Canadian stocks are hitting record highs, so where should investors look next? On this episode of In the Money with Amber Kanwar, veteran money manager Lyle Stein of Forvest Canada breaks down why he’s leaning into dividend paying resource stocks as the backbone of a portfolio.

Canadians love their bank stocks — and for good reason. They’ve delivered decades of strong returns and dividend growth. But what’s the easiest, low-cost way to own all six of the Big Banks without picking favourites? Enter Hamilton ETFs. Learn more about the Hamilton Canadian Bank Equal Weight Index ETF (HEB) — which comes with no management fee until 2026 — and the Hamilton Enhanced Canadian Bank ETF (HCAL), which uses modest 25% leverage to boost exposure and dividend yield.

Forgive me if this is disjointed. My boy is insisting I read “Goodnight, Goodnight Construction Site” before he goes to school. My attempts to replace “Cement mixer sings his whirly song” with, “We do not expect further earnings upside from credit normalization” is not going unnoticed.

Here are five things to know today:

Smash grab: Futures are higher this morning as AI deals continue to fuel optimism in the tech sector. Gold is higher and oil is up right now but still on pace for its biggest weekly decline since June. This weekend there is an online meeting of OPEC+ to decide on output for November and markets are nervous about the group increasing supply again to regain market share. Nevertheless, the TSX is riding a five session hot streak and closed at another all-time high yesterday. Normally today we would be counting down to the US payrolls report, but due to the government shutdown the data will not be released. On the shutdown, the betting markets have the shutdown lasting 10-29 days. Asian tech stocks were up overnight after Hitachi announced an infrastructure deal with OpenAI and Fujitsu expanded its collaboration with Nvidia. This is spreading to the North American tech stocks this morning.

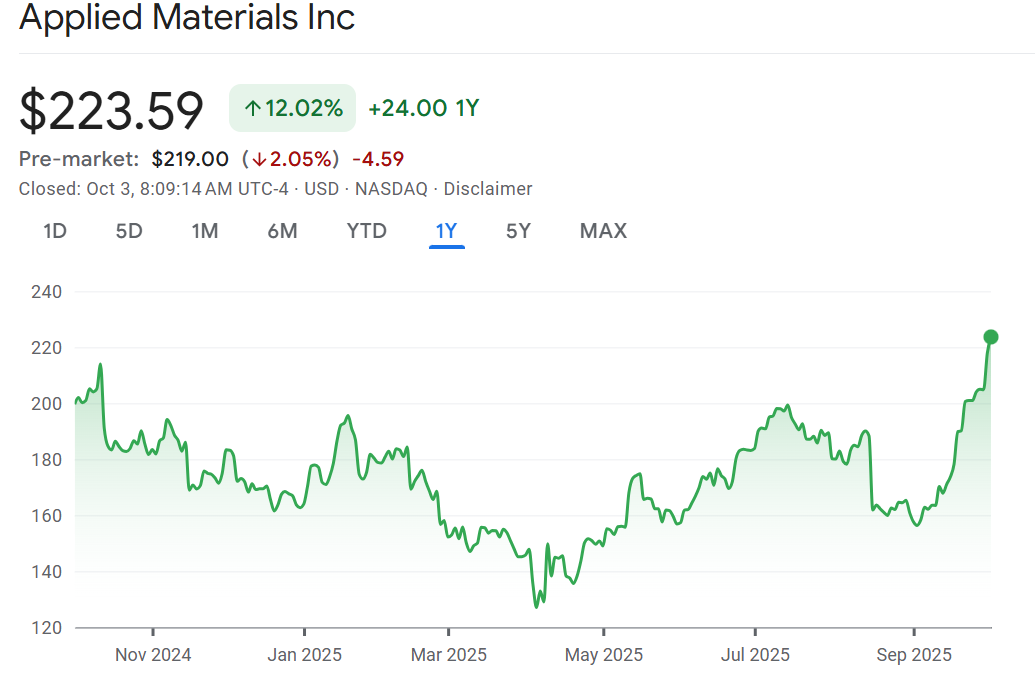

Applied track: Shares of Applied Materials are falling 2% after warning of a $600 million sales hit. The semiconductor equipment maker said sales will take a hit next year because of a new rules in the US that expand restrictions on what can be shipped to China. The stock has been on a tear lately, but analysts say the reduction is manageable. Citi estimates this is just a 2% hit to overall revenue. Bernstein’s Stacy Rasgon calls the update “annoying” but “mostly incremental.” Watch for warnings from peers like LAM research and KLA Corp.

