We’re looking ahead to the crucial Fed decision next week — and the central bank may be on a collision course with the market, with inflation, and possibly with its own incoming leadership. Amber sits down with Dustin Reid, Chief Strategist, Fixed Income at Mackenzie Investments and he explains why he thinks the Fed will be done cutting rates after December and why the Bank of Canada won’t be. Tune in to these out of consensus calls now! Listen on Apple, Spotify and YouTube.

QUICK SURVEY: I am partnering with Questrade for December and would be grateful if you could fill out 15-second survey before our campaign begins!

Everyone has been tagging us in their Spotify wrapped showing that we are in their top 5 list. To reward that loyalty we are doing a surprise Christmas swag giveaway! Tag us on X or Instagram @inthemoneypod with your wrapped list and we will send you some sweet sweet swag!

Here are five things to know:

Silent night: It is a quiet tape this morning with investors leaning on previously ignored economic data in the absence of official government data about the jobs picture. Layoff announcements increased 23% from last year, but are less than the previous month and less than expected. Initial jobless claims came in lower than expected. Regardless, the market is betting it is a done deal that rates will be cut next week by the Federal Reserve. In the podcast this morning Dustin Reid makes the case for the Fed to be done cutting rates after this despite pressures from the White House. It’s a good listen! In Canada, we have the banks guiding the tape while gold is modestly lower and oil is modestly higher.

Bank beat: CIBC, TD and BMO all reported results this morning.

- CIBC beat profit expectations but analysts are flagging some credit quality concerns. On the positive side, CIBC’s profit rose 16% which was higher than expected, it boosted its dividend by 10% (also more than expected), margins were up across most units, and capital markets profit surged 62% from last year. On the negative side, performance at its Canadian banking unit were mixed. Profit was up 14% from last year, but down sequentially as provisions for credit losses came in higher than expected and impaired loans rose. “Credit concerns have caused some investor caution, which may limit CM’s upside,” concluded John Aiken at Jefferies. However, at this moment shares are higher in the pre-market.

- BMO beat profit expectations, boosted its dividend 2.5%, and surprised investors with lower than expected provisions for loans that could go bad. Recall, credit quality concerns particularly in the US hampered the stock in 2024. BMO is releasing some of those reserves for its US business in a sign of recovery, while increasing them here in Canada.

- TD beat profit expectations aided by strong capital markets growth and lower than expected provisions for credit losses, boosted its dividend (although it was less than expected), and showed robust growth in the US despite its asset cap. TD can not grow its asset base in the US beyond $434 billion as a result of penalties from regulators due to its anti-money laundering lapses last year. TD still managed to grow profit more than in the US and noted that it still has room to grow under the asset cap as current assets sit at $382 billion.

- RBC reported yesterday is getting upgraded to buy at TD. “RY should benefit from HSBC-synergies, AI-related savings, deposit mix, and better loan growth,” said TD’s Mario Mendonca in the upgrade. “In 2025, RY has been the worst performing stock among the Big 6 and the stock now trades at a modest 3% premium to group. In upgrading the stock, we are setting our target P/E at 7% premium to group. When RY is functioning at a materially higher level, the premium can reach 10%+,” he wrote.

Shooting their shot: Watch EQB at the open after profit materially missed expectations and they surprised investors with an $800 million purchase of PC Financial from Loblaw in a mostly stock deal. First on the results of the alternative bank lender, profit missed expectations and provisions for loans that could sour was higher than expected. You could say that is them being conservative in case things go bad, but impaired loans continue to be on the rise at EQB. “Unless the company can convince the market that it has isolated credit issues to certain vintages/municipalities and conservatively provisioned these loans, the credit overhang weighing on the stock will persist,” wrote National Bank’s Gabriel Dechaine. These are all challenges for new CEO Chadwick Westlake who is only three months into the job after the sudden passing of CEO Andrew Moor. Analysts are also raising their eyebrows over the $800 million acquisition of PC Financial. The deal will add 2.5 million customers to EQB, be accretive in year 1 of closing, and the company will become the exclusive financial partner of the PC Optimum loyalty program. At the same time, Loblaw will own 17% of EQB with the option to go as high as 25% and get two board seats. While many analysts say the deal makes strategic sense, some fear it is not a home run. “The deal is being primarily financed by issuing EQB shares at a relatively depressed level (-12% ytd and trading at 1.1x P/B), and PC Financial credit card portfolio growth has been muted (L3Y CAGR of 2%),” wrote TD’s Graham Ryding.

