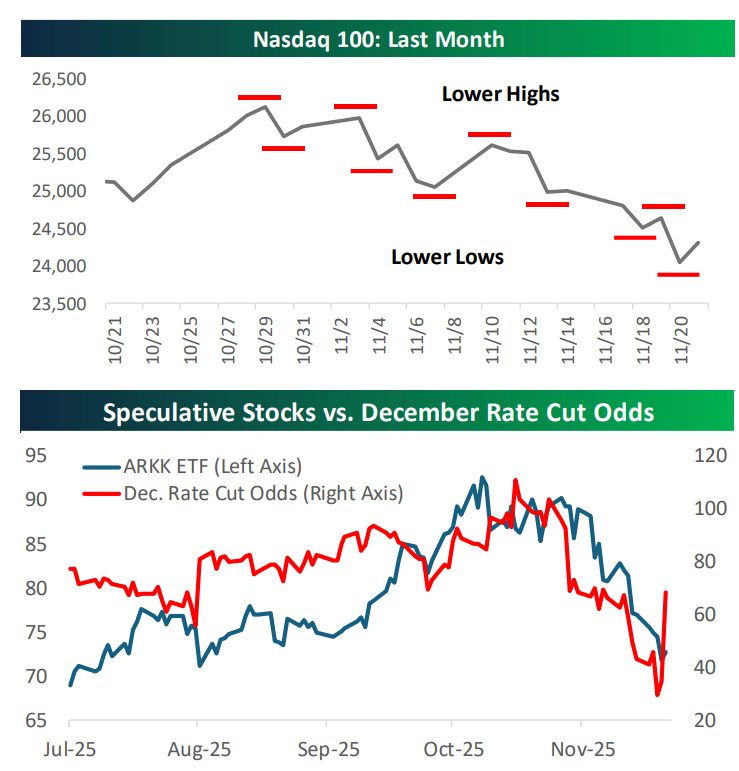

Keeping hope alive: Futures having some pep in their step after comments from NY Fed Governor Williams on Friday in which he said there is room for a rate cut near term. Williams word carries more weight than others and his comments were seen as de facto message from Fed Chair Jerome Powell himself. Odds of a December rate cut shot up to 70% and helped to support a Friday rally. Still, quite a bit of damage has been done. Particularly to the NASDAQ which is down 6% so far in November. The first chart below from Bespoke suggests a trend breakdown. However, if a rate cut materializes, the sector could see a bounce (see second chart). This morning, Alphabet (+4%) is propping up the the tech sector after the roll out of Gemini 3 – its answer to ChatGPT – was seen as higher functioning than other LLMs. Salesforce CEO Mark Benioff tweeted he is so impressed he will never go back to ChatGPT.

Race to cure Alzheimer’s: Novo Nordisk is plunging 10% after its Ozempic pill failed to halt the progression of Alzheimer’s in clinical trials. This was viewed as a key catalyst for the stock which has fallen badly behind Eli Lilly. Shares of Novo are poised to open at a 4-year low. Meanwhile Eli Lilly recently joined the $1 trillion dollar club and shares are up 40% over the past year. Novo’s loss is Biogen’s win as it keeps their Alzheimer’s treatment in pole position and the stock is trading up 5% in the pre-market. RBC believes this should clear the way for Biogen to start to outperform. ” BIIB has continued to trade at a discount to what we believe is fundamental fair value, we believe in part due to the overhang around this GLP-1 Alzheimer’s data, and with the evoke studies now out of the way, we believe this gap can start to close into what we expect will be a more eventful 2026,” wrote RBC’s Brian Abraham.

Bowing out: BHP has tried and failed for a second time to secure a deal to buy Anglo American and is now walking away. This clears the way for Anglo’s no premium deal for Teck Resources. The tie up between Anglo and Tech would make it the fifth largest copper producer in the world. Shareholders will vote on the deal December 9th. The deal still requires regulatory approval and reports suggest Canada is looking for concessions including the corporate head office remaining in the country in exchange for its seal of approval.

Day by day: Barrick is being upgraded at Bank of America against an increasingly interesting backdrop. Recall it started in September when CEO Mark Bristow abruptly left, then there was a management shakeup and recent media reports that activist investor Elliott Management has taken up a big stake in the company. Bank of America likes this set up against higher gold prices and attractive valuations. Barrick is also reportedly in negotiations to regain control of its giant mine in Mali which would end a two-year dispute with the government which shuttered the mine. Shares surged 3% after the report from Bloomberg. Buying Barrick was a top call from Kim Shannon on our podcast in mid-September before all the changes. The stock is up 26% since that episode vs just 7% for the index.

Notable call: Desjardins is downgrading Canadian Natural Resources to hold and upgrading Tourmaline and Peyto to buy. Canadian Natural Resources is being downgraded as it continues to digest its acquisition of assets from Chevron. “Although we continue to support the strategic rationale and industrial logic of the transaction, it has materially increased the company’s financial leverage while weighing on capital returns through a reduced 60% FCF allocation to share buybacks (from 100% previously) after funding dividends,” wrote Desjardin’s Chris MacCulloch. On the flip side, MacCulloch is upgrading Tourmaline after the stock underperformed on spending intentions and lower free cash flow profile. MacCulloch argues that is fully baked in the stock while it sits on the cusp of many catalyst including higher natural gas prices as we head into winter and the sale of Peace River High assets. Peyto is being upgraded as well which is more of a mea culpa for MacCulloch. “(Peyto) has delivered a colossal 87.0% return, significantly outperforming the S&P/TSX Capped Energy Index return of 29.0% (excluding dividends). Simply put, we got this call wrong and we believe there’s no better time to get off a bad call than the present!”

Don’t miss our next episode!

![]()