Inflation is surging again and it’s driving savvy investors to rethink how to manage their portfolios. So, what assets should you buy right now to protect your wealth? On this episode of In the Money with Amber Kanwar, James Davolos, Portfolio Manager and Director of Research at Horizon Kinetics, breaks down why investors need to reconsider everything they know about portfolio construction in a higher inflation world. He explains why a simple “buy gold” strategy isn’t enough, why real assets are still early in a long-term cycle, and why targeting 10%+ returns is essential just to stay ahead of rising prices.

Pro Picks is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

PAST PRO PICKS — April 15, 2025

ARIS — Aris Water Solutions | Taken out at $25 Picked at ~$23. Acquired by Western Midstream Partners. Management team has since pivoted to Solaris Energy Infrastructure. The water theme lives on.

PSK — PrairieSky Royalty | +52% Still owns it. 20M+ acre royalty position in the Western Canadian Sedimentary Basin. Growing LNG visibility in Canada. “Love the company” on a 5–10 year view.

X / TMX — TMX Group | Flat Still owns it. Sold off on AI obsolescence fears and the U.S. approval of Bitcoin perpetual futures — Dvolos calls both reactions overblown. Financial infrastructure with 40–60% operating margins doesn’t just disappear.

Average return on past picks: +26%

NEW PRO PICKS — June 8, 2026

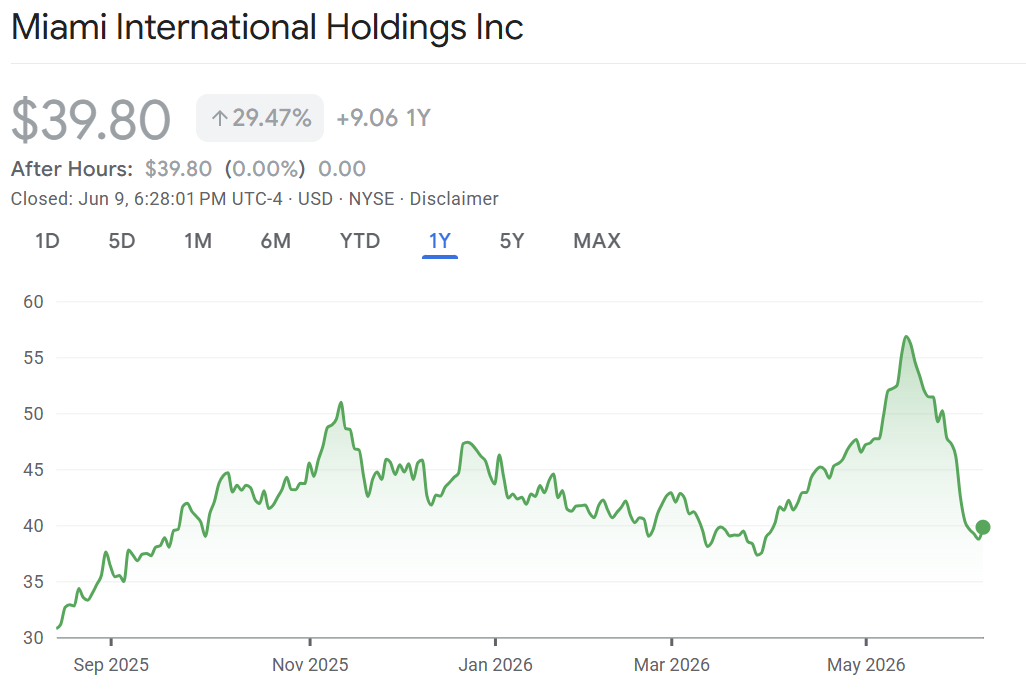

MIAX — Miami International Holdings A small-cap options exchange hiding a massive call option inside it

- MIAX built ~18% market share in U.S. multi-listed options by going where incumbents wouldn’t — low-margin contracts other exchanges ignored. Now pivoting to higher-value complex options where revenue per contract is meaningfully higher.

- U.S. options volume has grown from 16 million contracts/day in 2019 to ~63 million today — a 28% CAGR that has nothing to do with MIAX’s own execution and everything to do with the structural shift toward options trading.

- The real call option: MIAX is launching Bloomberg B500/B100 index futures — a fully rules-based competitor to S&P products with faster IPO inclusion. If SpaceX, Anthropic, or OpenAI go public and land in the Bloomberg index first, that’s an enormous high-margin revenue stream. “Pun intended — a very large call option embedded within one of the largest options exchanges in the U.S.”