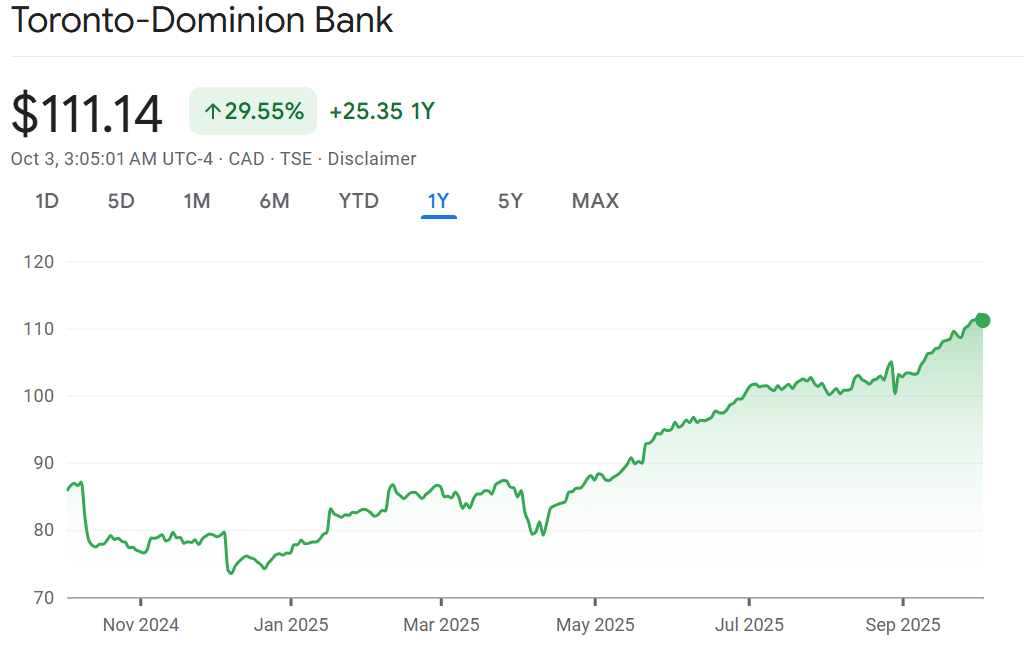

I like you when you’re high: TD is getting an upgrade from RBC following its investor day this week. “TD announced a significant incremental (share buyback) and cost savings targets at its 2025 investor day which were more than we had anticipated,” wrote RBC’s Darko Mihelic in the upgrade. While TD is now trading at record highs, Mihelic thinks it could go higher and has a $120/share price target implying 12% upside from here. Mihelic acknowledges TD is trading above its historic earnings multiple, but says higher capital return and better cost controls should drive valuation higher. On the flip side, RBC is downgrading BMO to hold mostly because they see limited upside to valuation. “We see valuation upside difficult to attain without further improvement in ROE and higher EPS, which we believe may happen but likely beyond 2027,” wrote Mihelic. BMO has been the second best performing major bank stock after TD so far in 2025, acknowledges Mihelic, but has the least room for additional buybacks he argues.

