For a look at the week ahead, don’t miss my weekly column in the Globe & Mail. September is bucking its seasonally weak reputation, Micron reports, and much more.

Diverge: US futures are under pressure as changes to the H1-B visa program weigh on tech stocks. The TSX, meanwhile, could get a lift from gold surging to a fresh record above $3,700/oz. US President Donald Trump announced that the popular H1-B visa program used by US companies to hire foreign employees would now come with a hefty price tag of $100,000 per application. It is especially popular with tech firms that use it to hire software engineers. The pressure in tech stocks is pretty modest right now and perhaps more of an excuse to sell as Rosh Hashanah begins (the old adage “sell Rosh Hashanah, buy Yom Kippur refers to average decline in the S&P 500 of 0.4% during 9 days between the two holidays). With the Federal Reserve rate cut behind us, the market will have to endure 18 Fed speeches this week.

Drug deal: Pfizer is buying Metsera in a $4.9 billion deal at a 43% premium for the obesity drug startup which just went public at the beginning of the year. It’s no secret that Pfizer has be floundering after Covid (mainly because as a shareholder I keep talking about it). Attempts to hop on the obesity drug bandwagon have flopped so far. Metsera is far from a sure bet, it is working on experimental weight-loss drugs and most are years away from approval. Still, shares of Pfizer are higher in the pre-market signaling how desperate investors are for any signs the company is getting its foot in the door.

Shoot first: Shares of Tylenol maker Kenvue are falling 4% in the pre-market as reports suggests the Trump administration is poised to announced the drug’s active ingredient is linked to autism. Officials plan to warn pregnant women against using drugs with acetaminophen (the key ingredient in Tylenol). “The facts are that over a decade of rigorous research, endorsed by leading medical professionals and global health regulators, confirms there is no credible evidence linking acetaminophen to autism,” according to a statement by Kenvue. Aside from the science of it all, this could re-open litigation against makers of acetomenophin after cases in 2023 were largely dismissed because lack of credible scientific evidence. This comes at a time when Kenvue is struggling. It’s in the middle of a CEO search and a strategic review. At the last earnings report cut their sales growth forecast for 2025.

That’s gold, Jerry: Shares of Barrick Mining are popping nearly 3% in the pre-market and poised to open at the highest level since January 2013 on several catalysts. First, gold is surging right now. Second, the company just did a mining tour at its Nevada Gold Mines complex (the largest gold mining complex in the world) and analysts are coming away very positive. National Bank’s Shane Nagle is upgrading the stock to outperform following the tour. “The tour highlighted recent and ongoing processing improvements within the complex,” said Nagle in the reason for the upgrade. Analysts are particularly excited about the Fourmile project, which is 100% owned by Barrick. “Fourmile is shaping up to be among the highest-grade discoveries in the world,” wrote TD’s Steven Green who already has a buy rating on the stock.

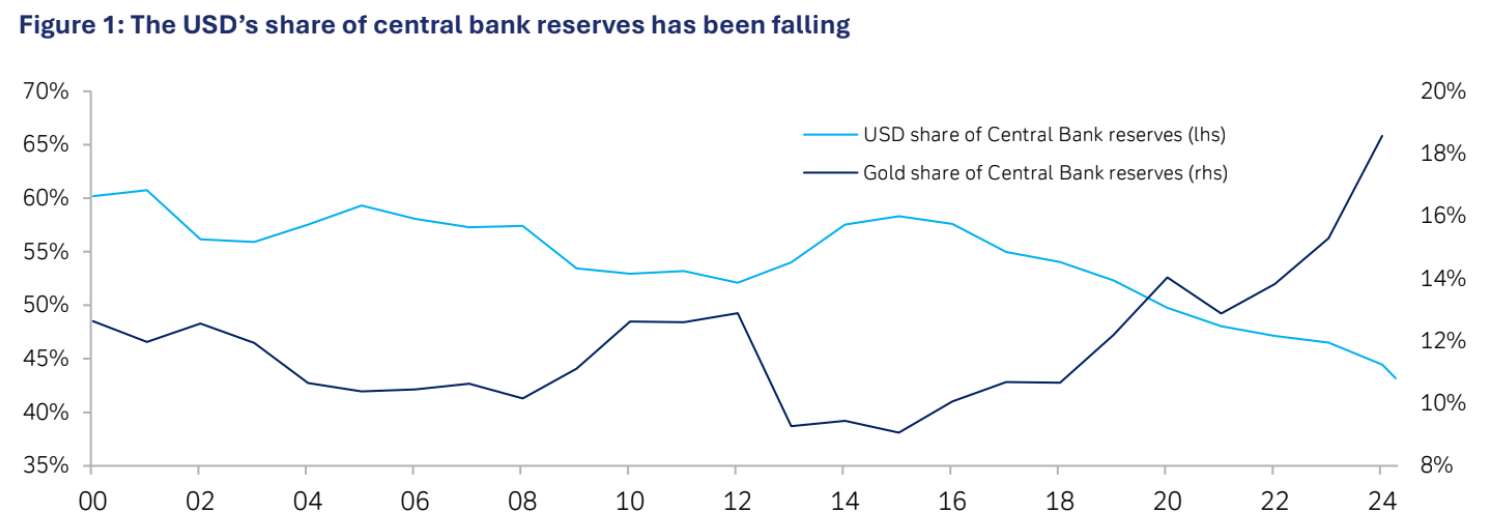

Old vs new: Gold is rocketing to a new all-time high while crypto is in the the throes of a sell-off right now. There is no particular reason for the crypto sell-off (Bitcoin -2.5%, Ether -6.5%, Ripple -5.7%). Some are chalking it up to an unwind of leveraged positioned after the Fed rate decision. Deutsche Bank is out with an interesting report on whether Bitcoin could ever find a place in central bank reserves in the next 5 years. They conclude that there is room for both gold and Bitcoin to coexist in central bank balance sheets by 2030. Their argument is that Bitcoin volatility will calm down and present as a viable reserve asset. The backdrop is that US dollars as a share of bank reserves are falling. Some food for thought!

Don’t miss our next episode!

![]()