What happens when politics collides head-on with monetary policy? On this episode of In the Money with Amber Kanwar, Amber sits down with legendary Fed watcher Ed Yardeni, President of Yardeni Research, to unpack what he calls an unprecedented threat to the independence of the U.S. Federal Reserve — and why the market may be more resilient than the headlines suggest.

So one of the downsides of living in the city with kids is that signing up for summer camps means you need to map out your entire summer by January. Normally I am panic texting my husband figuring out our plans 20 minutes before sign-up which leads to inevitably emailing administrators begging to make space because I missed the sign-up deadline. But not this year. This year I am *that* mom. I have mapped out the entire summer. Naturally, we got an email saying the camp is having some sort of website glitch and sign-ups wont be today but they promise to give us 48 hours notice. Cool cool cool. I’ll just wait. Not like it was incredibly inconvenient to race to plan the lives of three humans, week-by-week, 6 months in advance. On the bright side, it gives me time to make a doctors appointment to find out why my eye keeps twitching.

Here are five things to know:

Dogs breakfast: US futures are under pressure following a down day yesterday as metals rip higher and crypto prices break out. There is a dogs breakfast of catalysts to consider. Iran continues to worsen with the US promising to support through military action. Oil prices are rising for a fifth session in a row and hitting a 3-month high. Meanwhile, gold (+1%), silver (+4.5%), even tin prices (+3%) are hitting records. Higher oil and material prices should support Canadian markets today. Tech has underperformed to start 2026 and that has held back performance of US stocks compared to the TSX. Although on the podcast, Ed Yardeni says the S&P 500 can hit 7,700 on a broadening out of the rally. Aside from that, I wonder about nearly every metal hitting new highs and how that will show up in inflation at some point. Speaking of which, we got a read of producer prices which unexpectedly picked up in November thanks to higher energy costs. Retail sales also came out this morning beating expectations confirming bank CEO commentary that the consumer remains resilient. Aside from that we’ve also got Prime Minister Mark Carney landing in China just as US President Donald Trump called a trade agreement with Canada “irrelevant.” JD Vance and Marco Rubio are meeting with foreign ministers of Greenland and Denmark. There is also a chance we will hear from the supreme court in the US today about the legality of Trump’s tariffs. Oh yes, and earnings. Below is a recap of bank earnings out today. The bottom line is that none of the results are shoot the lights out and financials are off to a rocky start in 2026 in the US, currently the worst performing sector on the S&P 500.

BAC to business: Bank of America is trading higher after profit beat expectations. Profit rose 12% on higher revenue from the consumer bank and solid results out of sales and trading. Echoing Jamie Dimon’s comments about the consumers, CEO Brian Moynihan also called consumer spending “resilient.” To wit, provisions for loans that could go bad fell and came in lower than expected. However, unlike JPMorgan which fell yesterday on disappointing investment banking revenue, Bank of America’s investment banking did slightly better than expectations. If there is a blemish it might be on the expense outlook, notes Keith Horowitz at Citi. “Expect key debate to focus on fee growth potential to offset expenses,” he said in a note to clients.

