The best opportunities in the market might be the ones no one is paying attention to — and that’s exactly where microcap investor Mathieu Martin is looking. On this episode of In the Money with Amber Kanwar, Amber sits down with Mathieu Martin, Portfolio Manager for the Rivemont MicroCap Fund, to break down one of the most underfollowed — and potentially most lucrative — corners of the market.

Pro Picks is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

3 Microcaps Flying Under the Radar:

D-BOX specializes in motion seats for theaters (e.g., Cineplex customers), with hardware sales plus high-margin royalties from $8 ticket upcharges. After years of unprofitability, an activist investor cleaned up operations.

- Activist-led turnaround delivering profitability: New management refocused on core cinema competency, shedding distractions like gaming/home theater, achieving profitability after ~18 years of losses.

- Recurring high-margin revenue: Hardware covers operating expenses; royalty stream (nearly 100% gross margin) flows straight to the bottom line and surges with blockbusters/action films—revenue already above pre-COVID levels.

- Leverage to theater rebound: As big releases return, more D-BOX ticket purchases drive royalty growth, offering a unique way to play cinema recovery without owning exhibitors directly.

2. Cannara Biotech (LOVE.TO) – Quebec Cannabis Leader Expanding Nationally

Vertically integrated licensed producer that capitalized on industry distress to acquire premium assets cheaply and dominate its home market.

- Unfair cost and asset advantages: Bought a $250M facility for $27M (10 cents on the dollar), ramped it to $100M+ revenue in 3-4 years; low Quebec electricity costs provide major cultivation edge.

- Dominant local market share with proven model: #1 in Quebec (via SQDC preference for locals) achieved purely on quality/price—no marketing allowed—now replicating success in other provinces.

- Profitable micro-cap growth: Strong profitability (unlike many larger peers still struggling) at attractive valuations, with founder-led execution and national expansion runway.

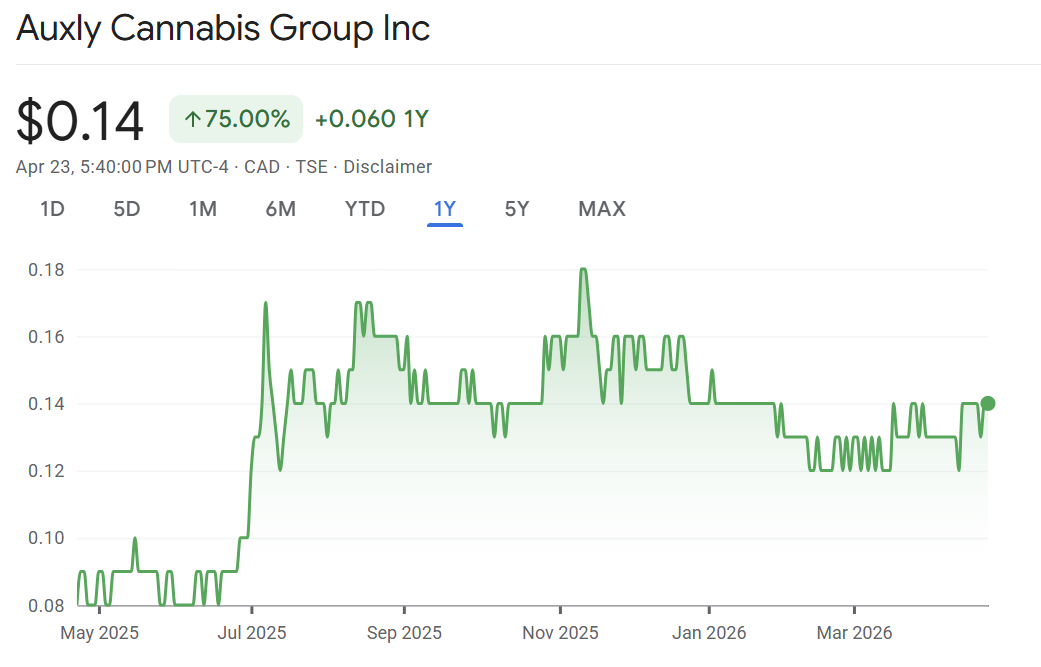

3. Auxly Cannabis Group (XLY.TO) – National Brand Leader with Cleaned-Up Balance Sheet

Larger-scale licensed producer (#3 market share) behind the top brand Back 40, focused on innovation and international exports.

- Best-in-class operations and margins: Lowest-cost producer in Canada, profitable with growing sales and strong margins; #1 national brand with real consumer affinity (e.g., significant merch sales).

- Balance sheet restructuring complete: Survived near-bankruptcy through debt conversion/restructuring; now positioned for growth as industry shakeout (70+ bankruptcies) reduces competition.

- Pricing power and export tailwinds: International medical demand (Germany, Australia, UK) absorbing supply, enabling retail price increases and more rational competition—Canada’s world-class production standard supports further upside.

Don’t miss our next episode! Submit questions to questions@inthemoneypod.com

![]()

DISCLAIMERS: This text AI generated and should be checked against actual delivery. The content provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.