Nvidia struggles, Manulife does it again, Bitcoin nears $100,000

My husband and I enjoyed our final night in New York last night. We ate at what is supposed to be a very exclusive club. We sampled from the glamourous life only to be back at the hotel by 9:30pm where we caught two reruns of The Office. Doesn’t get much better than that.

Lit: Futures are higher this morning as Nvidia attempts to go green post earnings and Snowflake soars 20% after results. In the Canadian markets I will watch the bank stocks after Barclays shuffled its ratings: downgrading National Bank to hold on valuation, downgrading TD to sell on anti-money laundering issues, upgrading RBC to buy on HSBC progress and moving Scotia to hold on transformation progress.

Green with Nvidia: The Latin translation of Invidia means “envy” and certainly there was lots to admire in the latest quarter. Nvidia shares are flat in the pre-market but don’t let that fool you, it was a stellar quarter. Sales grew 94% while EPS more than doubled at 103%. The outlook implies next quarter’s sales will grow more than 70% as CEO Jensen Huang calls demand for its new AI chips “staggering”. So why is the stock flat? A few reasons. 1) It is up 195% so far this year. 2) The outlook didn’t exceed the loftiest expectations. 3) The company warned about margin pressure as it works to have enough supply to meet demand. Worth noting that even with margins down to the 70s it is still nearly 20 percentage points higher than AMD and more than double Intel’s, according to Ipek Ozkardeskaya at Swissquote. The stock may be flat, but analysts are all generally positive. Bank of America said that results may have lacked the “sizzle” investors were hoping for, but the substance is still there. Price targets across the board are moving higher.

A different kind of sizzle: Manulife may not have the same pizazz as Nvidia, but the shares could trade even higher this morning. Last night Manulife announced it has entered into another agreement that would offload more of its long-term care exposure. It is a smaller deal than the last one. But remember, the market loves this for Manulife. It is up 61% since announcing its first reinsurance transaction nearly a year ago. “This follow-on transaction was well telegraphed,” wrote Meny Grauman at Scotia, “but there were still lingering doubts on Management’s ability to get it done.” While the stock may not move as dramatically as it did after December’s announcement, Grauman says it is still meaningful. “We think that it will still help drive Manulife’s valuation higher, and further validates our still bullish thesis on this name,” he wrote.

Back from the dead: Politico is reporting that one of Trump’s first announcements when he is in office will be to bring Keystone XL back from the dead. Trump first approved the Canada-to-Nebraska pipeline the last time he was President only to have it overturned by President Biden. Of course, this time is very different. For one thing, TC Energy has completely abandoned the initiative. If it were to take it up again it would likely be in the portfolio of its spin-off South Bow. Second, the physical pipeline that was in the ground has been mostly dug out. Third, Canada now has the TransMountain pipeline which makes the need for KeystoneXL less urgent. Having said all that, it is likely more about the message that it sends that America is pro-oil and pro-infrastructure. And matters less whether it happens or not.

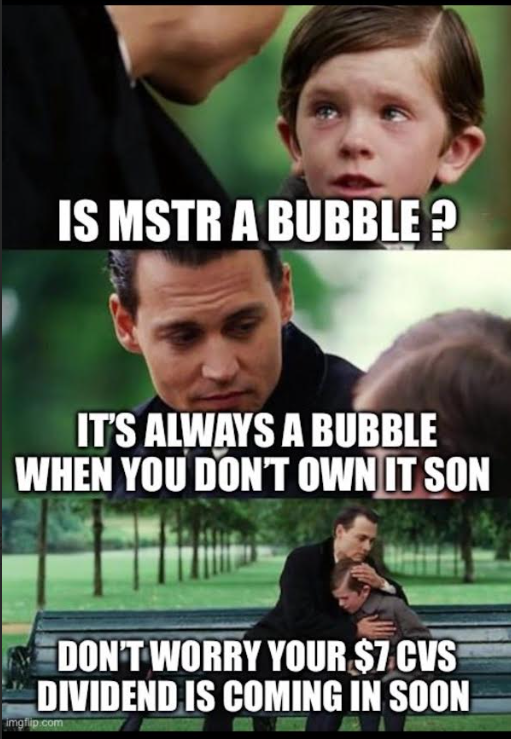

Moon landing: Bitcoin is less than 3% away from hitting $100,000. Prices have rallied 163% over the last year. That pales in comparison to MicroStrategy which is up more than 860%. Yesterday it was the most actively traded stock in America – more than Tesla and Nvidia. MicroStrategy’s primary business is buying and owning bitcoin. Right now, MicroStrategy owns about $30 billion in bitcoin, but is worth more than $106 billion. How can it be worth more than the bitcoin it is holding? I’ve heard Michael Saylor try to explain it and I’ll be honest it doesn’t make sense to me. The premium could be because they are raising money through debt and as of now bond investors have very limited ways to get bitcoin exposure. So it seems they are willing to pay up for it even if it means buying bitcoin at an equivalent price of $300,000. You can argue they are more protected on the downside because they are debtholders, but that is still one heck of a premium. Colour me skeptical. But also, this is literally me: