This segment is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

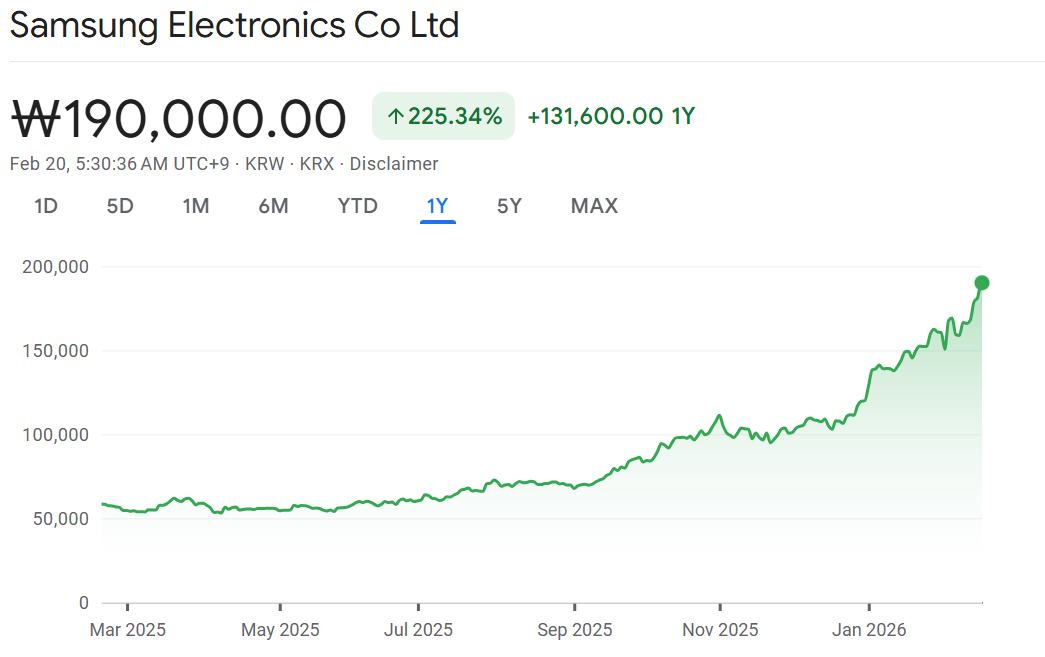

Samsung is a big winner from the AI boom, thanks to its role in supplying special high-speed memory chips needed for AI computers.

- Samsung got off to a slow start in this advanced memory race but caught up fast—it now produces and ships the newest version (called HBM4) ahead of schedule, putting real pressure on competitors like SK Hynix.

- These super-fast memory chips (think of them as the “high-speed highways” that let AI chips handle massive amounts of data quickly and efficiently) are in huge demand for AI, and Samsung benefits from its huge scale while the stock still looks reasonably priced (trading at low earnings multiples compared to other AI winners).

- Looking at Samsung’s different businesses (chips, phones, TVs) piece by piece shows the stock could be worth a lot more—the market is applying a discount because it’s a big, mixed company, but that could change as the AI memory strength shines through.

- Upside: 20-30% quite doable based on breaking down the value of its parts and strong execution in the memory area.

Alibaba is shifting from a mostly online shopping company to a major player in China’s fast-growing AI and cloud computing space.

- Alibaba offers a complete set of cloud services for AI (like the full infrastructure companies need to build and run AI tools), and it leads the market in China with little real competition right now—Tencent has fallen behind here.

- The cloud and AI part is growing quickly and should become the main driver, making Alibaba more like Amazon (strong in both shopping and cloud) instead of just an e-commerce giant with a small cloud side.

- Earlier worries about government regulations (like crackdowns on big tech) have eased—companies have adapted to work within the rules, reducing that risk.

- Upside: Eventually can go back to (or exceed) its pandemic-era highs as cloud/AI becomes the biggest growth engine.

Vista Energy (VIST)

Vista is an oil and gas company focused on a huge shale area in Argentina (Vaca Muerta), seen as a special opportunity with good execution in a improving environment.

- New drilling techniques have unlocked massive oil reserves there, allowing Vista to produce efficiently—its early wells are already more productive than similar ones in the U.S.

- Recent political and economic changes in Argentina are helping create more stability, and Vista grows smartly: it picks high-quality wells and acquisitions without overpaying or rushing.

- Big advantages include exporting most of its oil at world prices (not cheaper local ones), low costs, high efficiency, and a solid balance sheet with low debt and plans to fund growth from its own cash flow.

Don’t miss our next episode! Email your ESG questions to questions@inthemoneypod.com

![]()

DISCLAIMERS: This text AI generated and should be checked against actual delivery. The content provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.