AI was supposed to supercharge software. Instead, it’s threatening to disrupt it. Ivana Delevska, Founder & CIO of Spear Advisors, joins In the Money with Amber Kanwar to break down whether the brutal software sell-off is justified — or overdone.

Something weird just happened. I asked my kids to do something once and they are all doing it. I’m hesitant to even let out a breath lest I destabilize whatever precise cosmic alignment that led to this moment.

Here are five things to know today:

Keep on turning: Futures are indicating a higher open. There isn’t a whole lot to sink our teeth into this morning from a macro perspective. Tech is getting a boost as Nvidia is trading higher after announcing a deal with Meta to supply their hyperscale data centres. Although shares of peers like AMD, Broadcom and Arista Networks (top idea from Ivana) are feeling left out and under pressure this morning. The TSX got run over yesterday thanks to weakness in gold stocks. This morning gold prices are higher and tonight we get a number of gold companies reporting. Earnings are continuing on the TSX with 14 companies reporting today but all are after hours (which has become more common over the last few years). Names like Kinross, Equinox Gold, Alamos Gold and Nutrien all report this afternoon.

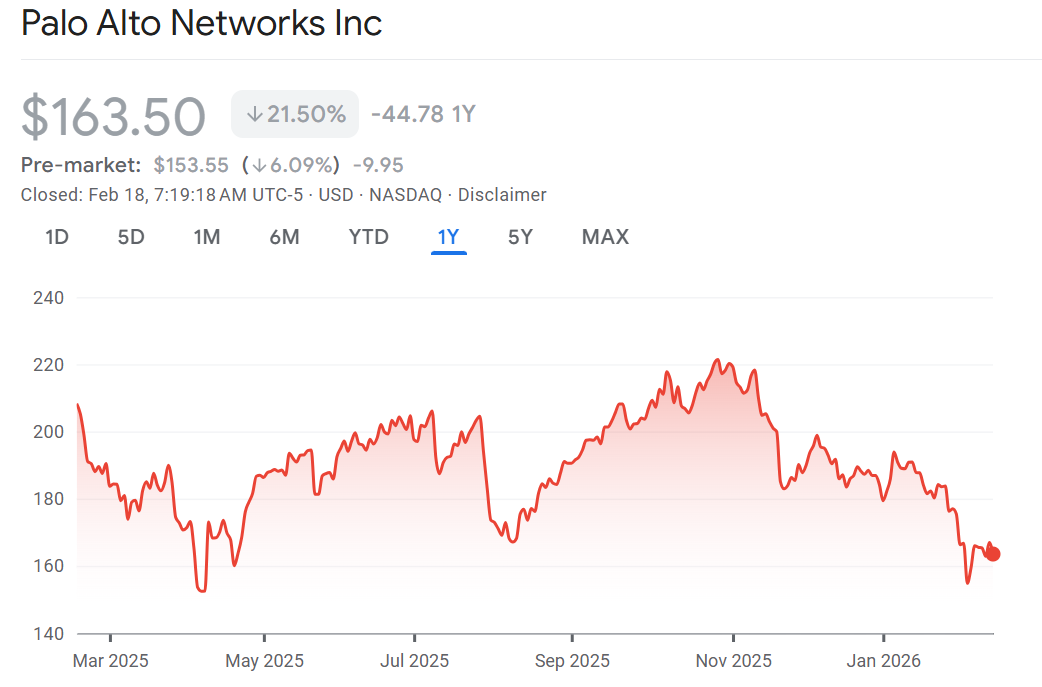

Cyber risk: Shares of Palo Alto Networks are down 6% after its profit outlook was slightly weaker than expected. The cyber security software company actually posted stronger than expected sales and profit in the reported quarter and boosted its forecast for sales and annual recurring revenue. The stock has been at the mercy of a software sell off, down 26% from October. It has also been digesting some major acquisitions including its $23 billion deal for CyberArk, a $3.4 billion deal for Chronosphere and smaller tuck-in of an agentic cyber security company Koi. Some are questioning the return on those acquisitions just as software as a whole is melting down. “While organic trends look intact, updated guidance for acquisitions suggests Palo’s initial near-$30B capital outlay has yielded just ~$1.5B in acquired (annual recurring revenue),” wrote Adam Tindle of Raymond James, “…but this was essentially a levered bet on software right ahead of a significant meltdown in valuations.”

