On this episode of In the Money with Amber Kanwar we speak with Amber Fairbanks of Impax Asset Management to unpack the ESG backlash, the performance debate, and why she believes sustainable investing isn’t a label — it’s simply long-term investing done right.

My daughter was watching a show where the kids were roasting “Millennial Pink” aka the Barbie-core lewk that took over when the movie was released. I really over-indexed on that trend and have a head-to-toe pink suit to prove it. Trying not to have a full blown crisis that my generation is now being mercilessly teased as if we are…boomers? Anyway, if anyone needs a shockingly pink blazer you can find it on the curb.

Here are five things to know:

Green screen: Equity investors are willing to believe in the AI trade again ahead of Nvidia’s results today after the bell. Tech stocks rebounded yesterday with shares of Thomson Reuters surging 11% after being mentioned at an Anthropic event. Thomson Reuters has been roadkill along with the broader software sector on fears that AI will eat their lunch. But the event yesterday highlighted that TRI’s AI legal software platform (CoCounsel) already has 1 million users. We also have an analyst upgrading Oracle this morning, which is the poster child for a levered bet on AI. Shares of Oracle have been cut in half since September and Oppenheimer’s Brian Schwartz says that’s enough. While acknowledging the upgrade may be early, Schwartz argues the company can still compound earnings and that it is broadly underowned. Today we have earnings to contend with. Lowe’s is trading lower after its margin forecast was slightly weaker than expected. There are 14 TSX companies reporting today including BMO, National and Loblaw (more below) and EQB after the bell.

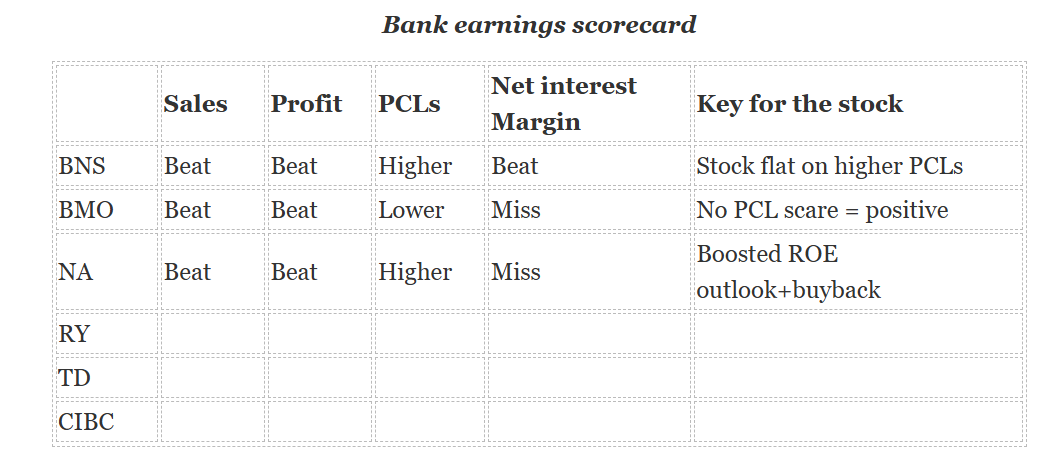

Marching to the beat: Bank of Montreal reported a clean quarter with a beat on most important metrics: profit, sales, provisions for credit losses were all better than expected. Net interest margins were slightly lower, but analysts don’t seem fussed. “PCLs were much better than expected – mostly commercial, otherwise no surprises on impaired PCLs,” wrote TD’s Mario Mendonca, “We view the quarter positively.” A few years ago BMO had some credit quality issues dating back to loans made during the pandemic, so the fact that provisions for credit losses didn’t contain any negative surprises means more for this bank. While all-bank margins were slightly lower than expected, they expanded in the Canadian and US business. Return on equity expanded to 12.4% which is also being viewed as a positive.

Core: National Bank also beat expectations in what looked like a pristine quarter: sales, profit, and Canadian banking were all higher than expected. It also increased its forecast for return on equity to 16% from 15% with plans to achieve 17% by 2027. There was also a significant increase to its share buyback program authorizing the purchase of 14.5 million shares (3.7% of the float) compared to its last buyback of 8 million shares. Much of the strength came from its Canadian banking division (hat tip to its Canadian Western Bank acquisition) and RBC says the capital markets business was actually slightly lower than their expectation. “Overall, we have a positive view of Q1/26 results as core EPS was above our estimate and consensus mainly due to stronger than expected Personal and Commercial (a good source of earnings strength) and Corporate results, partially offset by lower than anticipated Capital Markets core earnings,” wrote Darko Mihelic of RBC.