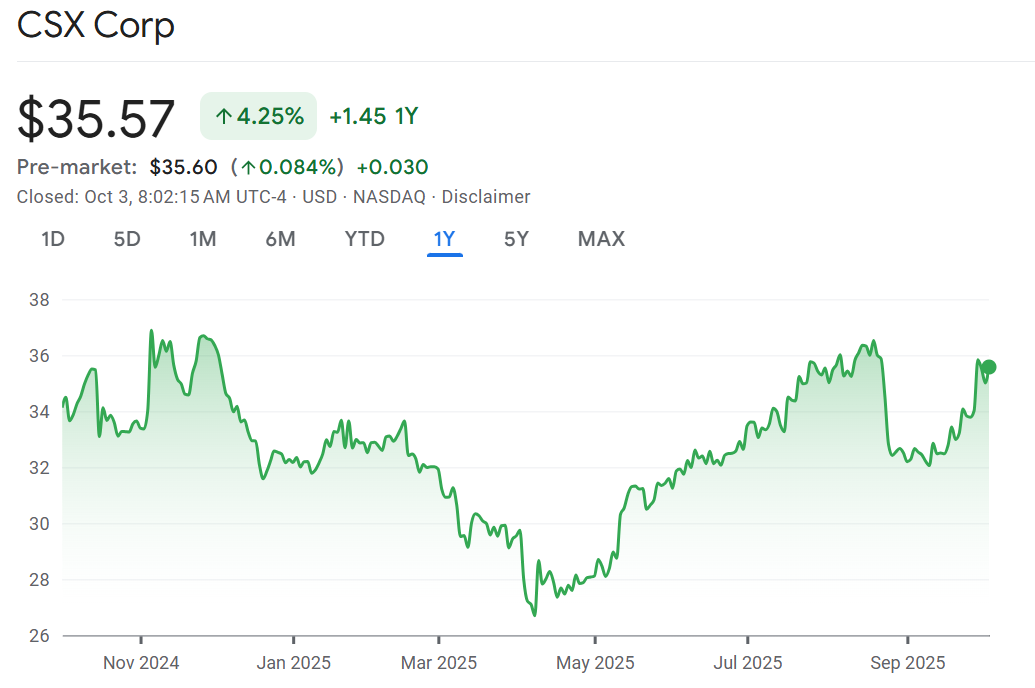

Musing: Earlier this week CSX surprised market with the sudden departure of its CEO amidst activist pressure. This morning Citi is musing about how this “could alter the dynamics of the rail M&A landscape.” Recall Union Pacific has already proposed to buy Norfolk Southern. While investors speculate about who else needs a dance partner, Citi’s Ariel Rosa believes this could lay the groundwork for a three-way merger between CSX, CP Rail and BNSF. “…We believe a BNSF-CSX-CP combination could make strategic sense, with Warren Buffett-led Berkshire being one of the only entities with the capital and credibility to make this combination happen,”

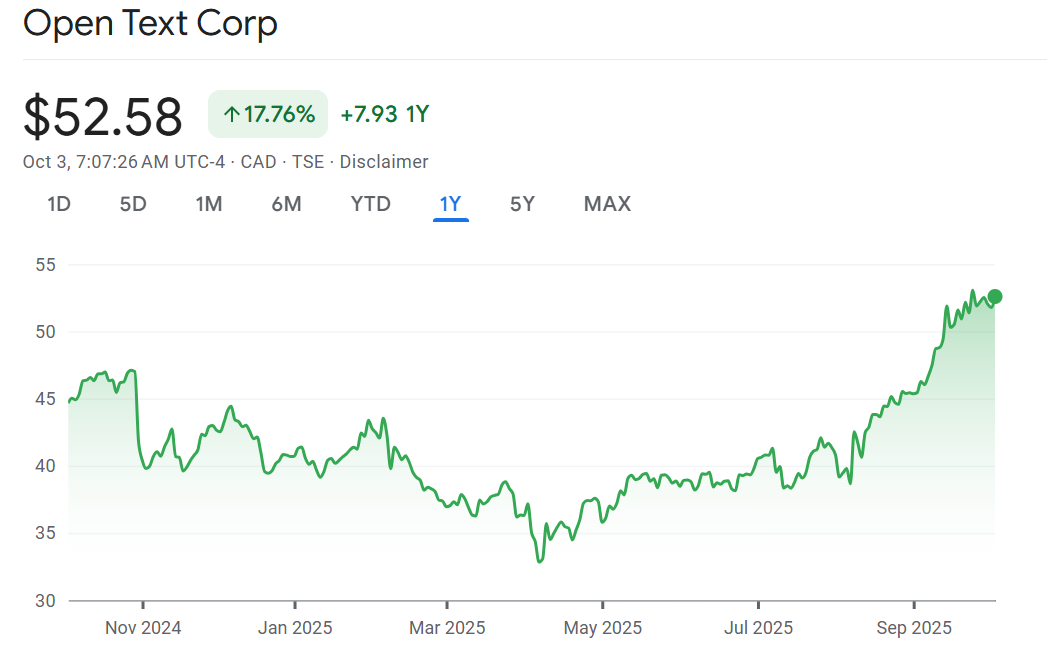

Addition by subtraction: Watch OpenText after announcing its first non-core divestiture for $163 million in cash. OpenText is selling its eDocs business in an effort to progress on its previously stated goals to pay down debt and refocus the company. Raymond James thinks they got a good multiple for the business and this could be a marker for future dispositions which is key to the stock’s performance. “An OpenText (with non-core assets divested) looks like a ~4-5% organic grower, high-30s EBITDA margins, a higher FCF margin rate (~25% potentially as OTEX pays down 7% debt) and a de-levered balance sheet. We think this has potential to re-rate the stock substantially,” argued Steven Li of Raymond James.

Don’t miss our next episode! Get your questions in now! Email questions@inthemoneypod.com

![]()