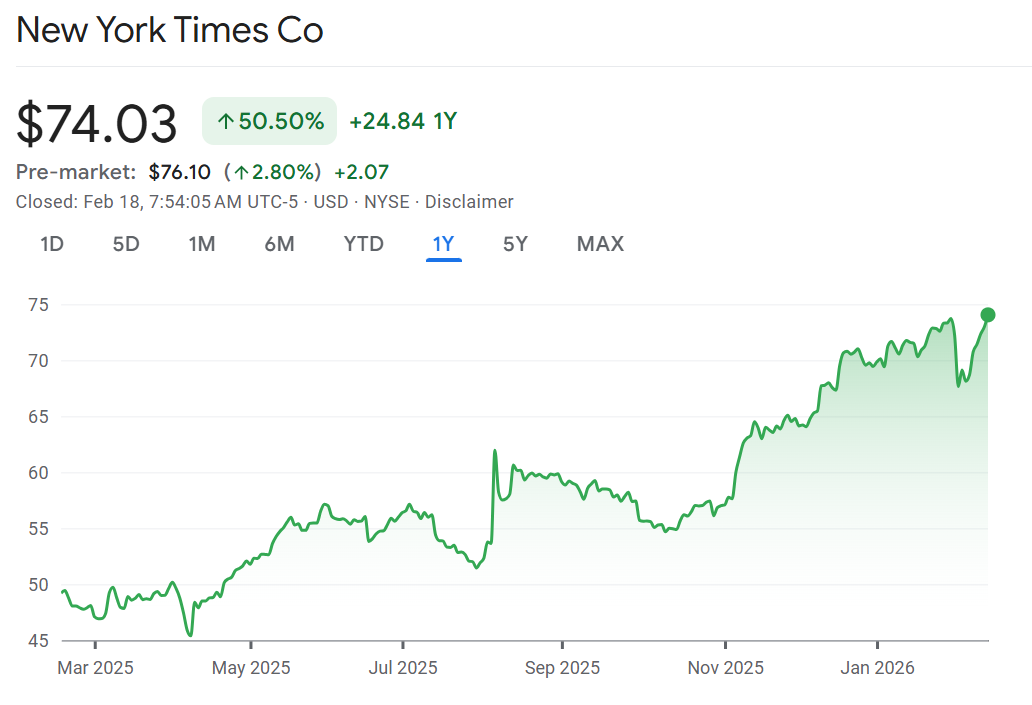

What the 13F: Selling tech stocks to by a newspaper company seems counterintuitive for this day and age, but that is exactly what Warren Buffett is doing in his last moves as CEO. Berkshire Hathaway revealed it has purchased a new stake in New York Times (+3% in the pre-market) while continuing to trim its Apple position and reducing its Amazon stake by 75%. To be clear, Amazon was never a big position, Apple remains a top holding, and the New York Times could disappear tomorrow and it wouldn’t make a dent in the portfolio. But this isn’t your grandparents Times, it has transformed into a digital company with the stock at a near record high. Other notable buys in the 13F filings include Soros Fund buying a new position Canada’s New Gold and Brad Gertsner’s Altimeter Capital revealing a new position in Shopify.

