On this episode of In the Money with Amber Kanwar, Amber sits down with Hussein Allidina, Head of Commodities at TD Asset Management, for one of the most comprehensive conversation about commodities after an explosive year. Hussein argues that we’re still in the early stages of a multi-year commodity upcycle, driven by chronic underinvestment, rising global demand, and a world that needs far more energy, metals and power infrastructure than we’re currently capable of producing. He explains why commodities zig when everything else zags, how they deliver real inflation protection, and why a 5–10% allocation may be the most overlooked tool in modern portfolio construction. Listen now on Apple, Spotify or YouTube!

This month I am partnering with Questrade—they’re building out some very cool investor tools and have a great promo on right now for our listeners. They’ve rolled out real game-changers: they’ve completely redesigned Questrade Pro, which is in beta testing now; you can trade directly from best-in-class charts with lightning-fast execution, AI tools, a full trader performance dashboard, and more—best part, it’s all free. And starting this December, you can trade assets like real physical gold right inside your account with Quest Metals, just like a stock. For listeners of the podcast, you can use promocode INTHEMONEY (all one word) when you sign up for your first self-directed account and get a $50 cash reward, or open a Questwealth Portfolios account and you’ll get your first $10,000 managed for free for one year. Visit Questrade.com, promocode INTHEMONEY.

Someone was asking me if my third child was self-sufficient because he learned from his two older sisters. Of course I said “Oh yes, my special boy is so advanced. He will come home from school and go straight to the sink to wash his hands all by himself. ” I left out the part where he commanded “Lights ON!” as though he had a voice controlled “clap on, clap off” light system. The worst part is that it worked, naturally I came rushing over to his aid!

Here are five things to know:

On to the next: Futures are giving back some of the rally yesterday after the Federal Reserve delivered its third rate cut in a row. For the first time in six years, there were three members who dissented the decision: two who favoured a hold and one who favoured a bigger cut. Fed Chair Jerome Powell signaled that the job picture is likely worse than the headline suggests which left traders comfortable with bets on two more rate cuts in 2026. Interestingly, the forecasted projection for rates by Fed members suggested only one more rate cut in 2026 (supporting that hawkish cut). The Fed is less relevant this morning than Oracle which reported results and is weighing on sentiment (more on that below). Oil continues to sink despite tensions between Venezuela and the US. On the podcast, Hussein explained why geopolitics don’t really matter for crude and why he sees crude falling to low 50s/high 40s per barrel near term (setting the stage for a rally in the next 6-12 months). Silver continues to be powered by rocket fuel this morning, Hussein also addresses why he won’t go all-in on the trade.

