“If tech was the best performer for 25 years because it took in all the cash… what do you think happens when all the cash flows into commodities and infrastructure?” That’s the big question driving today’s conversation—and according to Daniel Dreyfus, the answer could define the next decade of investing. In this episode of In the Money with Amber Kanwar, Daniel Dreyfus, Chief Investment Officer at Bornite Capital, lays out his high-conviction thesis that we are in the early stages of the largest capital spending cycle in modern history.

Pro Picks is brought to you by ATB Financial. With over $100 billion in assets, ATB Financial is powering possibilities for more than 843,000 financial services clients. ATB Cormark Capital Markets is a leading North American investment firm providing holistic corporate and capital markets advice and full-service financial solutions. Visit www.ATB.com/inthemoney for more information.

Past Pro Picks

- Cheniere Energy (LNG): +10% (Still owns, continues to like US nat gas players)

- Ivanhoe Mines (IVN): +10% with significant volatility (Still owns — advice: take it off your screen and look at it in 5 years)

- Talen Energy (TLN): +87% (Brings it back as a Pro Pick today — believes there is still a 2–3x from here)

- Average return: 36%

Pro Picks: Power, Precious Metals & a Hidden Aerospace Play

Talen Energy (TLN)

A Re-Up on the Home Run — Power Prices Have Nowhere to Go But Up

- Trading at ~7x earnings today against estimated free cash flow of ~$50/share by 2028–2029, driven by a contracted power supply deal with an Amazon data center — Dreyfus believes it should trade at 15x, implying a double on current numbers alone

- The PJM grid operator (Pennsylvania, Jersey, Maryland) has projected 100 gigawatts of new power demand over the next 10 years — equivalent to Japan’s entire annual power consumption — and the supply chain simply cannot keep up

- A 20% increase in power prices, which translates to only a ~4% increase in a typical utility bill (power is just 20% of the bill), would take earnings power to ~$70/share — at 15x, that’s a 3x from today’s ~$350 stock price

- Additional upside optionality from further long-term take-or-pay agreements with new data centers as AI buildout accelerates; Dreyfus views this capex cycle as mandatory, not discretionary

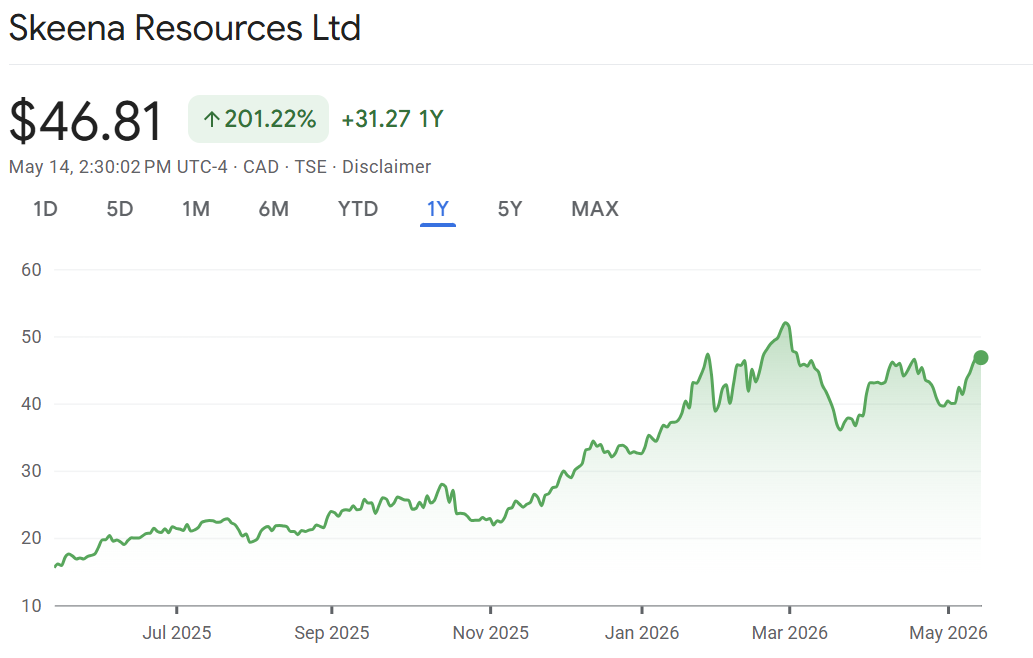

Skeena Resources (SKE)

The Pro Pick — A Fully Permitted Silver-Gold-Antimony Restart in BC at a Fraction of Its Intrinsic Value

- Skeena is restarting the Eskay Creek mine in British Columbia — originally owned by Barrick, which shut it down when gold prices were low and diesel costs were high; Skeena acquired it, permitted it, and built a hydroelectric dam, giving it access to some of the lowest-cost power on the planet

- Produces three commodities whose end markets are all on fire: gold (currency debasement hedge), silver (solar panels, semiconductor fabs, industrial demand), and antimony (military applications) — stock trades in the low-$30s (USD)

- At spot prices, Dreyfus estimates the mine will generate $8–$9/share in free cash flow; at 12x — standard for a low-cost, long-life Canadian mine — that implies a ~$100 stock, roughly a 3x from today

- The most de-risked milestone — permitting — is already done; this is a restart of an existing mine, not a greenfield build, which significantly reduces execution risk; first real year of production expected in 2028

- If Dreyfus is right that silver prices double (citing a 200M oz/year structural deficit with only ~3 years of above-ground inventory remaining), the upside is dramatically higher — “this is how 10xs are born”

Carpenter Technology (CRS)

An Under-the-Radar Aerospace Monopoly Compounding at 15–25% a Year

- Carpenter manufactures nickel superalloys — the single most acute pinch point in the entire Boeing/Airbus aerospace supply chain, which carries over $1 trillion in combined backlog over the next decade; Dreyfus calls it effectively a critical mineral

- Pricing power is structural, not cyclical: aerospace certification requirements make it nearly impossible to substitute cheaper alternatives, locking in Carpenter’s quasi-monopolistic position for parts on moving aircraft components

- Supply chain underproduction over the last 5–7 years (COVID, Boeing safety issues) means the restart of new plane production has 5–7 years of catch-up demand baked in, independent of any new demand growth

- Looks expensive on near-term multiples but Dreyfus expects 15–25% annual earnings compounding over many years of high-visibility backlog — “it doesn’t take that many years of compounding at that rate to make the stock look pretty darn cheap”

Don’t miss the next episode!

![]()