Futures shrug off inflation, tariff watch, Cisco pops, Deere drops, Sun Life & Canadian Tire miss

Last night at dinner time I realized I was behind on my homework – the kids needed to make Valentines for each of their 20+ classmates by today. So I braved the rush-hour traffic in a snowstorm to buy cards and spent a grueling hour before bedtime getting the kids to write out everyone’s name. Long story short, it’s a snow day today and I believe a direct result of those efforts.

A new episode of In the Money with Amber Kanwar is out now! I spoke with Ross Gerber of Gerber Kawasaki about all things tech. It’s the worst performing sector so far in 2025 in the US and while he still finds plenty of buying opportunities, he is getting selective and two of his best three ideas aren’t tech stocks. He also told me why he’s been selling Tesla. He’s as much a storyteller as he is a stock picker. Listen here on Apple, Spotify, or here.

Today’s newsletter is brought to you by BMO. We all want to make the most of our investments. That’s why BMO InvestorLine is here. Their easy-to-use platform, packed with tools, resources, and commission-free trading on over 100 popular ETFs, can help you trade with confidence and take control of your financial future.

Learn more here.

Hot to go: It may be cold outside but US inflation is coming in hot. Core producer prices increased more than expected (+3.6% vs +3.3% expected) while the prior month was revised higher. This comes after consumer inflation for January increased by the most since August 2023. No matter how you slice it, prices are moving back up in the US and this complicates that rate cut path for the Federal Reserve. Unlike yesterday, however, the reaction in the bond market is more muted, while futures are slightly higher. While broad markets shrug this report off, we are seeing gold advance to another fresh record with the yellow metal less than $100 away from $3,000/oz. This morning we are on high alert for retaliatory tariffs by Trump who said reciprocal tariffs were on the way in a post on Truth Social. Moments ago he said “Today is the big one” when it comes to tariffs. It is a busy day for earnings with 16 TSX companies reporting today and 29 reporting on the S&P 500.

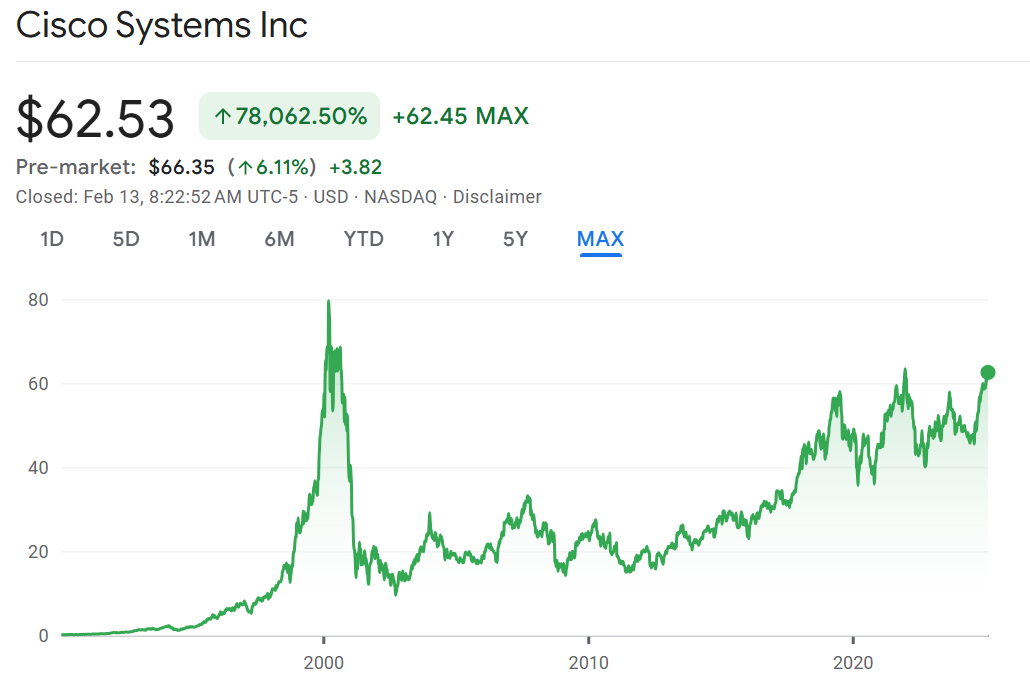

Gear heads: Cisco is rallying 6% in the pre-market after sales grew for the first time in five quarters and the company boosted it’s sales outlook for the year. The largest maker of networking gear posted 9% sales growth courtesy of its Splunk division which is acquired last year. Without Splunk, sales would have been down. Profit came in higher than expected. Cisco is benefitting from strong AI infrastructure demand and lifted its forecast for sales in 2025. The stock is poised to open at the highest level since 2000. While the average analyst price target suggests it is fully valued here ($68/share), Rosenblatt’s Michael Genovese is upgrading the stock and has an $80/share price target which suggests 21% upside. Cisco deserves a higher multiple because of growth in software subscriptions and AI becoming a larger driver of the total business, argues Genovese in his upgrade. It trades at an undemanding 17x forward earnings multiple.