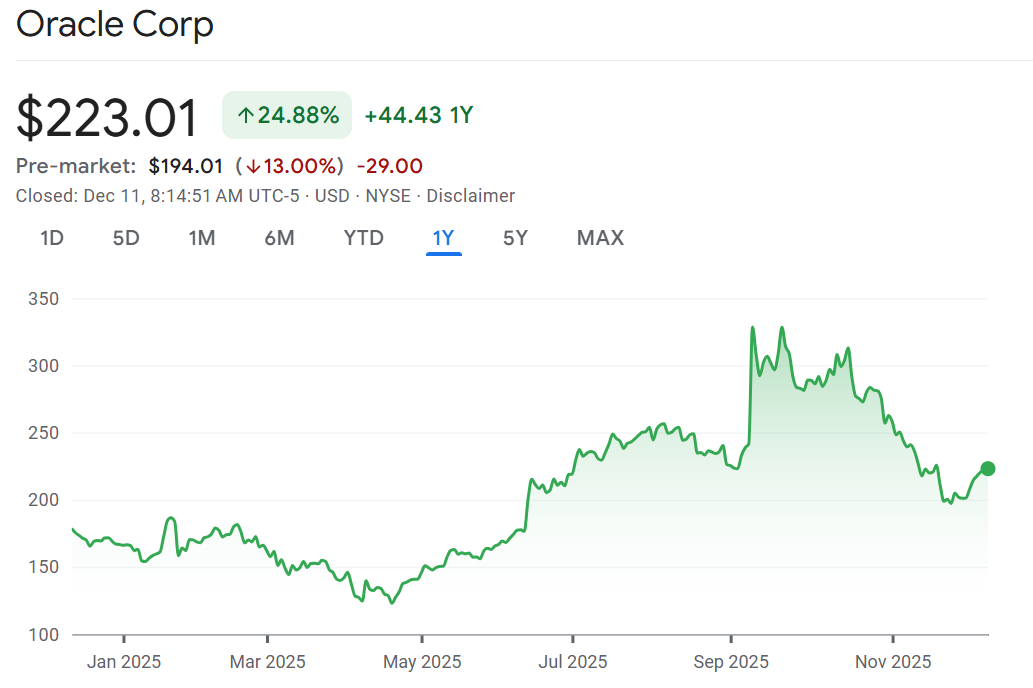

Prophetic: Oracle is sinking 13% in the pre-market weighing heavy on the overall AI trade this morning. To be clear, Oracle’s AI business is exploding but anxieties over debt, cash burn and heavy spending are making investors nervous. This quarter Oracle beat profit expectations, but cloud sales failed to live up to the hype (cloud sales up 34% fell just short of expectations). You could say that is the market being overly nitpicky. Indeed, the value of its total contracts have surged 5x to an eyewatering $523 billion which was way more than the street was expecting. But the concern is over the heavy spending needed to get that business. It plans to spend $50 billion next year, a$15 billion increase from its spending projection just a few months ago. In two years, Oracle has gone from a company that was generating $12 billion in free cash flow to one that is projected to burn $16 billion in 2026 and $22 billion in 2027. Not to mention the mountain of debt ($105 billion) and the cost to insure against a default soaring to the highest level since 2009. Enter Dan Ives, the uber AI bull who says all that matters is that their backlog is ballooning. “Oracle will likely need to raise less than the $100 billion in debt to service the Capex needed…and could be significantly under this number when all is said it done in our view,” he wrote in a note to clients. Nvidia is catching heat from the Oracle quarter because Oracle opened the door to using more non-Nvidia chips to “be prepared and able to deploy whatever chips our customers want to buy.”

Phone lines are lighting up: BCE is getting upgraded to buy for a second time this week. Following CIBC’s upgrade on Monday, BMO is upgrading the stock to outperform on a better risk/reward profile. Analyst Tim Casey says growth will hover around 2% which is hardly shooting the lights out but is better than outright declines. The dividend cut earlier this year now means the balance sheet has been “derisked” and the payout ratio is “reasonable.” Casey argues BCE has levers to pull to bring their leverage down even further, including potentially monetizing their 20% stake in the Montreal Canadiens (which he values at just under $1 billion). Valuation is also compelling with the stock trading well below its 5-year earnings multiple. Price target is $37/share implying 21% return from here.

Nothing to see here: Apropos of nothing, Tamarack Valley announced the adoption of a plan typically used to fend off hostile takeovers. Tamarack said this is not in response to any specific proposal or intention to control Tamarack. Shareholder rights plans, also known as poison pills, are a tool used by companies to fend off takeovers or activist investors. It allows existing shareholders to buy more shares at a steep discount to keep out outside shareholders. ” In the event of an unsolicited takeover bid in the future, the purpose of the Shareholder Rights Plan is to provide the Board and shareholders of Tamarack with an adequate amount of time to evaluate such unsolicited offer, explore value-enhancing alternatives, encourage potential bidders to treat Tamarack shareholders fairly and provide full and fair value for the Tamarack shares,” said the release. Put this in the “where there is smoke, there is fire” category. Tamarack Valley operates in the Clearwater basin in northern Alberta. Recall, David Szybunka of Canoe Financial called it “the best oil play I’ve ever seen in my career,” on the podcast in November. Shareholders will vote on the plan on May 6.

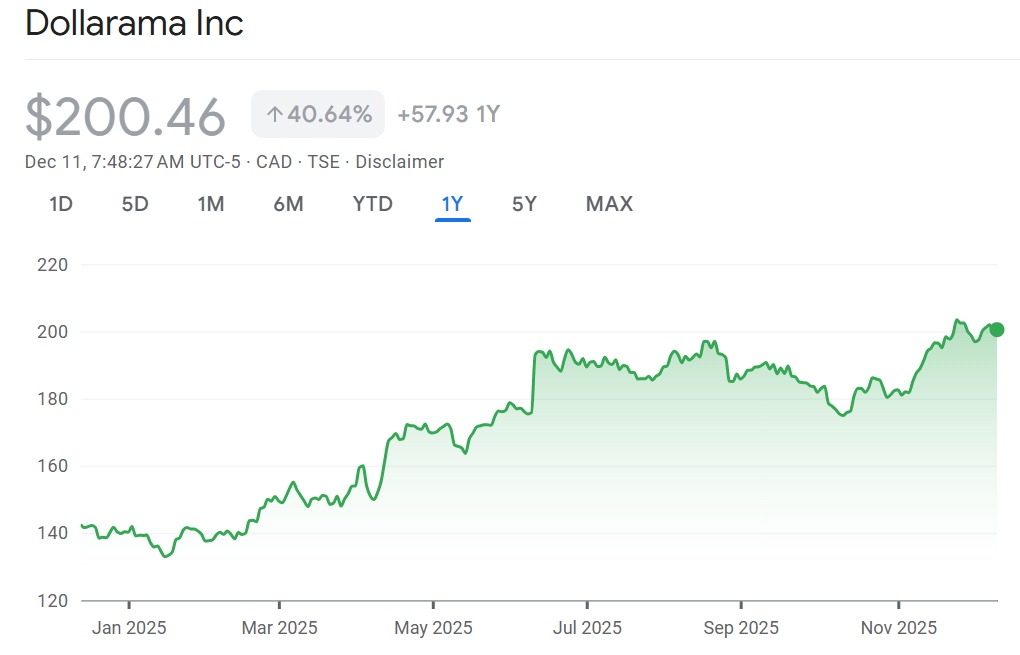

Printing dollars: Watch Dollarama at the open after it beat sales and profit expectations and boosted its outlook for 2026. A hat trick. Same store sales grew 6% compared to consensus estimates for 4.8%. Margins were also higher than expected. Pretty much a perfect quarter.

Don’t miss our next episode! Send us your tech questions questions@inthemoneypod.com