In a world crazy for AI stocks, who is interested in anything else? Rob Lauzon of Middlefield says major political change is afoot and it means big opportunity for investors. “I feel the most positive about our country, about our business climate…our natural resources than I have been in many years,” said Lauzon on a new episode of In the Money with Amber Kanwar.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information.

1. Canadian Apartment REIT (CAR.UN)

Why it’s compelling:

- Trading below $40 despite an estimated net asset value around $55, implying 25–30% upside once sentiment normalizes.

- Management has de-levered the balance sheet, sold off European assets, and has fresh cash — yet insiders haven’t bought recently, which Lauzon thinks could change.

- Lauzon believes “no one wants apartments right now,” but that’s exactly where deep value lives — and he expects either a strategic transaction or steady compounding as rent growth resumes.

Why it’s lagged:

- Oversupply fears in Canada’s condo market and lower immigration have dampened sentiment toward all residential REITs.

- Investors are conflating troubled condo developers with purpose-built rental REITs like CAR.UN, which have healthier fundamentals.

Upside catalyst:

- A rebound in immigration or management-led catalyst (buyback, partnership with pension fund) could re-rate shares 25–30% over the next 18–24 months

2. Tourmaline Oil (TOU)

Why it’s compelling:

- One of Canada’s strongest balance sheets, with 75 years of reserves and a six-year plan that could generate $13 billion in free cash flow — roughly half its current market cap.

- Lauzon says buy it and “put it in a drawer for six years,” offering 10% annual total returns through dividends and growth.

- Positioned to benefit from new LNG export capacity and data center–driven natural gas demand, both domestic and global.

Why it’s lagged:

- Investor frustration over large capital spending plans and fears that cash flow will be diverted from dividends toward development.

- Gas prices were hit by temporary infrastructure outages that trapped Alberta gas under $1 this summer.

Upside catalyst:

- As gas prices normalize toward $3–4 in Canada and $4–5 in the U.S., Lauzon sees TOU as a potential $100 stock vs. ~$60 today — more than 60% upside with a strong dividend kicker.

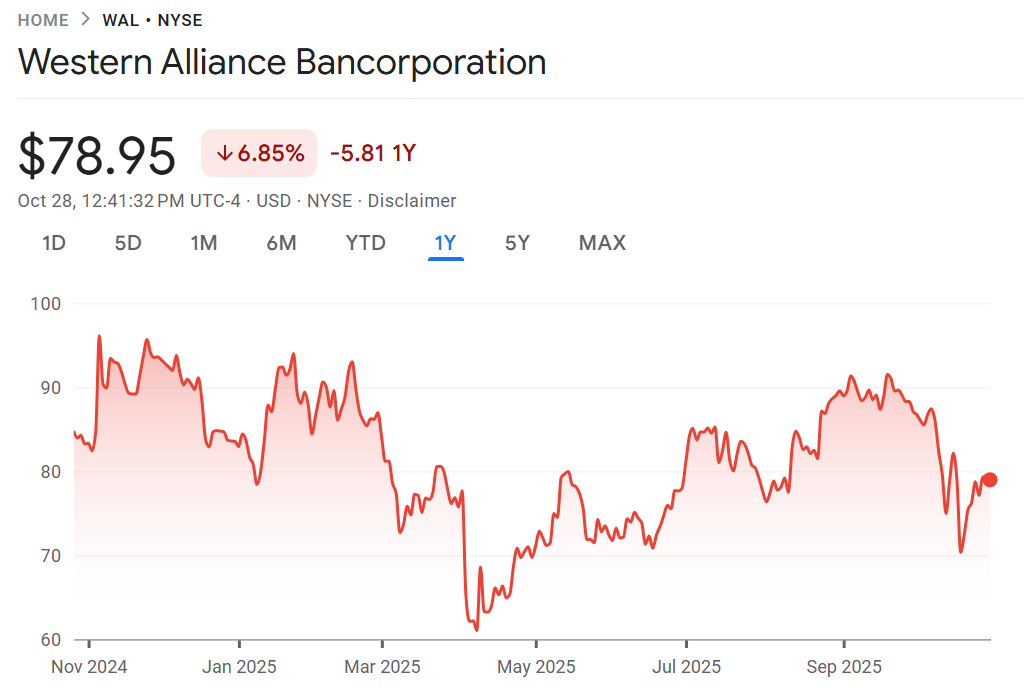

3. Western Alliance Bancorporation (WAL)

Why it’s compelling:

- A U.S. regional bank trading at just 8x earnings but growing EPS 20% annually, with strong credit history and expanding technology-led banking services.

- Recent lawsuit-related selloff was an overreaction: the issue represents ~$90 million in exposure, largely collateralized and already provisioned for.

- Management announced a $300 million buyback and expects margin expansion as interest rates fall and mortgage activity rebounds.

Why it’s lagged:

- Shares dropped ~16% after news of a potential fraud case involving collateralized loans; investors feared a repeat of the 2023 regional bank turmoil.

- Market concerns over the U.S. housing slowdown and inverted yield curve weighed on sentiment.

Upside catalyst:

- Lauzon expects Fed rate cuts and a housing recovery by 2026, reviving mortgage growth and boosting margins.

- He sees WAL at $100+ within two years (vs. ~$78 today) — a 30%+ upside with growing dividends.

DON’T MISS OUR NEXT EPISODE COMING TO YOU FROM VANCOUVER!

![]()