For years, U.S. markets felt unstoppable. Now the script is flipping. On this episode of In the Money with Amber Kanwar, Matthew Strauss, SVP, Portfolio Manager & Lead – Global Equities at CI Global Asset Management, makes the case for rotating into global and emerging market equities. After years of American dominance, Matthew argues that stretched U.S. valuations, crowded positioning, and a shifting growth differential are finally pushing investors to look abroad.

I was in the middle of a board meeting when someone banged the table and slammed their laptop shut. It was then we all new the hard truth: the US scored, Canada lost.

Here are five things to know today:

Hodge podge: Futures moved lower after a set of disappointing data out of the US. American GDP came in below expectations while a key gauge of inflation came in higher than expected (cue: stagflation fears). Let’s unpack before we lose our minds. US GDP expanded 1.4% in the fourth quarter, significantly below the 2.8% expected and the 4.4% in the third quarter. “But the headline figure has been noisy due to shifts in trade and inventories, and this time around the government shutdown added to that noise, delivering an outsized negative impact this quarter but that will reverse and then flatter growth in 26Q1,” wrote CIBC’s Ali Jaffery. At the same time we got a read of the Fed’s preferred gauge of inflation which advanced more than expected on both headline and core basis. “This report is likely what the Fed expected and won’t move the needle in discussions on where rates need to go. Future inflation and job reports will continue to be the main guidepost for the Fed. We expect two cuts in the second half of the year,” wrote Jaffery. Oil prices are holding onto gains as the US increases its presence in the Middle East warning there could be a strike in 10-15 days if Iran doesn’t reach a nuclear deal. This morning there could be an important Supreme Court ruling about whether US President Donald Trump’s tariffs are legal. The proceedings start at 10am. BMO notes potential refunds to businesses could exceed $175 billion, according to Penn-Wharton Budget Model. In Canada, we got a read of retail sales were slightly better than feared falling only 0.4% in December after a 1.2% surge in November.

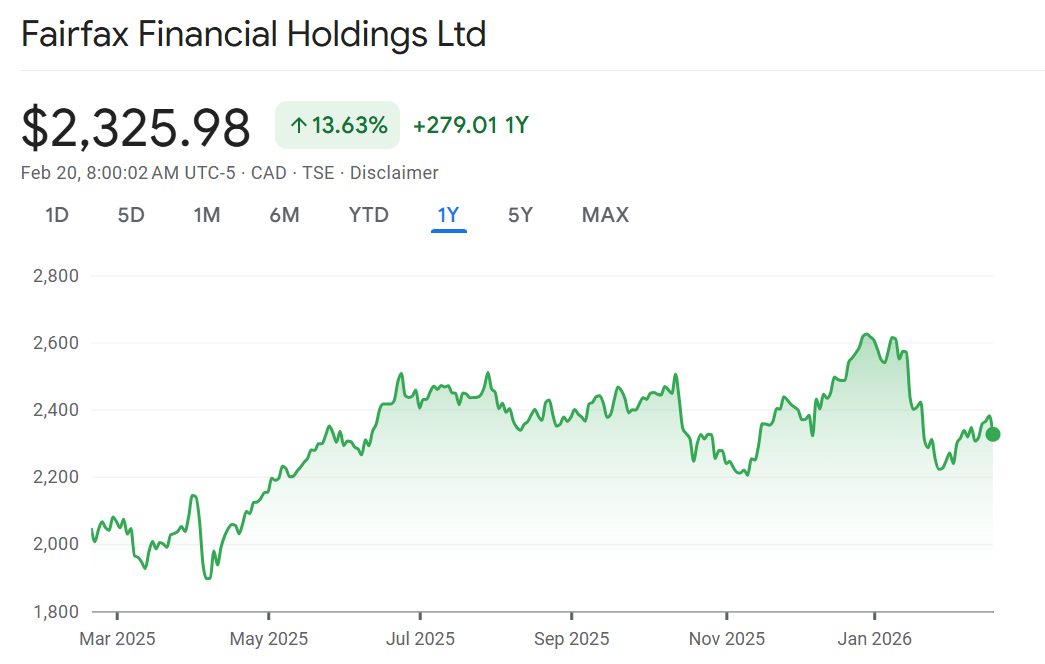

Canada’s Buffett: Watch shares of Fairfax Financial after its profit topped expectations. Favourable reserve releases and higher investment gains powered the quarter. Book value was aided by its stake in Eurobank in Greece which is up 67% over the past year. Shares are off 11% from the record high in December. RBC says they expect a neutral reaction to the earnings. Listening to the conference call now and they are talking up some of their investments including a recent position in Under Armour which has been underperforming. They say they like the setup and as long term investors they are optimistic that the founder-led company can turn it around. Q&A is just beginning as I write.

