The big 5 banks report results this week along with Nvidia. Read all about it in my week ahead preview in The Globe and Mail!

LATEST EPISODE: For years, U.S. markets felt unstoppable. Now the script is flipping. On this episode of In the Money with Amber Kanwar, Matthew Strauss, SVP, Portfolio Manager & Lead – Global Equities at CI Global Asset Management, makes the case for rotating into global and emerging market equities. After years of American dominance, Matthew argues that stretched U.S. valuations, crowded positioning, and a shifting growth differential are finally pushing investors to look abroad.

Here are five things to know today:

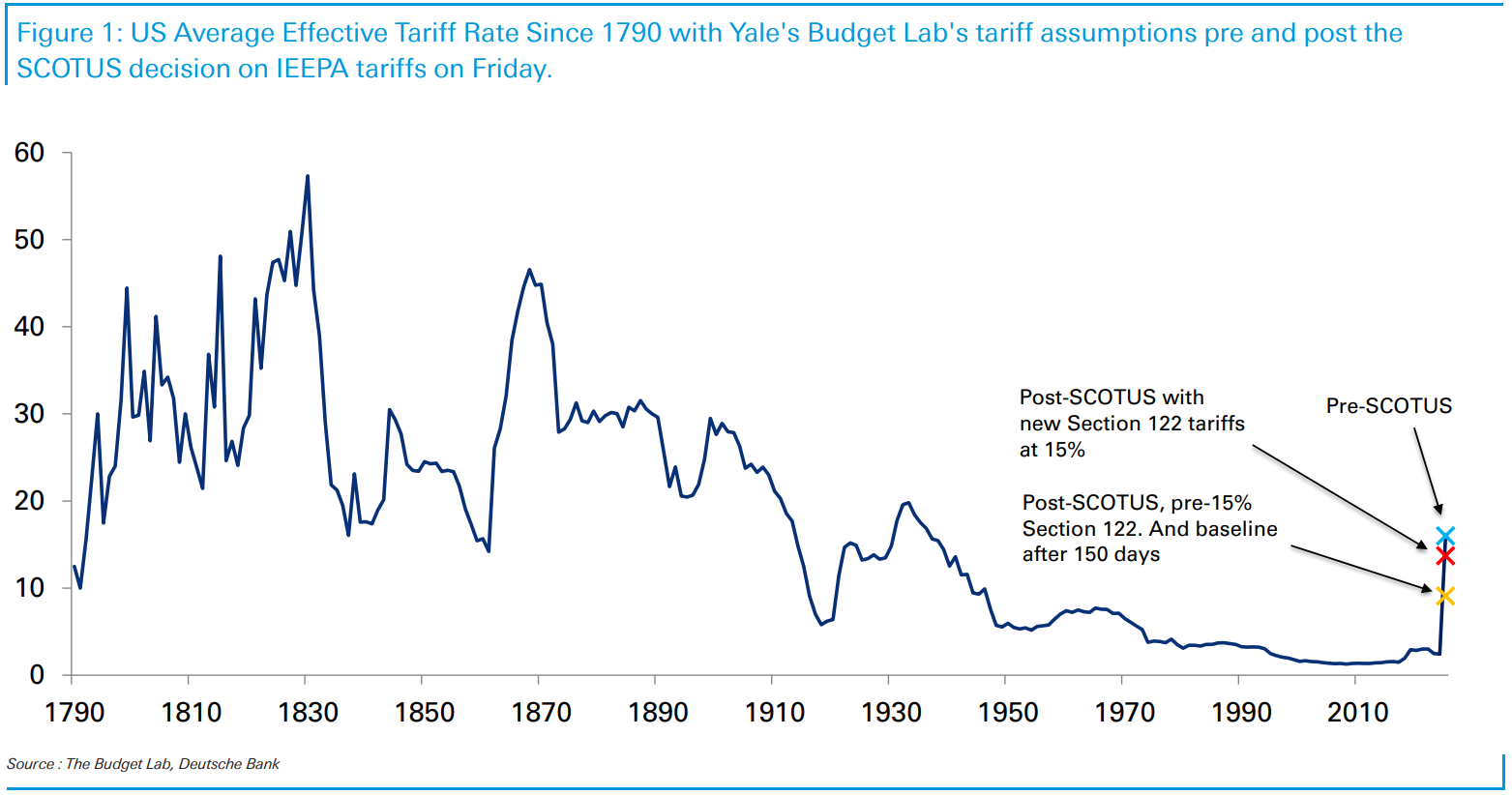

Whack-a-tariff: US futures are under pressure on the announcement of new tariffs after the US Supreme Court struck down tariffs enacted under emergency measures. Undaunted, US President Donald Trump announced he was hiking Section 122 tariffs (temporary tariffs up to 15% that can be placed by the President to address balance of payment issues). This boosts the average effective tariff rate in the US to 13.7% according to the Budget Lab at Yale, which is still lower than the 16% rate when the emergency tariffs were in place but higher than the 9% when they were struck down Friday (see chart below). It is unclear how this would affect countries that have trade deals or are negotiating trade deals. That uncertainty is contributing