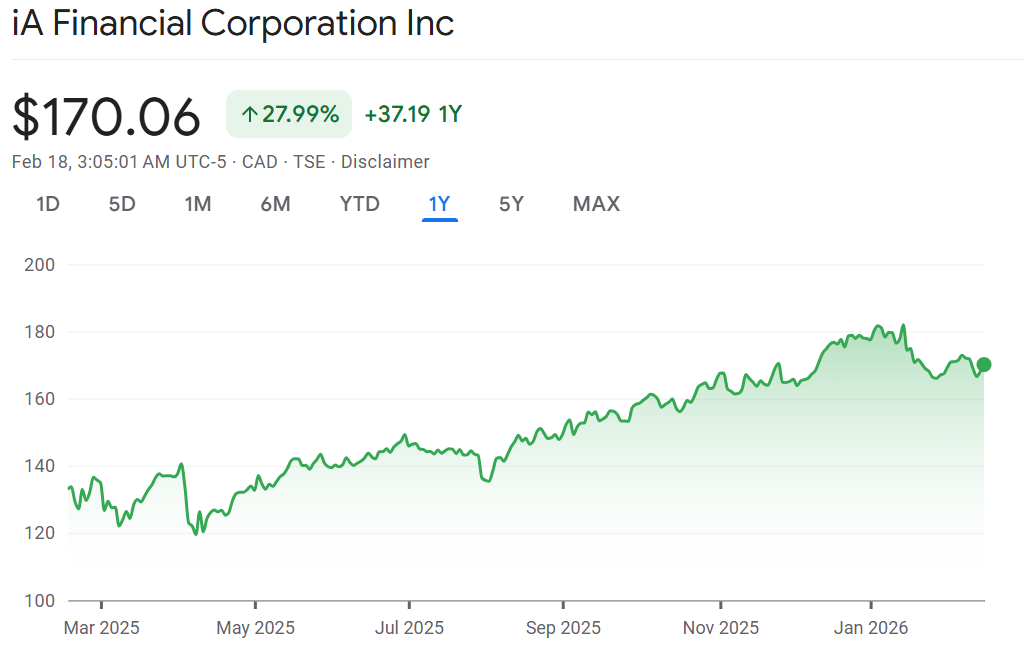

Big miss: Shares of iA Financial are likely to come under pressure this morning after a significant bottom line miss. The insurance and wealth manager reported core earnings that were 6% below consensus. The quarter was messy with the miss attributed to many things like experience losses, lower non-insurance earnings, and higher expenses. Earnings quality was also weak with reported earnings 37% below core earnings. Scotiabank downgraded the stock following the “underwhelming” quarter. The stock will remain under pressure in the absence of any near term catalysts, warned Mike Rizvanovic of Scotia in his downgrade.

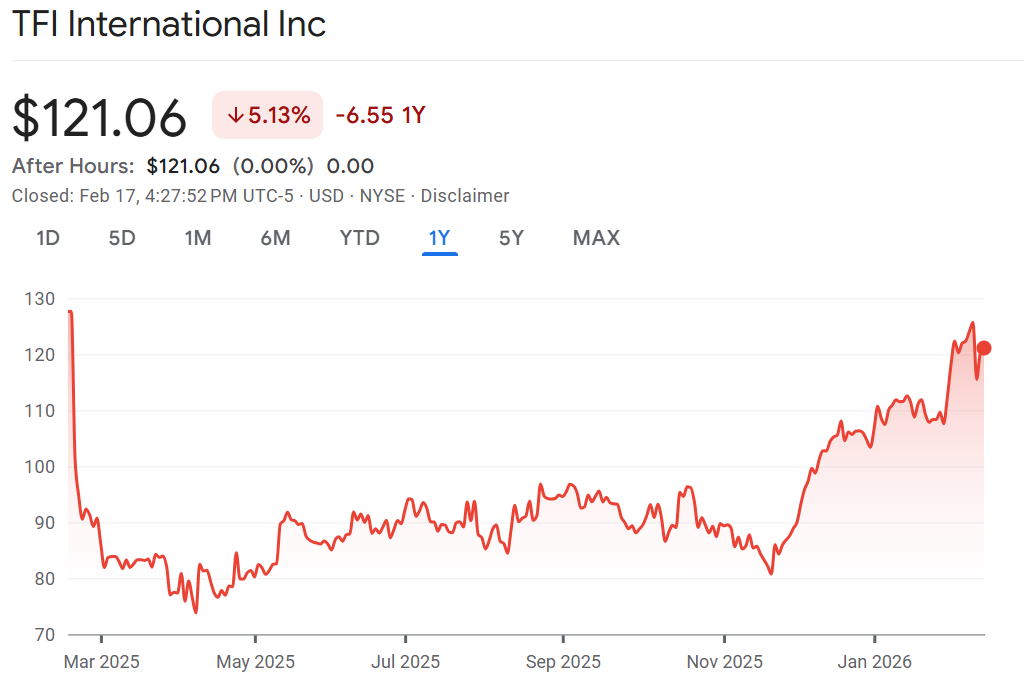

Honk honk: Watch shares of TFI International after its forecast significantly missed expectations. It is feeling a bit like deja vu because it was around this time last year that the stock plunged 21% in a single day after a quarter the CEO called a “disaster.” This time might be a little less severe. The trucking and logistics company gave an outlook for Q1 was below consensus, yet analysts don’t seem all that surprised. “Overall, we expect a neutral reaction as we believe whisper expectations for 1Q had fallen below consensus following management comments at recent conferences, the impact of severe weather should be broadly understood, and investors are likely starting to catch on to the company’s tendency to under promise and over deliver,” wrote Benoit Poirier of Desjardins. Since bottoming in March, TFI International is up 57%. There were some green shoots this quarter: truckload revenue and less-than-truckload revenue didn’t fall as much as feared. “Although freight demand remains soft and the Q1 guide is below our current expectations, there is mounting evidence supported by positive data points (spot trucking rates inflecting positively in recent months) that North American trucking capacity may finally be exiting the market, which could sustain a pricing recovery for the industry in 2026,” wrote Cameron Doerksen of National Bank.

Don’t miss our next episode on global markets outperforming the US!

![]()