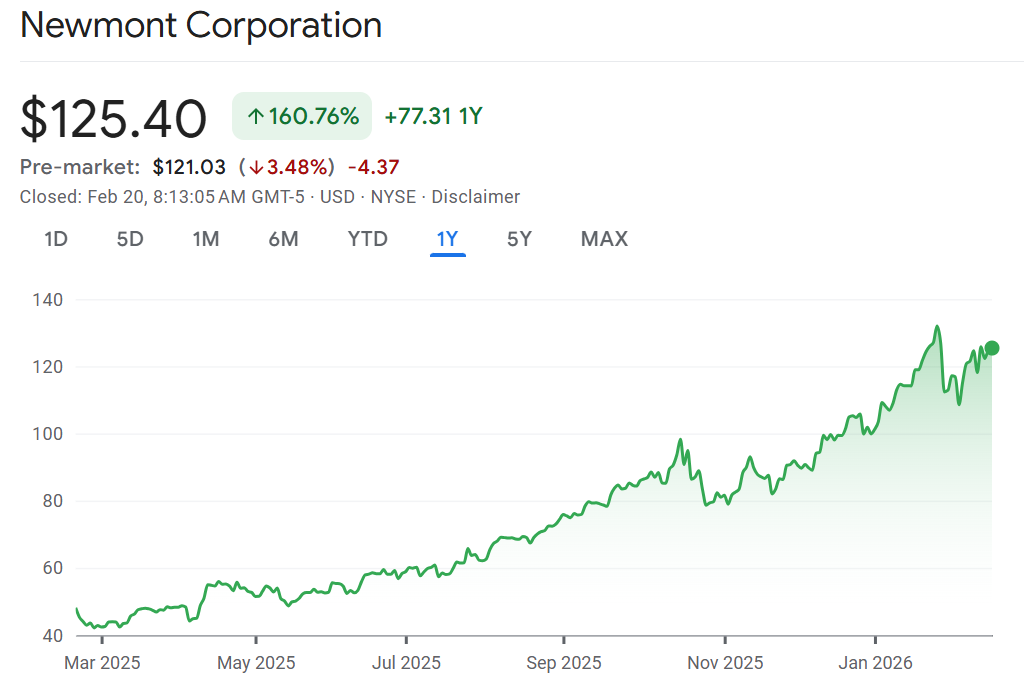

Gold digging: Newmont is falling 3% in the pre-market after warning that 2026 gold output would fall. This is overshadowing strong quarterly results that were better than expected and record quarterly profits. The weaker output in 2026 is attributed in part because of lower expectations out of two gold mines which are jointly owned by Barrick. Barrick is hoping to spin their ownership out into an IPO, but Newmont wants them to improve output first revealing in the quarter they sent a letter saying they have “identified evidence of mismanagement.” This will likely come down to a monetary payment, says TD’s Steven Green “which is unlikely to have any material impact on either company.” Eldorado Gold is falling 5% in the pre-market after warning production will be lower due to the delay of a key mine starting up. Eldorado said their Skouries mine in Greece, which is a key cornerstone of growth, won’t start production until the third quarter of this year vs previous expectation it would be up and running this quarter. This represents about a 15% decrease in their production forecast. CIBC and Canaccord have both downgraded the stock on the back of the announcement.

Hoot hoot: The private credit market has been roiled by asset manager Blue Owl which has been hit with redemptions in its private credit funds. The redemptions forced the company to sell loans related to three of its business development companies and restrict redemptions in other funds. The catalyst has been anxieties that AI is going to disrupt software businesses in the private market – much like we have seen in the public markets. This is coming at a time when retail investors are being given greater access to the private markets and raising questions about the suitability for investors. It’s not that these assets are in current distress, but the fear of distress means investors want their money back. It is similar to what we have been seeing with real estate funds in Canada. The woes are weighing on asset managers across the board. “Against an already fragile macro backdrop, Alt Manager stocks took another leg down on 2/19 following loan sales by OWL that seemingly touched off a firestorm on whether the wealth management democratization cycle is kaput,” wrote TD’s Bill Katz, “…we do not believe the (long-term) opportunity to further penetrate global wealth is kaput…we believe the seeds are being planted for a wider ranging M&A/alliances across Asset Managers, as the drive for public/private capabilities at scale is becoming increasingly paramount…)

Door number 1: Shares of meme stock Opendoor are surging 18% in the pre-market on signs a turnaround is taking place. The US-based online seller and buyer of residential property has caught the imagination of retail investors for its revival prospects following a dismal US housing market. Canadian activist investor Eric Jackson (who has been on the podcast twice) has been leading the charge and helped create conditions for Canadian Kaz Nejatian (formerly of Shopify) to become CEO. Sales fell 32% in the quarter, but this was much better than feared. The number of homes sold also fell 30% but again, better than feared. The outlook suggests next quarter sales will only fall 10%. “(Opendoor) is driving operational transformation and setting the stage for sustainable growth even in a depressed housing market,” wrote Dae Lee of JPMorgan who has the only buy on the stock and a $8/share price target. It’s a blow to the shorts with nearly 15% of the shares outstanding short.

Don’t miss our next episode! Email questions@inthemoneypod.com

![]()