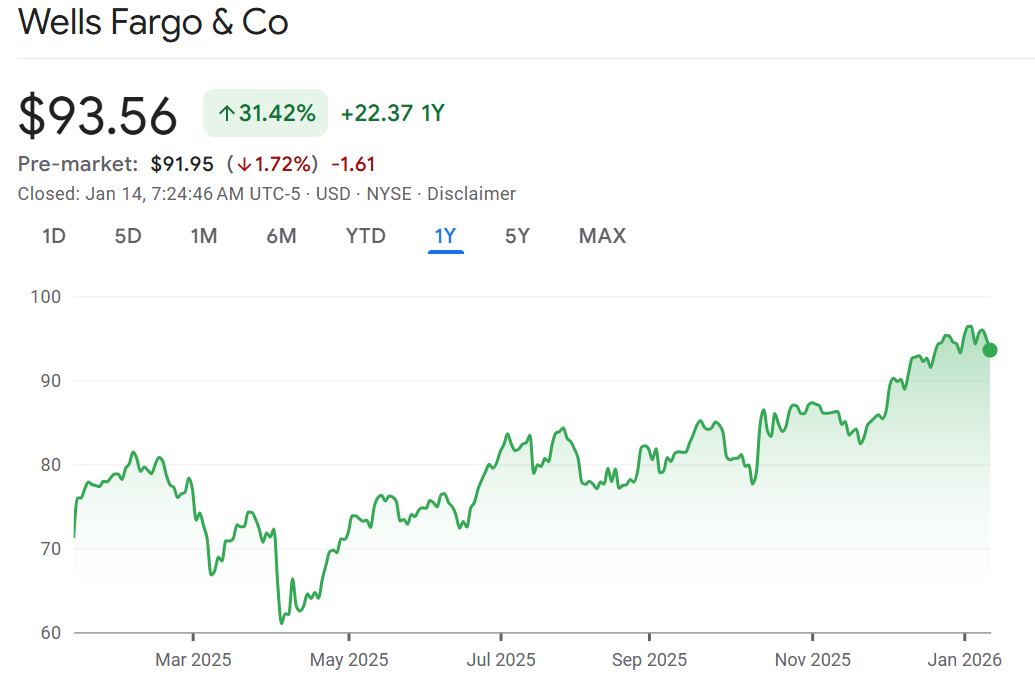

Swing and a miss: Wells Fargo is falling in the pre-market as a measure of bank profit was lower than expected and revenue missed expectations. Net interest income (profit they make on the spread between what they charge for loans and pay on deposits) came in lower as consumer lending and investment banking revenue missed the mark. The cost of severance also drove up expenses higher than expected as the company lowered headcount by over 5,000 jobs. Perhaps the greatest endorsement of the economic outlook is that provisions for losses that could go bad came in less than expected, similar to what we saw at Bank of America.