to market anxiety today. “The bottom line is that there’s a lot of noise and legal uncertainty but even allowing for a pivot toward Sections 232 and 301 to replace (emergency measures) over time,” wrote strategist Jim Reid at Deutsche Bank, “and with Section 122 likely temporary—the direction of travel still looks like a lower effective tariff rate in 2026.” Outside of tariffs, there are other items generating frown lines this morning. OpenAI increased its sales forecast for the next five years, but that comes along with a cash burn that was twice more than expected and gross margins which were 33% – well below the 46% expected. Airline stocks could be a mess today with no flights into New York because of weather and violent eruption in Puerto Vallarta halting air travel. Add in Cuba for Canadian airlines and there are a lot of headwinds for the sector recently.

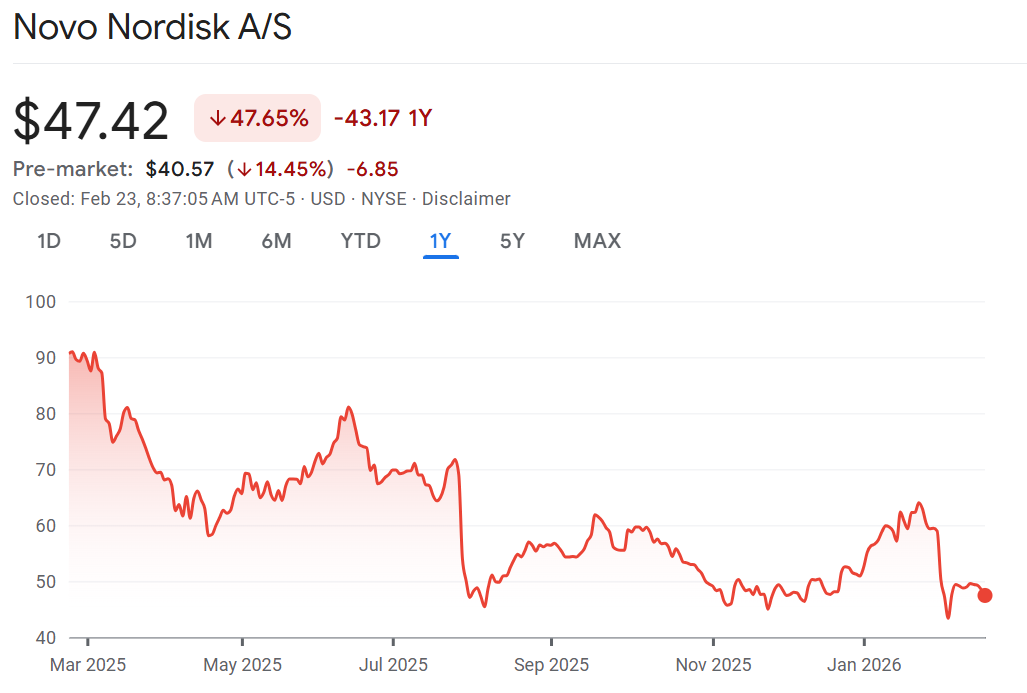

Lunchbag letdown: Novo Nordisk is plunging 14% after its obesity shot failed to deliver more weightloss than Eli Lilly’s version. Novo is poised to open at a 5-year low. Lilly is bouncing 3.5% in the pre-market (I own this one). Individuals treated with Novo’s solution lost 20% of their weight compared to Eli Lilly’s version in which people lost 23.6% of their weight. Novo needed this to reverse what has been an incredible fall from grace. The stock is now down 67% from its all-time high in 2024.

