Top investment ideas from Jeannine LiChong of Waratah Capital Advisors

Pro Picks: Resilience in Chaos – Three Defensive Stocks with Growth Ahead

Watch full episode: Markets are in meltdown mode, but Waratah Capital’s Jeannine LiChong says this isn’t the bottom. On this episode of In the Money with Amber Kanwar, veteran fund manager Jeannine shares how she’s navigating market volatility, tariff uncertainty, and growing recession risks.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information

1. Dollarama (TSX: DOL)

Why she likes it:

• Extremely cash-generative and self-financing—even international expansion is funded internally.

• EBITDA margins are 3x higher than Canadian Tire.

• Strong merchandising discipline and ability to scale operations efficiently.

Why it can go higher:

• Recent expansions into South America, Australia, and Mexico will be immediately accretive.

• Appeals to cost-conscious consumers during inflationary times.

• Not impacted by U.S. tariffs—Canadian importer.

2. Intact Financial (TSX: IFC)

Why she likes it:

• Core insurance holding with pricing power in a hard insurance market.

• Short liability duration allows for annual repricing—unlike life insurers.

• Strong cost control through vertical integration and auto dealership partnerships.

Why it can go higher:

• Well-executed M&A strategy (e.g. U.S. Specialty acquisition in the U.S.).

• Considered a defensive financial—could see inflows as investors rotate out of banks.

• Stock has outperformed in a down market, signaling resilience.

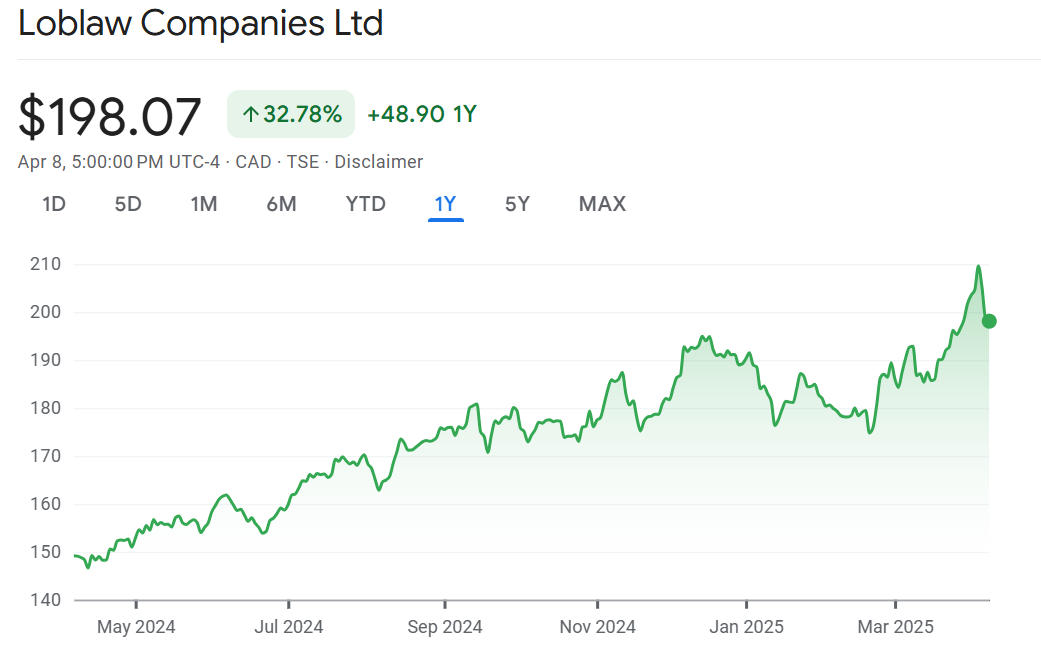

3. Loblaw Companies (TSX: L)

Why she likes it:

• Market leader in discount grocery through its No Frills brand.

• Maintains or gains share as consumers trade down.

• Well-capitalized with aggressive buybacks and inflation tailwinds.

Why it can go higher:

• Leverage to food inflation—pricing power and volume upside.

• Strong branding and communication (e.g. “Buy Canadian” and tariff transparency).

• Despite a high P/E (~30x), it’s a defensive staple with reliable cash flow