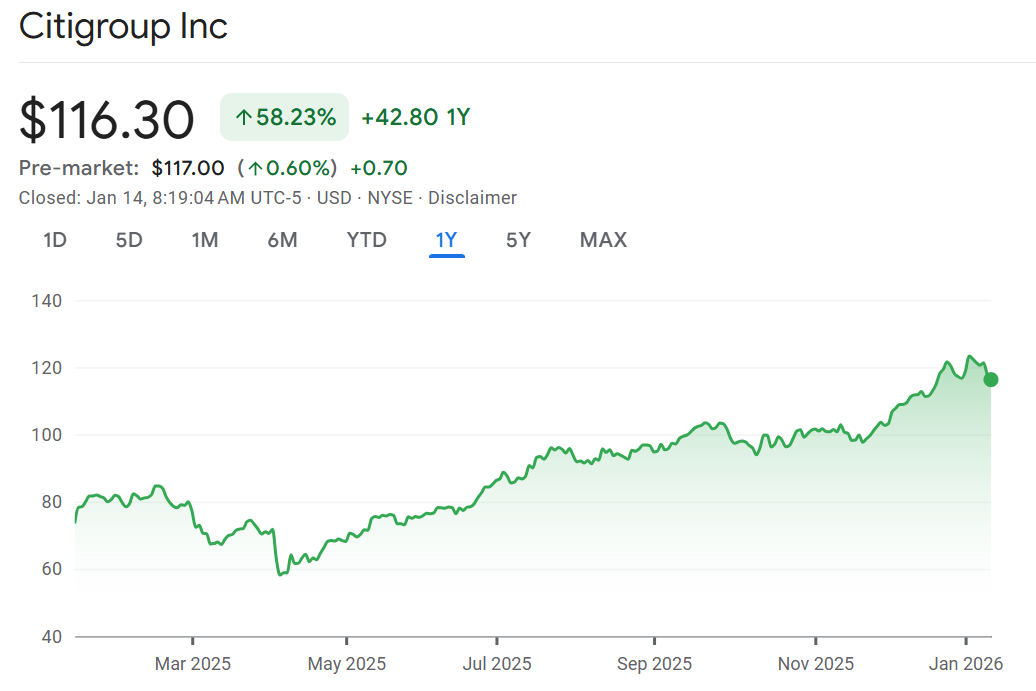

Paradise Citi: Shares of Citigroup are getting whipsawed this morning on a mixed quarter. On the plus side, profit was higher than expected lifted by better fixed income, currency and commodity trading and its banking business. On the negative side, total reveune was lower weighed down by weaker equity trading and slightly lower wealth revenue than expected. Its debt underwriting business was also weak.

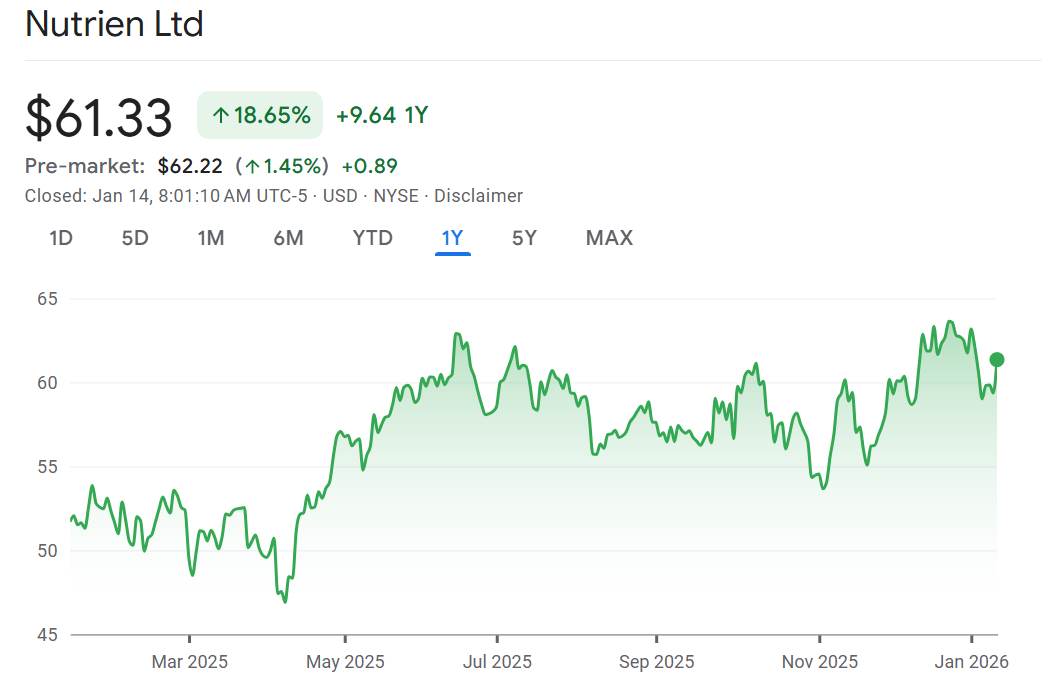

Notable calls: Nutrien is up 2% in the pre-market after Morgan Stanley upgraded the stock to overweight from equal weight. The analyst is more constructive on potash demand and prices. The price target of $77/share implies 25% upside from here. TD is shuffling its ratings on asset managers upgrading CME Group to Buy while downgrading KKR, Stifel Financial and Blackrock. CME Group has a favourable volume backdrop and leverage to retail investor opportunities says analyst Bill Katz. KKR and Stifel have the greatest risk into earnings says Katz while Blackrock is also at risk and has limited near-term catalysts. Insiders are selling shares of Aritzia according to a new filing. Chairman and founder Brian Hill is selling stock in a $200 million bought-deal offering. Hill says this is part of estate planning and chartable giving. With the stock doubling over the past year, better to give while the getting is good!

Don’t miss our next episode!

![]()