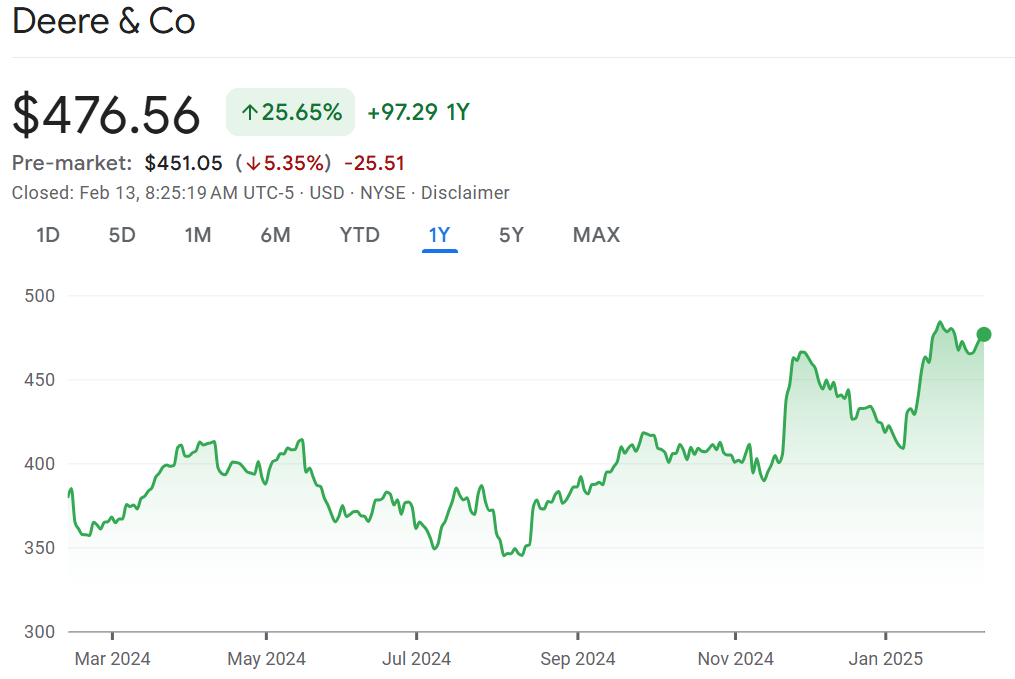

Oh Deere: Shares of Deere are dropping 5% in the early trade despite better than expected profits as challenged farm demand continues to weigh on sales. Total sales dropped nearly 30%, its steepest quarterly drop in sales on record. Lower crop prices have tempered demand from farmers for equipment. The company did maintain their full year profit forecast suggesting they don’t expect things to get worse, however the outlook does not include the potential impact from tariffs which would raise the cost of making their machines. Having said all that, the stock has been remarkably resilient. It has outperformed the S&P 500 over the past year and is up nearly 30%. It seems investors are taking comfort in the fact that the company reaffirmed its profit forecast and could be betting that this will be the bottom in earnings.

The sun will come out: Shares of Sun Life could come under pressure today. The insurer missed earnings expectations as it was hit by weakness in its US medical and dental insurance unit. Furthermore, outflows at MFS (its asset management division) were a record -$20 billion according to TD’s Mario Mendonca in a report titled “Not a lot to like about this quarter.” There were plenty of blemishes in this report, notes Mendonca, who says earnings quality was very week. On the flip side, Gabriel Dechaine of National Bank says this would be a buying opportunity. “Should there be a large pullback in SLF’s share price in reaction to these results…we would view it as a buying opportunity,” wrote Dechaine, “We note this quarter marks only the fifth large (i.e., 5%+) EPS miss over the past decade+.”

Pit stop: Canadian Tire may come under pressure this morning after earnings and sales came in below expectations. Same-store sales were weaker than expected across all its banners (SSS for Canadian Tire was +1.1% vs street 3.3%, SportChek +0.4% vs street +2.8% and Mark’s +1.8% vs street at +3.6%). “We expect results to be interpreted negatively by the Street,” wrote John Zamparo of Scotiabank.