Stuffed crust: Shares of Domino’s are pumping after sales growth came in higher than expected. Profit was a little lighter and gross margins fell from last year. Keep in mind that the stock has languished so a little bit of good news is helping the stock. Remember, Berkshire Hathaway is the second largest shareholder owning just under 10% of the company. “As we look ahead to 2026, it is our expectation that we will meaningfully increase our market share within a U.S. (quick-serve restaurant) pizza category that continues to grow”

Swing and miss: Emera missed profit expectations when it reported results this morning. However, the utility also extended its promise to grow profit 5-7% annually until 2030. The miss was largely due to weather which affected its Florida operations while higher expenses weighed on its Canadian business. “We believe the extension of EMA’s EPS growth target to 2030 mitigates the modest miss on Q4/25,” wrote TD’s John Mould.

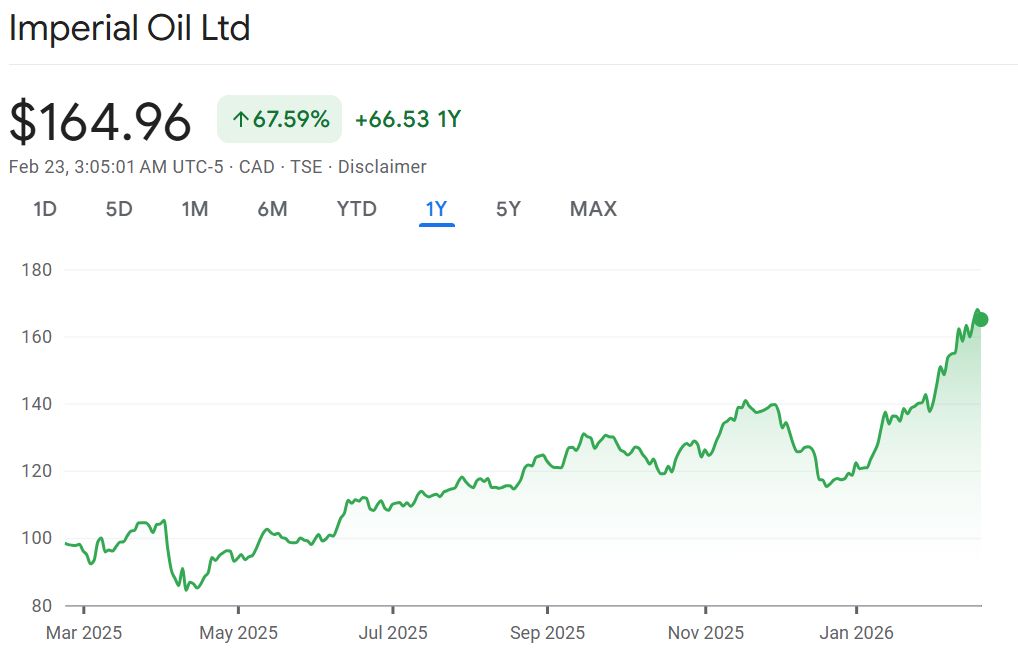

Ring the register: RBC is downgrading Imperial Oil and Athabasca Oil this morning. Imperial is being downgraded to sell with RBC’s Greg Pardy calling the stock’s outperformance “disconnected from its fundamentals.” The target price implies nearly 30% downside from here. Imperial recently announced restructuring which would transfer “above-field” employees out of Canada. This is a risk not priced in, argues Pardy. “We are mindful that a reorganization of above-field employees of this magnitude in Canada over the course of the next two years could impact the company’s operating performance, which has been impressive in years past.” The downgrade of Athabasca is less harsh and mainly due to valuation. Pardy downgrades to neutral saying they see better returns elsewhere with the price target implying just 1% upside.

Don’t miss our next episode!

![]()