- Potential takeout candidate. The exchange M&A math is obvious: combine two venues, strip out redundant tech and compliance costs, and already-fat margins get fatter.

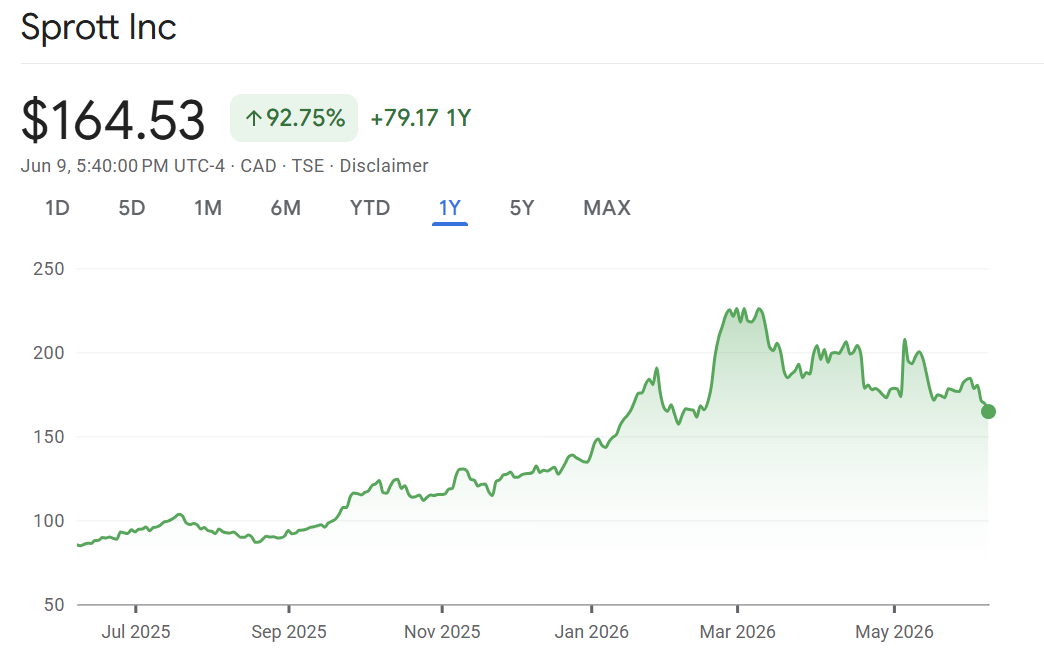

SII — Sprott Inc. The highest-margin way to own the precious metals and real assets thesis

- $65B AUM manager focused on precious metals and real assets. ~$50B sits in physical trusts (gold, silver, copper, uranium) — incredibly high-margin because there are no portfolio managers to pay and no positions to churn. AUM has grown 3x since 2021 at a 30% CAGR.

- EBITDA margins have expanded from 53% to 72% over that same period. Every incremental dollar of inflows flows almost entirely to the bottom line.

- Trading at ~13–15x forward earnings for a 70%+ margin, no-leverage business. The pullback — driven by gold and silver weakness — is the entry point. Physical trust investors are stickier than ETF holders; this isn’t the fast-money crowd leaving.

- At a ~$3B market cap, a larger diversified asset manager could easily justify consolidating this business. Quiet takeout optionality on top of an already compelling standalone.

LB — LandBridge A 72,000-acre Texas ranch that became the most important water business you’ve never heard of — and an AI data center play

- LandBridge owns surface rights on a massive West Texas ranch, leasing land and easements to Waterbridge for Permian Basin water infrastructure. The core business: for every barrel of oil produced in the Permian, there are 4 barrels of produced water that need to be moved, treated, and disposed of. ~90% EBITDA margins, ~25% projected annual growth for the next 2–3 years, 70% free cash flow conversion.

- Disposal of produced water is getting harder — shallow injection is now causing well blowouts and surface disturbances, creating a structural bottleneck that advantages whoever has the right surface position. LandBridge is that player.

- The asymmetric kicker: multi-gigawatt AI data center development is heading to West Texas. Data centers need water for cooling — wet cooling is far less power-intensive than dry HVAC in a desert environment. LandBridge’s surface position for land leases, power transmission, fiber, and water makes it a potential foundational piece of the entire buildout. “You don’t need there to be data center development — but that can really make the return profile asymmetric.”

- Horizon Kinetics owns approximately 20% of LandBridge. That’s the clearest possible signal of conviction.

Don’t miss our next episode!

![]()

DISCLAIMERS: This text AI generated and should be checked against actual delivery. The content provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.