Inertia: Salesforce shares are up 1% in the pre-market after profit beat expectations despite sales missing estimates and it boosted its forecast touting AI demand. Still, considering the stock is down 35% over the past year this mornings gain is hardly unbridled enthusiasm. Salesforce has been struggling because of softness in their core business and slow monetization of their AI offering. Agentforce, their AI sales tool, saw annual recurring revenue soar 330% but at $540 million it is a drop in the bucket for a business with $40 billion in sales. “Although results exceeded expectations, we see limited catalysts for multiple expansion given stable growth and margin trajectory,” wrote RBC’s Rishi Jaluria.

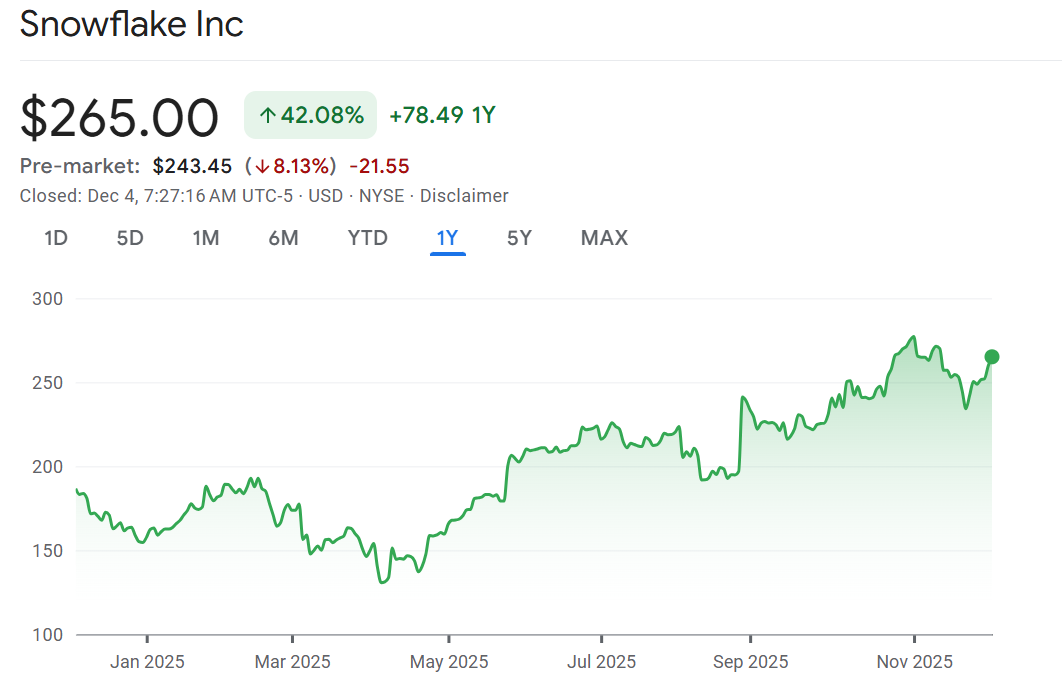

Melting: Shares of Snowflake are dropping 8% as it increased its sales forecast but kept its margin forecast the same stoking fears about the cost of chasing AI. The cloud-based data software platform showed an impressive 29% increase in revenue in the quarter, but is still losing money. Analysts see a lot of positives in the quarter despite the sell-off this morning. First, the total value of customer contracts grew more than the last quarter. Second, it crossed $100 million in annual recurring revenue from AI a full quarter ahead of expectations. Third, the total number of new customers was higher than the last quarter. “Overall, we continue to believe that SNOW is well-positioned to be a key 2nd derivative in the AI Revolution as it will continue to benefit from the significant acceleration of use cases and a rapidly growing pipeline,” concluded Dan Ives at Wedbush.

Don’t miss our next episode! Get your questions in now! Email questions@inthemoneypod.com

![]()