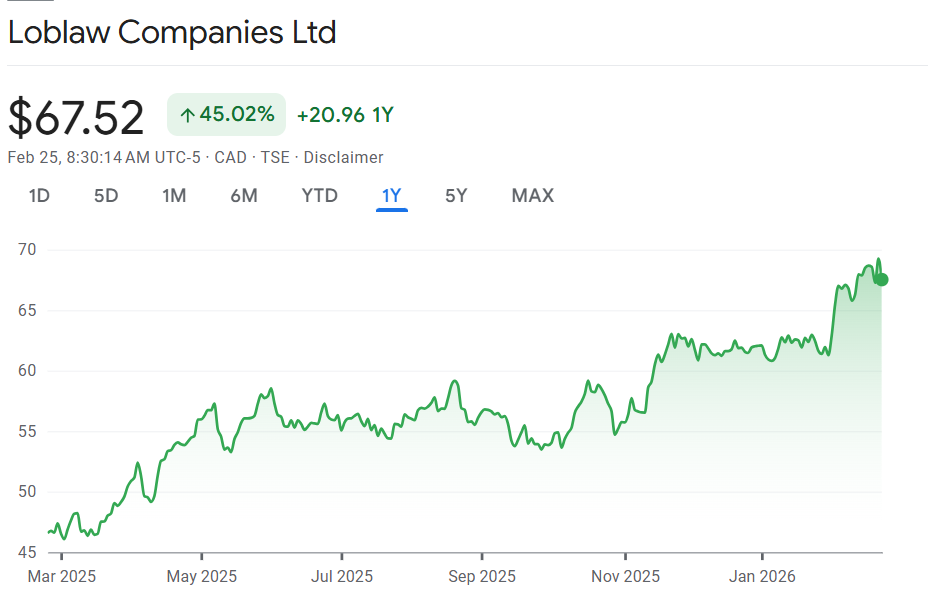

Price check: Watch Loblaw at the open after sales growth disappointed in both food and drug departments. Profit came in slightly ahead. Food same-store sales growth was 1.5% vs consensus at 1.9% and food inflation at 4.4%. The growth marks a deceleration in growth from previous quarters. Drug sales grew 3.9% but this was below the 4.3% expected. Still, profit was a penny above expectations. RBC’s Irene Nattel says it was a solid end to 2025 and says the 2026 outlook points to more of the same.

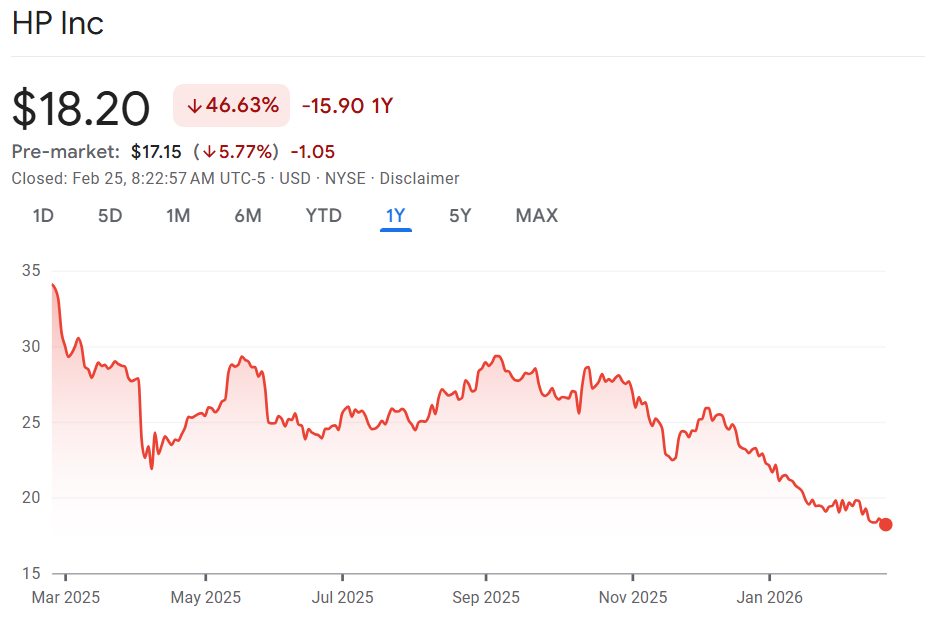

Memory problems: Shares of HP Inc are falling 5% after warning that high memory chip prices will weigh on profit. The PC and printer maker said profit for the year will likely be at the lower end of their target due to skyrocketing memory chip prices as well as things like tariffs. There are signs this is already eating in to the business. Margins this quarter came in below expectations. Memory prices have doubled for the company over the last year and the CFO warned that prices will likely continue to increase this year. The stock is poised to open at a more than 5-year low.

Don’t miss our next episode!

![]()